Global| Oct 07 2009

Global| Oct 07 2009German Orders Growth Extended

Summary

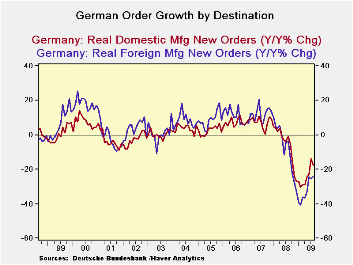

Order Trends: German new orders growth was extended as foreign orders snapped back after a one-month decline. Domestic orders fell by 1.9% after surging by 9.5% in July. Orders have been rising steadily, strongly, over the past six [...]

Order Trends: German new orders growth was

extended as foreign orders snapped back after a one-month decline.

Domestic orders fell by 1.9% after surging by 9.5% in July. Orders have

been rising steadily, strongly, over the past six months with domestic

orders up in five of those six months and foreign orders up in four of

those six months. Both series are showing continuing acceleration not

just growth. In the current quarter domestic orders are outpacing on

the back of a one month 9.5% spurt in orders in July as the new quarter

began.

Foreign order sources: Orders from

countries outside the euro zone alone jumped 5.9%, in August while

foreign demand for German manufactured goods from the other 15

countries sharing the euro rose by just 2.8% in August from the month

earlier. Growth outside of the e-Zone drove German orders this past

month.

Euro-Area policy cuts no slack - Apart

from orders, the European Commission Wednesday warned nine countries,

including Germany, that their budget deficits are too large. This is

the legacy effect of having used domestic deficit spending to bolster

the economy in the recession. That policy response was good thing, but

it now puts those countries afoul of EU Commission rules.

Out of touch with reality? The warning

comes at an odd time since Euro-central bankers and policy officials in

the US have underscored that the time is not right to withdraw

stimulus. Hanging the ‘Sword of Damocles’ over the heads of the various

ECB nations does not seem like the right policy tilt to encourage them

to keep their stimulus efforts in place. It sounds a lot like pressure

to get you house in order NOW! The EU Commission is using bad judgment

and being too strict on rules of evaluations at a time like this. Yes

it is just this sort of thinking that keeps the euro strong but it also

unduly complicates and hampers policy. This stance reminds me of the

ECB’s problems in cutting rates in timely fashion in the recession. The

target rate ceiling on the HICP hampered the ECB in the pits of the

crisis. It cut rates as a part of an ‘international effort’, using that

as an excuse to cut rates with headline inflation well over its ceiling

at the time. I suppose we are to understand that this warning from the

EU Commission as a formality that has come as scheduled. But in times

such as these what is the merit? Does this act brand the EU Commission

tough or as out of touch?

| German Orders and Sales By Sector and Origin | ||||||||

|---|---|---|---|---|---|---|---|---|

| Real and SA | % M/M | % Saar | ||||||

| Aug-09 | Jul-09 | Jun-09 | 3-Mo | 6-Mo | 12-Mo | Year Ago | QTR-2-Date | |

| Total Orders | 1.4% | 3.1% | 3.8% | 38.7% | 17.8% | -21.1% | -2.4% | 43.7% |

| Foreign | 4.6% | -2.4% | 6.9% | 42.1% | 19.2% | -24.0% | -3.8% | 30.7% |

| Domestic | -1.9% | 9.5% | 0.5% | 35.5% | 16.4% | -17.6% | -0.9% | 59.5% |

| Real Sector Sales | ||||||||

| MFG/Mining | 2.7% | -0.5% | 1.1% | 13.8% | 6.7% | -16.6% | 1.8% | 14.4% |

| Consumer | 0.4% | -0.7% | 0.1% | -0.8% | -0.4% | -8.4% | -3.0% | -4.8% |

| Consumer Durables | 1.6% | 0.5% | -2.6% | -2.3% | -1.1% | -20.6% | -1.8% | 3.8% |

| Consumer Nondurable | 0.2% | -0.9% | 0.5% | -0.8% | -0.4% | -6.2% | -3.2% | -6.3% |

| Capital Goods | 4.2% | -2.0% | 1.4% | 15.4% | 7.4% | -20.9% | 4.8% | 18.7% |

| Intermediate Goods | 2.5% | 1.3% | 1.6% | 23.9% | 11.3% | -16.2% | 1.0% | 22.9% |

| All Manufacturing Sales | 2.6% | -0.5% | 1.2% | 13.8% | 6.7% | -16.9% | 1.9% | 14.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief