Global| Aug 06 2014

Global| Aug 06 2014German Orders Sink as Italy Slips into Recession

Summary

It has not been a good day for statistics out of Europe. Italy has just unexpectedly recorded its second consecutive drop in quarterly GDP, giving way to cries of recession. Germany has reported out a large drop in orders and the [...]

It has not been a good day for statistics out of Europe. Italy has just unexpectedly recorded its second consecutive drop in quarterly GDP, giving way to cries of recession. Germany has reported out a large drop in orders and the second large drop in a row. The two months together show a drop in total German orders, that was last larger when Germany exited from recession in February of 2009 over five years ago. German Ifo and ZEW data have been backing off for several months. Yesterday's PMI data showed a broad flat spot for Europe and today German and Italian data show extreme weakness. It's not a good trend.

It has not been a good day for statistics out of Europe. Italy has just unexpectedly recorded its second consecutive drop in quarterly GDP, giving way to cries of recession. Germany has reported out a large drop in orders and the second large drop in a row. The two months together show a drop in total German orders, that was last larger when Germany exited from recession in February of 2009 over five years ago. German Ifo and ZEW data have been backing off for several months. Yesterday's PMI data showed a broad flat spot for Europe and today German and Italian data show extreme weakness. It's not a good trend.

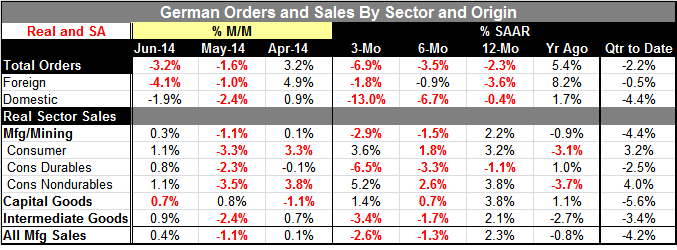

German orders fell by 3.2% in June against a forecast for a rise of nearly 1%. And now that drop forms a back-to-back drop, combining with a 1.6% decrease in May. In June, total orders fell, foreign orders fell and domestic orders fell. It was a clean sweep.

German orders show sequential growth rates, forming a pattern of clear ongoing deterioration. Orders drop at a 2.3% annual rate over 12 months; that expands to -3.5% over six months and grows to -6.9% over three months.

Foreign orders are weak, but domestic orders are weaker. Domestic orders show the same deteriorating pattern as 12-month orders show a -0.4% annual rate that expands to -6.7% over six months and culminates at -13% over three months.

Orders from places inside the euro area fell by 10.4% in June. Capital goods orders from inside the euro area fell by 19.5%. Meanwhile, orders from places outside the euro area fell by 4.1%. The economics ministry laid some of the weakness at the feet of bulk orders, saying that excluding such items orders would have risen by 1.1%. What is clear from this pattern is that weakness is coming from inside the euro area, but we can only speculate as to what the true cause of that may be. Is it simply domestic deterioration? Or is there some loss of confidence over external factors?

German foreign orders are weak but do not show the same sequential deteriorating pattern as overall orders and domestic orders. But foreign orders fell by an outsized 4.1% in June as domestic orders dropped by only 1.9%.

Real sector sales in Germany show progressive deterioration with manufacturing sales up by 2.3% over 12 months then falling at a 1.3% annual rate over six months with that accelerating to -2.6% over three months. Sales of consumer durable goods and intermediate goods are being hit the hardest. Capital goods sales are still growing, but sputtering.

Of course, the first reaction is to blame this on the Russian sanctions and their geopolitical fall out. And that may be what it is. That does not make the ongoing fallout any easier to take. The sanctions were imposed at a time that inflation in the euro area had fallen so much that the European Central Bank launched a special program to stimulate lending. But this is a new bit of weakness on top of that and it comes with European banks still not ready to do heavy lifting as we see from the recent banking problems in Portugal.

German orders and sales are showing declines in the recently completed second quarter. Italy is showing a GDP decline in that quarter. Poland's Prime Minister Donald Tusk said today that the risk of direct Russian intervention in Ukraine had risen. In Russia, Putin has been urging the government to take retaliatory steps against the sanctions that have been imposed on it. It does not look like we are past the worst of this yet.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief