Global| Oct 06 2014

Global| Oct 06 2014German Orders Dive Lower

Summary

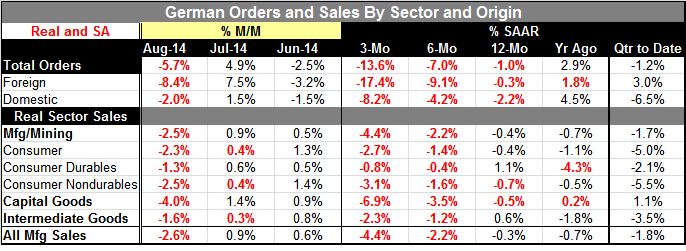

German new orders, seasonally adjusted and expressed in real terms, fell sharply in August. They are falling over horizons of three months, six months and 12 months. The August decline in orders of 5.7% was led by an 8.4% decline in [...]

German new orders, seasonally adjusted and expressed in real terms, fell sharply in August. They are falling over horizons of three months, six months and 12 months.

German new orders, seasonally adjusted and expressed in real terms, fell sharply in August. They are falling over horizons of three months, six months and 12 months.

The August decline in orders of 5.7% was led by an 8.4% decline in foreign orders and aided by a 2% drop in domestic orders.

Total orders have fallen in two of the past three months, as well as in three of the past four months. Over three months, orders are declining at a 13.6% annual rate, steeper than their 7% annual rate drop over six months and steeper than the 1% drop over 12 months. The declining pattern in these growth rates is clear.

Foreign orders fell by a substantial 8.4% in August after a slightly less substantial rise of 7.5% in July and a 3.2% drop in June. Foreign orders have the same decelerating patterns as overall orders; they contracted at a 17.4% at an annual rate over three months, at a 9.1% annual rate over six months, and at a 0.3% annual rate over 12 months.

German domestic orders are slightly less volatile but follow the same general patterns as for total orders and foreign orders. Domestic orders fall by 2% in August after a 1.5% increase in July and a 1.5% decline in June. The three-month growth rate shows an 8.2% decrease, weaker than their 4.2% rate of decline over three months and their 2.2% rate of decline over 12 months.

The pattern for German orders is quite clear in overall orders and supported by trends in foreign and domestic orders. The path is to weakness. In the quarter to date, a slightly different calculation, as we are two months into the current quarter, we calculate the growth rate over these two months compared to the previous quarter's average level. On this basis, orders are falling at 1.2% annual rate in the third quarter with foreign orders rising at a 3% annual rate and domestic orders falling at a 6.5% annual rate.

German real sector sales echo many characteristics in the trends for orders. Sales fell across all categories in August (check). Sales were positive in all categories in July but were showing smaller increases than the absolute value of the declines in August (check). However, sales also increased in June across all categories, unlike orders (no check). When we turn to the sequential growth rates, real sector sales across all categories are falling over three months and without exception are falling faster over three months than they are falling over six months (check, check). Over 12 months, sales are falling in most categories, but rising for only two of them, namely consumer durable goods and intermediate sector goods (mostly another check).

It's hard to get an exact grip on the effect of the sanctions on the euro area and its members, partly since Russia seems to be in denial about how it's being affected. In the last purchasers survey from Markit, the Russians managed to report an increase in activity that seemed highly unlikely to me. Since the Russians have been lying to us on the political front about their actions and interventions in Ukraine, it seems likely that there also lying to us about their economic data. In addition, without making any statements, the Russians are generating energy delivery shortfalls across Europe with their pipeline. They are trying to seem invincible while destabilizing Europe in a subtle fashion.

The Russian stock market rebounded overnight along with the European data partly in sympathy with the stronger-than-expected U.S. employment report from Friday that helps to reassure investors about there being still growth in the U.S. and perhaps globally. But other news reports tell of the problems with sanctions in Russia and of the struggle that Putin is having with his inner circle over some hard economic decisions that have to be made. The Russian stock market may bounce, but there is likely very little follow-up in store.

One ominous point to keep in mind is that Germany is embedded in the euro area as the euro has been falling. That should have been increasing the competitiveness of all countries in the euro area versus areas outside of the euro area. Despite that, we get this extremely weak report from Germany on the performance of its orders with foreign orders slipping even faster than domestic orders. At some point, we would expect the weakening euro to have some positive impact on export competitiveness across the euro area. Germany's data today suggest that's not happening yet and since Germany has run the lowest inflation rate in the euro area since it was formed, that means that Germany's competitiveness flash point will come ahead of that of the area as a whole.

The chart on the left is a PPP calculation of the euro using the values of member-currencies and their local inflation rates before the currency union was formed and using the euro, thereafter. It shows us the inflation-adjusted euro exchange value relative to the trade-weighted inflation-adjusted exchange rate of its trade partners. The horizontal line is the average for the PPP (Purchasing Power Parity) value. If markets value exchange rates correctly over a long period of time the real effective exchange rate's average (which is what is plotted in the chart as a horizontal line) is a measure of the proper value of the currency (its PPP value). By this metric, the euro has been too strong since 2004 having been below parity only briefly on two separate occasions since then. Despite the euro's current drop, it is only now approaching parity again - and still has a way to go to reach it.

The chart on the left is a PPP calculation of the euro using the values of member-currencies and their local inflation rates before the currency union was formed and using the euro, thereafter. It shows us the inflation-adjusted euro exchange value relative to the trade-weighted inflation-adjusted exchange rate of its trade partners. The horizontal line is the average for the PPP (Purchasing Power Parity) value. If markets value exchange rates correctly over a long period of time the real effective exchange rate's average (which is what is plotted in the chart as a horizontal line) is a measure of the proper value of the currency (its PPP value). By this metric, the euro has been too strong since 2004 having been below parity only briefly on two separate occasions since then. Despite the euro's current drop, it is only now approaching parity again - and still has a way to go to reach it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief