Global| Feb 05 2021

Global| Feb 05 2021German Orders Log First Drop since April; Orders Fall 1.9%

Summary

German factory orders fell by 1.9% in December, their first monthly drop since April of last year. Of course, orders fell sharply in March and April of last year as the virus struck and struck hard – some places harder than others. [...]

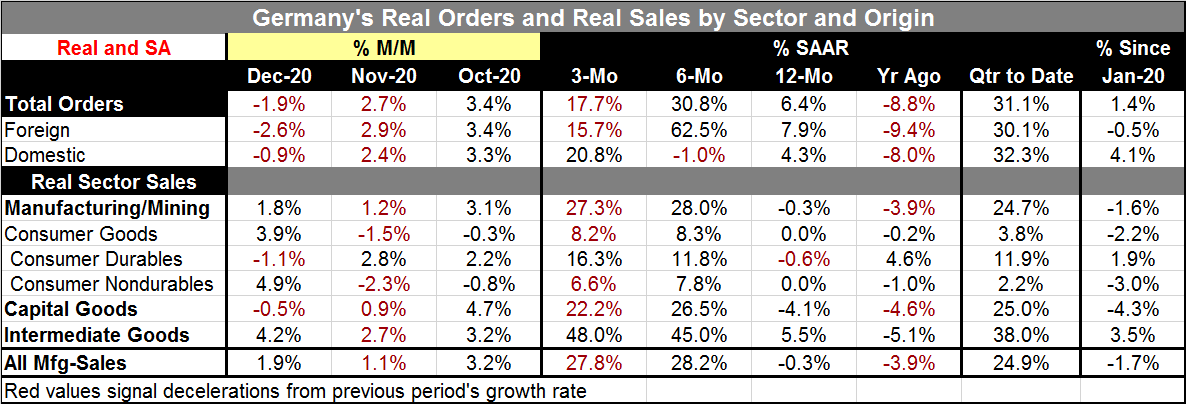

German factory orders fell by 1.9% in December, their first monthly drop since April of last year. Of course, orders fell sharply in March and April of last year as the virus struck and struck hard – some places harder than others. And that virus sucker-punch had come during a period in which German monthly orders had only risen in nine of the last twenty-eight months. However, even with the long string of uninterrupted increases in orders from April 2020 through November, orders are up by only 1.4% since January of last year just before the Covid-19 crisis began disrupting economic data. Foreign orders are down by 0.5% on that period while domestic German orders are up by 4.1%.

German factory orders fell by 1.9% in December, their first monthly drop since April of last year. Of course, orders fell sharply in March and April of last year as the virus struck and struck hard – some places harder than others. And that virus sucker-punch had come during a period in which German monthly orders had only risen in nine of the last twenty-eight months. However, even with the long string of uninterrupted increases in orders from April 2020 through November, orders are up by only 1.4% since January of last year just before the Covid-19 crisis began disrupting economic data. Foreign orders are down by 0.5% on that period while domestic German orders are up by 4.1%.

In December German foreign orders fell by 2.6% on the back of having risen by 2.9% in November. German domestic orders fell by 0.9% in December after a 2.4% rise in November.

Sequential growth rates are not particularly telling because the 12-month, six-month and three-month periods chop the calendar into odd pieces surrounding the impact and revival of the virus crisis and recovery. However, over 12 months, German total orders, domestic orders and foreign orders, all are higher. Over the recent three months, orders also carry strong double-digit annualized growth despite the step back in December. January is going to be another month of having a lockdown in place and half of February will be like that as well. German data may have some rough sledding ahead although the manufacturing sector tends to be less hard-hit than services during these episodes.

The year is ending strongly for Germany despite the December setback in orders. In Q4, orders are rising at a 31.1% annualized rate with foreign orders up at a 30.1% annualized rate and domestic orders advancing at a 32.3% pace. Strength is apparent and well distributed in the fourth quarter.

Overall real sales and real sales by sector also have been strong. In December, manufacturing sales rose by 1.9% led by a 4.9% surge in consumer nondurables and a 4.2% gain in sales of intermediate goods. Capital goods sales backtracked in December as did sales of consumer durables.

Over three months, sector sales are almost eye-popping with consumer goods sales up by a ‘pedestrian’ 8.2% pace while capital goods expanded at a 22.2% annual rate and intermediate goods blew the doors off with a 48% annual rate surge.

Unlike orders, manufacturing real sales grew at a nearly identical pace over three months to the pace over six months: the three-month annualized growth rate is 27.8% compared to a pace of 28.2% over six months. These rates of change contrast sharply with a 0.3% drop in sales over 12 months.

In the just-completed fourth quarter (Qtr to Date column), manufacturing sales are up at a 24.9% annual rate, pretty much in step with the rise in orders. Gains are skewed to intermediate goods (38%) and capital goods (25%) while consumer goods sales rose at a solid, if much weaker, 3.8%.

While orders are stronger when compared to January 2020, real sales are still lagging their January level by 1.7%. Capital goods at -4.3% are the biggest drag on sales, followed by consumer goods at a 2.2% drop. Intermediate goods sales are up by 3.5% vs. January 2020.

The German data show that Germany has been in a funk when the Covid-19 crisis struck. The German economy was hit hard by the virus, but then it recovered sharply and then it continued to repair itself steadily. However, with the new wave in the virus having spread at yearend and early in 2021, the German economy took it on the chin again in December and there may be more setbacks ahead.

Moreover, Germany trades a lot within the EMU and also with now EU-outsider U.K. whose trade flows are clearly disrupted by the new Brexit processes and the demand for endless EU-required red-tape. The extent of the virus spread in the EMU and the U.K. as well as Brexit-specific distortions could continue to be issues for German exports over the next two months –and thereby become a problem for German orders and sales. The last seven months were a breath of fresh air for German manufacturing despite having to deal with Covid-19 issues. Orders expanded monotonically overall and with only one month of interruption for both domestic and foreign orders during that period. However, now the going is going to get tougher.

The hard economic times also have opened political schisms in various places. The U.S. is famously divided politically in part because of what the virus did to the economy as well as to its impact on elections. In Europe, the impact has been especially great in Italy where Mario Draghi is trying to form a new government without the inclusion of the Five-Star Movement, apparently. Portugal has been hit every hard by the virus, but it may be seeing the light at the end of the tunnel. The U.K. lockdowns drag on and there is lots of political blame-man-ship going on there. And the EU, looking to a brighter future with the vaccines distributed, has laid an egg when it comes to having secured enough supply to feed its ambition. There is a lot of finger pointing in the EU these days over that SNAFU. All of these elements are going to affect growth in Europe. And with Germany a heavily export-dependent economy, there are repercussions there for Germany.

While markets are running up stock values globally, and the U.S. is seeing the Democrats preparing to ram through what stimulus they can by going it alone, there is optimism that policies are being geared to keep the global expansion running. And while there are flare ups and signs of some inflation pressure – not to ignore oil that is over $60/barrel for the first time in quite a while- central bankers see only episodic pressures and have no fear of inflation apart from some potential supply-induced run-ups as supply chains reorient themselves to a new reality. You should do that too…reorient yourself to a new reality.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief