Global| Jul 05 2013

Global| Jul 05 2013German Orders Fall Again

Summary

German industrial orders fell by 1.3% in May after falling by 2.2% in April. The May drop marks a two consecutive month drop for overall orders. Foreign orders have fallen for two months in a row as have domestic orders marking the [...]

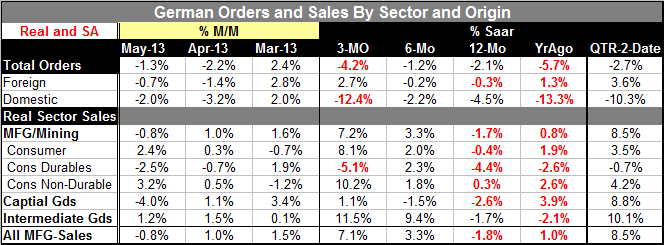

German industrial orders fell by 1.3% in May after falling by 2.2% in April. The May drop marks a two consecutive month drop for overall orders. Foreign orders have fallen for two months in a row as have domestic orders marking the fact that weakness is widespread.

German industrial orders fell by 1.3% in May after falling by 2.2% in April. The May drop marks a two consecutive month drop for overall orders. Foreign orders have fallen for two months in a row as have domestic orders marking the fact that weakness is widespread.

Total orders are down on balance over three months as are domestic orders. However, over three months foreign orders are up at a 2.7% annual rate. Over six months all three categories are lower and over 12 months all three categories are lower. If we look at the evolution of orders in the quarter to date we find the two months into this quarter total orders are falling at a 2.7% annual rate with domestic orders falling at a 10.3% annual rate; but foreign orders are up on balance at a 3.6% annual rate.

German real sector sales show decline in May after several months of increasing. The weakness is concentrated in consumer durable goods and capital goods. In the quarter to date overall manufacturing as well as manufacturing and mining sales are advancing sharply at an 8.5% annual rate. Among the various categories only consumer durables are declining two months into the new quarter - and that of the slow rate of 0.7%.

Orders specifically from the 17 member euro-Zone region declined by 3.9% Orders form the euro-Zone appear to be an important source of weakness in May. Although some data have showed that there is some degree of a firming in the Zone on this horizon, on balance German industrial orders don't reflect that. Germany is still the most competitive country in the Eurozone. If there is business in the Zone for anyone there's business there for Germany. Weak German orders from other EMU members is not an encouraging sign.

The threats and weakness that have been worrying markets in the past few days concerning Portugal seem to have dissipated. Portugal has been able to keep its coalition together. Wolfgang Schaeuble, Germany's finance minister, has puts aside concerns about the political stalemate in Portugal. He is arguing that the euro-Zone is seen as stable and at these political tensions will not mean another crisis for the euro.

Still the Eurozone is struggling with growth. The IMF is wary of the recovery in the euro-Zone's third-largest economy, Italy. The IMF has downgraded its growth outlook for Italy looking for gross domestic product to shrink by 1.8%, a deeper decline in its previous estimate of a 1.5% drop. It looks the economy to expand by 0.7% in 2014, a slight improvement from its previous 2014 estimate of a gain of 0.5%.

The decline in industrial orders in Germany that was unexpected comes one day after the German industry group VDMA has reported weaker orders for machine tool products. This recent dip in Germany comes amid the appearance of some stability in the other countries. That signal has to be taken with some degree of skepticism given the fresh evidence of a faltering German economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief