Global| Feb 05 2015

Global| Feb 05 2015German Orders Gather Pace: International Orders Lead, As Expected, As ECB Collateral Rules Roil Markets

Summary

The long steady drop of the euro exchange rate is boosting German export orders. German orders rose by 4.2% in December led by foreign orders that rose 4.8% after a moderate 0.9% November drop. Domestic German orders rose by 3.4% in [...]

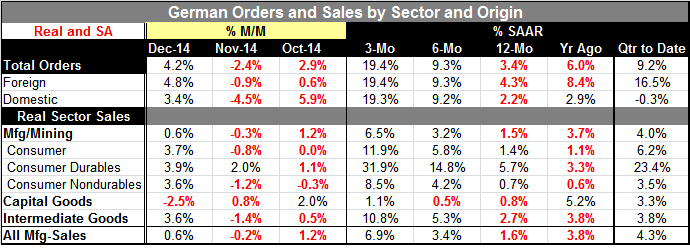

The long steady drop of the euro exchange rate is boosting German export orders. German orders rose by 4.2% in December led by foreign orders that rose 4.8% after a moderate 0.9% November drop. Domestic German orders rose by 3.4% in December after a 4.5% November decrease and a huge rise in October. Domestic orders in Germany have become quite volatile.

The long steady drop of the euro exchange rate is boosting German export orders. German orders rose by 4.2% in December led by foreign orders that rose 4.8% after a moderate 0.9% November drop. Domestic German orders rose by 3.4% in December after a 4.5% November decrease and a huge rise in October. Domestic orders in Germany have become quite volatile.

The year-over-year orders trends show little evidence of much movement. The suggestion of change comes from the sequential growth rates for 12 months to six months to three months where orders of all types show a building acceleration, culminating in growth rates of nearly 20% overall and for both domestic and foreign sectors over three months.

German real sector sales rose nearly across the board in December with a drop in capital goods as the exception. Over three months, German real sector sales are up across the board and they are up on a broad basis over six months as well. The German economy seems to be recovering from the blow it took from sanctions last year and now the low euro seems to be injecting new life-blood into the German export machine.

At the same time, we see troubles linger in Europe. We cannot write about Germany alone today without mentioning the ECB decision to no longer accept Greek bonds as collateral. This decision is almost surely heavily the result of German lobbying and is exactly the sort of thing we expected would follow after the ECB was forced into a QE campaign that Germany opposed.

All these events are connected. The weakness in the euro area is forcing the euro lower and stimulating the German economy, the most efficient economy in Europe. The weakness in the euro area after a prolonged period of austerity left no other choice but unusual ECB monetary intervention which Germany long opposed. In the end, the ECB charter did not `protect the ECB' as much as the Germans thought it would. So now the ECB itself is under pressure and taking extraordinary measures to protect its balance sheet from its own policies (QE) using a unique system of Federalization and of risk demutualization.

Ultimately, German opposition to the large scale QE leads the ECB to adopt this approach where risk sharing would be reduced and where local central banks would do the local QE bond buying on their own balance sheets for QE. The threats from Greece about wanting relief and even the screwy proposal that perpetual bonds (consuls) should/could be issued to replace current Greek paper and give the appearance of eventual full repayment tells us how out of sync European realities are with Greek domestic politics.

My view is that the Germans are no long flexible at all. This is no longer just pro-forma tough German rhetoric. Greece had one bailout and needs to stick to it. There can be no deviating from sanctions and certainly no deviation and a reward for it! I am much more of the mind that a Greek exit is very possible and even likely.

Greek politics tapped into a source of real domestic anger but did not see the resistance in Europe. Germany's discovery that Europe could raid its piggy bank, the ECB, which was supposed to be as protected as the Bundesbank was the game changer. There is no more Mr. Nice Guy from the Bundesbank. Germany has learned that no matter how good it is with inflation and fiscal policy the ECB can be undone by behavior elsewhere in the euro area and that is what will no longer be allowed. This is what is different and has been learned since the last crisis. Germany has realized that bad behavior by others in the euro area puts something it holds dear at risk and that is what it will now act to protect with vigor.

So the German economy will prosper from the weak euro and for everyone else there will be some help from the weakened exchange rate. But strict fiscal rules and no mutualization of monetary risk especially from buying local government bonds will occur. The collateral rule is part of this process given that Greek actions and demands have put the value of Greek bonds into question.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief