Global| Jun 05 2020

Global| Jun 05 2020German Orders Plunge in April

Summary

Germany's orders plunged in April, falling by 25.8% m/m after a 15.0% drop in March. The two-month decline for overall orders, for foreign orders, and for domestic orders each are the largest two-month drops seen on German data back [...]

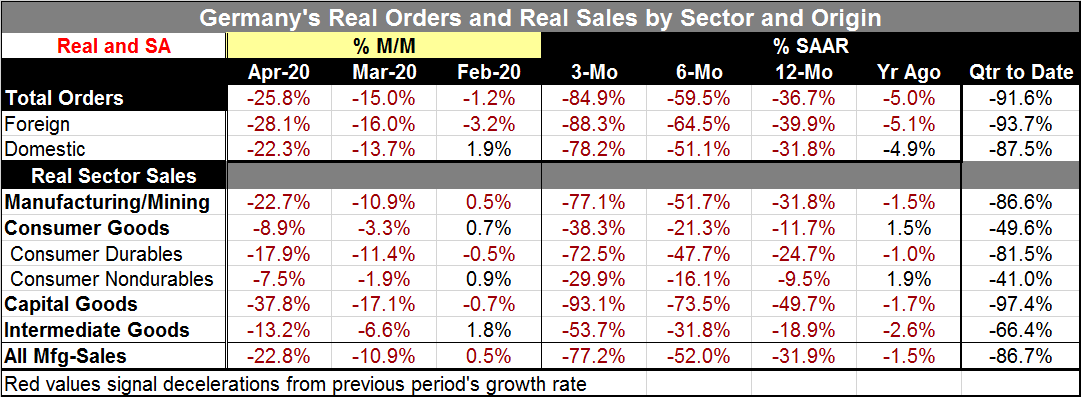

Germany's orders plunged in April, falling by 25.8% m/m after a 15.0% drop in March. The two-month decline for overall orders, for foreign orders, and for domestic orders each are the largest two-month drops seen on German data back to March 1991. The annual rate of decline in the current unfolding quarter is at a pace near -90% for all sectors.

Germany's orders plunged in April, falling by 25.8% m/m after a 15.0% drop in March. The two-month decline for overall orders, for foreign orders, and for domestic orders each are the largest two-month drops seen on German data back to March 1991. The annual rate of decline in the current unfolding quarter is at a pace near -90% for all sectors.

Sales are also cascading lower across the board and on all timelines Capital goods sales in the current quarter (quarter-to-date) are falling at neatly a 100% annual rate. Consumer nondurables show the least weakness falling in the current quarter at a -41.0% annual rate. For all of manufacturing, the decline in sales is progressing at a -86.6% annualized rate of decline early in Q2 compared to Q1.

The report is so weak and so bleak that there is almost nothing meaningful- certainly nothing positive- to say about it…that is apart from the fact that we have probably seen the worst. Germany has adopted another stimulus plan. The EU is still negotiating its stimulus program while the ECB has sweetened its participation in markets. There are many forces at work to try to feed some stimulus into the global economic system to spur growth.

But the best news of all today comes from the U.S. with the May employment report showing job gains of 2.5 million instead of losses nearly double that that were expected. The sharp turnaround in the U.S. will be good news to the rest of the world. It means two things: (1) that the U.S. did not dig itself into as deep a hole as we had feared and (2) that recovery has begun sooner than expected.

The U.S. turnaround is going to change the timing and shift the optimism regarding the global recovery. U.S. trade data have already been showing much weaker U.S. exports than imports confirming that U.S. domestic demand has been better preserved than has foreign demand in the markets to which the U.S. exports.

While the U.S. jobs reports are grounds for some optimism, the bottom line is still that the impact from the Coronavirus has been a severe body blow. The U.S. shed 22 million jobs in March and April. In May it has created 2.5 million. That is a good turn but still a deep hole of job losses. The signal from the U.S. is for an earlier turn than expected and of a somewhat reduced severity in the downturn, but the challenges we have been speaking of regrading getting global growth in gear still lie ahead and have not been diminished by one better-than-expected job report out of the U.S.

Social distancing is going to impede commerce in a number of businesses. There are still questions about how fast leisure and restaurants and movie theater businesses will be coming back. If many of the labor-intensive and customer-contact-intensive businesses are slow to come back that will have repercussions for how growth will evolve. In fact, there could easily be a second round of weakness and there is still the risk of a second wave of coronavirus infection. But what people are saying now as they notice how quickly some people came out of lockdown and want to engage in the economy again is that it will not be possible to have second lockdown. People are not ready to be that compliant again. Indeed, in the U.S. the President has already said that. I suppose that would be true in Europe as well. Spain is reported to be seeing a surge in consumer spending with its lockdown restrictions just recently modified.

I expect that the coronavirus works the same way in Europe as it does anyplace else. What we know about it is that it kills people with preexisting conditions and especially people with multiple conditions. Doctors have learned to be not so quick to put people on ventilators. People themselves are better about social distancing and being careful so maybe a second wave even if it comes will be smaller and more manageable. The first wave has already taken the most vulnerable population that alone will make countries that have had COVID-19 sweep though more resistant to a second wave.

The U.S. reports remind us to be focused on the release date when we look at economic reports. The U.S. is good at getting economic data out topically. We can now begin to expect some more upbeat features from data for May and markets will probably build even stronger expectations for June especially since globally the lockdowns are seeing their rules relaxed across Europe and in the U.S. and, of course, for China before all the rest.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief