Global| Aug 06 2015

Global| Aug 06 2015German Orders Rise on the Foreign Sector; Domestic Orders Remain Moribund

Summary

The story this month is less about how well German orders are doing and more about how weak Germany's domestic orders have become. With an economy that is doing quite well - certainly by Europe's standards - and maintaining a low rate [...]

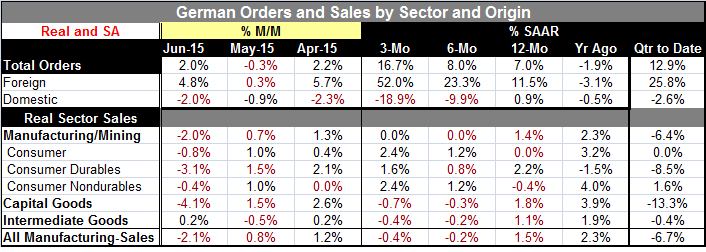

The story this month is less about how well German orders are doing and more about how weak Germany's domestic orders have become. With an economy that is doing quite well - certainly by Europe's standards - and maintaining a low rate of unemployment, Germany's domestic orders are pathetically weak. Domestic orders have fallen in each of the last three months. Current German order growth, which is still impressive, is completely relying on Germany's ability to exploit demand in other nations. The low euro exchange rate is helping Germany to do that and to maintain a huge current account surplus relative to its GDP.

The story this month is less about how well German orders are doing and more about how weak Germany's domestic orders have become. With an economy that is doing quite well - certainly by Europe's standards - and maintaining a low rate of unemployment, Germany's domestic orders are pathetically weak. Domestic orders have fallen in each of the last three months. Current German order growth, which is still impressive, is completely relying on Germany's ability to exploit demand in other nations. The low euro exchange rate is helping Germany to do that and to maintain a huge current account surplus relative to its GDP.

Germany, the strong economy of Europe, is staying strong by poaching domestic demand in countries that are largely less strong than Germany itself. While orders from inside Germany were down 2% compared with May, order demand from other countries in the euro area rose 2.3% higher and orders from outside the currency area rose 6.3%. Fortunately, German orders are growing fastest outside the euro area when the lower euro has given it an increasing advantage. But inside the euro area, Germany maintains an advantage from years of keeping its inflation rate below that in every other member and that policy continues to pay dividends for German exports within the euro area.

Germany's competitive position within the EMU remains paramount. Thus, in trade among EMU nations, German goods are usually the cheapest for products where Germany has its best advantage. But as the strong economy of Europe, Germany is offering no access whatsoever to its own domestic demand. Germany continues to run a large trade surplus. Germany's growth contributes nothing to its surrounding economies, save envy.

For some time, Germany has run an excessive trade balance (surplus) in the EMU. This is something that is reviewable under the Macroeconomic Imbalance Procedure (MIP). But Germany is far more interested in pursuing the intransigence of others, such as Greece. Germany can tell you that haircuts are a violation of the euro area pact, but it can then ignore its own excessive trade surpluses and their impact on the rest of the EMU year-after-year.

The European Commission has looked into this issue of excessive imbalances even when it applies to surpluses (see here). Germany, while often cited as an example, has never been sanctioned. Yet, it is clear that being in a currency arrangement with one member that hogs surpluses will affect adversely the other members of the arrangement. Germany has pursued a strategy of having the lowest inflation in the EMU and has aggressively used it to extend its competitiveness to the detriment of its neighbors.

Right now German foreign orders are literally exploding. They are rising at a 52% annual rate over three months, up from a 23.3% annual rate over six months and an 11.5% gain over 12 months. On those same time lines, domestic orders are contracting at an 18.9% pace over three months, falling at a 9.9% pace over six months but still are higher by a skinny 0.9% over 12 months.

The German economy is being lit up by foreign demand.

Over three months, the strength in output has been all in consumer products with capital goods and intermediate goods sales lower. But capital and intermediate goods sales are declining over all horizons in the table out to one year. While German orders are flying on the back of international demand, manufacturing sales have been gradually shrinking over the last year. Maybe stimulating domestic demand would be good for Germany too?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief