Global| May 07 2013

Global| May 07 2013German Orders Put in Strong Back-To-Back Gains

Summary

German factory orders rose by 2.2% in March building on a gain of 2.2% in February. Surprisingly, driving the overall growth were orders from the euro-zone market which jumped 4.2 percent. Total overseas orders rose 2.7 percent, while [...]

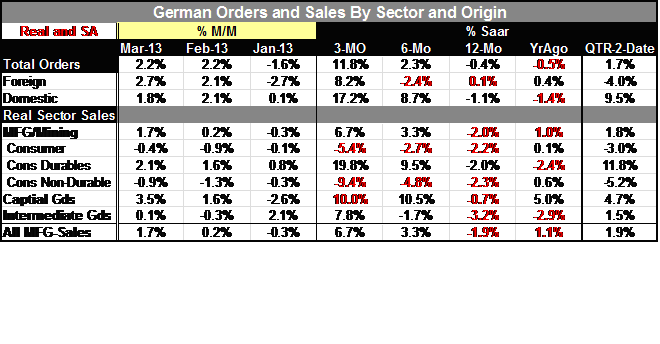

German factory orders rose by 2.2% in March building on a gain of 2.2% in February. Surprisingly, driving the overall growth were orders from the euro-zone market which jumped 4.2 percent. Total overseas orders rose 2.7 percent, while new orders in the domestic market moved up by 1.8 percent.

German factory orders rose by 2.2% in March building on a gain of 2.2% in February. Surprisingly, driving the overall growth were orders from the euro-zone market which jumped 4.2 percent. Total overseas orders rose 2.7 percent, while new orders in the domestic market moved up by 1.8 percent.

With these strong back-to-back numbers, three-month growth rates for orders are now nearly 12% at annual rate foreign orders are rising at about an 8% in annual rate. The order surge is led by domestic orders which are pulsing at a 17% annual rate. The current surge is making up for some previous sluggishness. Over six months orders are up at just a 2.3% annual rate; foreign orders are down at a 2.4% annual rate but even over six months domestic orders are up at 8.7% annual rate.

Even so year-over-year figures for Germany remain weak with overall orders down by 0.4% foreign orders up by just 0.1% and domestic orders down by 1.1%.

Real sector sales show that there is strength coming from consumer durables which are rising at a nearly 20% annual rate over three months and from intermediate goods where sales are rising at nearly an 8% annual rate over three months. Still we find sales of consumer durables down by 2% over 12 months and even intermediate goods sales are down by 3.2% over 12 months.

The burst in the pace of orders in March is certainly a good thing for the German economy. However, this report does not dovetail well with the ongoing weakness that we see from the manufacturing ISM or the service sector ISM, both of which point to continuing weak domestic conditions. It's hard to square the weak ISM reading for Germany with the notion that domestic orders are rising at 17% annual rate over three months. We are told that this report was dominated by some large block orders. It's possible that such orders have pushed up the growth rates and do not represent business that will continue to rise in the future turning the current months rise into an unsustainable blip.

For the moment markets are celebrating the German figures. And however good they appear, one thing we must bear in mind is that they are not consistent with a number of other reports we've seen to date. So as we view new incoming data for the Zone and for Germany, we are going to have to subject everything to the veracity test to try to figure out what's really going on in Germany which has continued to be the backbone of growth in Europe and which may or may not be accelerating.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief