Global| Aug 06 2018

Global| Aug 06 2018German Orders Drop 4% in June, the Largest Drop Since January 2017

Summary

Orders Drop in Five of Last Six Months; Is the Weakness Over Or Is It Just Beginning? Germany’s orders last dropped more than 4% in a month in January 2017. This time a 4% drop in June comes after a 2.6% gain in May. But this is no [...]

Orders Drop in Five of Last Six Months; Is the Weakness Over Or Is It Just Beginning?

Orders Drop in Five of Last Six Months; Is the Weakness Over Or Is It Just Beginning?

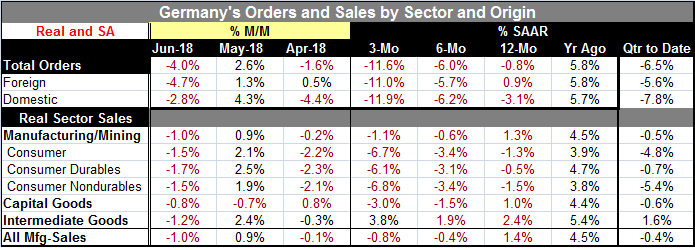

Germany’s orders last dropped more than 4% in a month in January 2017. This time a 4% drop in June comes after a 2.6% gain in May. But this is no ‘one month reversal’ story. German orders have fallen in five of the last six months. The chart shows clearly that orders are in a substantia cooling mode. The ramp up in orders experienced from 2016 through late-2017 is over. The bloom is off both the foreign order trend and the domestic order trend. Real domestic orders have been bracketing the zero line for five months running. German international orders have been much stronger and only recently have slowed to the near zero mark with a 0.9% gain logged over 12 months in June.

Both foreign and domestic German orders are sequentially declining at decelerating rates of change. Over three months, total orders as well as domestic and foreign orders all are falling at an annualized pace of 11% or more. In the quarter-to-date, orders are falling at a 6.5% annual rate and they are ending the quarter on an even weaker note. Growth in June, measured over the Q2 average, is at a -10.7% annual rate. Weak growth is being inherited at the outset of Q3 on top of the weakness in Q2.

Weakness is also apparent in German real sales in June; sales show declines over one month, over three months and over six months. Total sales rose by 1.3% over 12 months, but their pace still decelerated from what it had been one year ago. For consumer goods (durables and nondurables) and capital goods, sales are declining and decelerating from 12-month to six-month to three-month. Only intermediate goods sales show any sign of growth.

This is a great deal of weakness in the German industrial profile. Both sales and orders are weak. German real orders tend to lead German real sales by about 2 months. However, there is a counter-point. The IHS-Markit manufacturing PMI for Germany has actually stabilized in July after it ended a sharp ratcheting lower from a peak reached at yearend 2017. The PMI gauge still leaves the overall PMI level well above the levels that had prevailed in Germany during most of 2015 and 2016. That may be the reason for some complacency in the markets in terms of reactions to this month’s report on real orders. There is no way to sugar-coat the real orders report; it is simply bad and weak. The real question though is this: “What does it mean?”

This is a great deal of weakness in the German industrial profile. Both sales and orders are weak. German real orders tend to lead German real sales by about 2 months. However, there is a counter-point. The IHS-Markit manufacturing PMI for Germany has actually stabilized in July after it ended a sharp ratcheting lower from a peak reached at yearend 2017. The PMI gauge still leaves the overall PMI level well above the levels that had prevailed in Germany during most of 2015 and 2016. That may be the reason for some complacency in the markets in terms of reactions to this month’s report on real orders. There is no way to sugar-coat the real orders report; it is simply bad and weak. The real question though is this: “What does it mean?”

The fall in real orders in five of the last six months with ’balanced weakness’ in both domestic and foreign orders is a disturbing result. The companion slide in the manufacturing PMI gives the weakness signal authenticity. But the fact that the PMI which is one-month fresher shows decline is rearrested in July is an important ingredient. If the weakness is going to stop that abruptly, then this is just an unwinding of unsustainable strength. The chart shows that there has been substantial agreement between the German manufacturing PMI and the real orders series. They are not clones of one another, but their signals have been mutually compatible. One is plotted as a diffusion index and as a level, the other as a 12-month percentage change.

Maybe the German economy has been through a cooling off period and it is going to segue into a period of lower growth ahead. That is what we are going to be looking for. Without the benefit of the advance PMI readings, our fears would up a notch or two... or three.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief