Global| Jan 08 2014

Global| Jan 08 2014German Orders Surge Back But Domestic Orders Lag

Summary

German orders rose by 2.1% in November, rebounding from a 2.1% drop in October. The headline trend shows solid growth with three-month growth at a 12.7% annual rate, up from a 6.2% annual rate over six-months and a 6.8% annual rate [...]

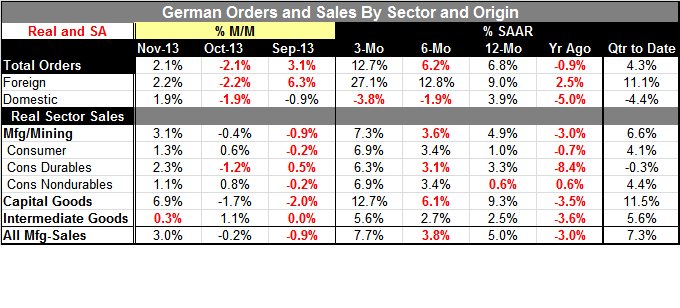

German orders rose by 2.1% in November, rebounding from a 2.1% drop in October. The headline trend shows solid growth with three-month growth at a 12.7% annual rate, up from a 6.2% annual rate over six-months and a 6.8% annual rate over 12-months. The strength is led by foreign demand.

German orders rose by 2.1% in November, rebounding from a 2.1% drop in October. The headline trend shows solid growth with three-month growth at a 12.7% annual rate, up from a 6.2% annual rate over six-months and a 6.8% annual rate over 12-months. The strength is led by foreign demand.

Foreign orders rose by 2.2% in November from a 2.2% drop in October but also logged a 6.3% increase in September. As a result, foreign orders are rising at a 27.1% annual rate over three-months, up from a 12.8% annual rate over six-months, and a 9% annual rate over 12-months. The foreign sector clearly is strong and accelerating; this is what is underpinning growth in Germany.

In contrast, domestic orders rose by 1.9% in November, unwinding a 1.9% drop in October. However, domestic orders also fell by 0.9% in September. As a result, the trend for domestic orders is poor. It is not just weaker than foreign orders - it is poor. Domestic orders are falling at a 3.8% annual rate over three-months following a 1.9% annual rate drop over six-months and a 3.9% annual rate gain over 12-months. The domestic sector is in a clear deceleration and contraction. This is completely apart from the kinds of reports with that we get about the strength of the German economy and how strength in the rest of the European Monetary Union is helping to spread even more growth in Germany. German employment has been improving and German unemployment has been falling.

Perhaps the result on domestic orders reflects some anomaly and timing or weather issues. German real sector sales are doing much better. For mining and manufacturing sales are up at a 7.2% annual rate over three-months, up from a pace of 3.6% over six-months and 4.9% over 12-months. This progression shows that growth in real sector sales is sustaining itself. Consumer goods sales have come in at a 6.9% rate over three-months with durables up at a 6.3% annual rate and nondurables up at a 6.9% rate. Overall real sector sales are dominated by capital goods, which is exactly what you would expect in an upturn in Germany. Capital goods are growing at a 12.7% annual rate over three-months, compared to a 6.1% pace over six-months and 9.3% over 12-months. Intermediate goods show sales of 5.6% over three-months and 2.5% over 12-months.

On balance, the results for German domestic orders are surprising and out of kilter with other data points that we have seen. In the quarter to date, overall German orders are up in a 4.3% annual rate with foreign orders leading, rising by 11.1% at an annual rate; domestic orders are falling by 4.4% at an annual rate. There is simply no way to understand this weakness in domestic orders apart from chalking it up to some anomaly - given the strength and other German data.

One clear takeaway from the German data, however, is that the foreign sector seems to be improving significantly. And this finding is completely in tune with other data that show a growing world economy and an improvement in Europe. For the time being, this is the part of this report that make sense and that we can take to the bank. The anomalous weakness in domestic orders is something that we will for the moment chalk up and something that is quizzical and that we expect to see turned-around in the coming months. There is simply too much strength of the rest of the German economy to think that domestic orders could continue to remain this weak.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief