Global| Feb 06 2014

Global| Feb 06 2014German Order Strength Fades in December

Summary

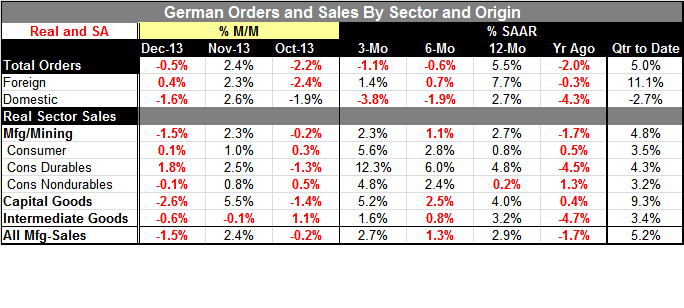

In December, German orders fell by 0.5%. Foreign orders rose by 0.4%, a deceleration from November's 2.3% gain. The real culprit in the weakness of orders, however, is domestic demand. German domestic orders fell by 1.6% in December [...]

The trends in German orders are depressing. Over 12 months orders are up by 5.5%; over six months they are falling at a 0.6% rate; over three months they are falling at a 1.1% annual rate. German orders have progressively become weaker and weaker.

Foreign orders are part of this but not the biggest culprit. Foreign orders are up by 7.7% over 12 months. That growth simmers down to 0.7% over six months and it reaccelerates mildly to a 1.4% pace over three months. It is not much of acceleration, but the constant deceleration is not present in foreign orders although the pattern is still far less than reassuring.

Domestic orders show a clear and very disconcerting pattern of weakness. Over 12 months domestic orders are up 2.7%; over six months they are falling at 1.9% annual rate; over three months they are contracting at a 3.8% annual rate - and this was supposed to be Europe's most solid economy.

In the quarter to date, orders are nonetheless growing. The overall pace is 5% annualized. This growth is led by an 11.1% annual rate increase in foreign orders. But it is accompanied by a 2.7% annual rate decline in domestic orders.

German real sector sales patterns are not as weak as the overall orders pattern. For all the manufacturing sales growth rates go from 2.9% over 12 months, to a 1.3% pace over six months and back up to a 2.7% pace over three months. Even so manufacturing declines in sales occur in two of the last three months.

Sales are positive for consumer goods, capital goods and intermediate goods over three months, over six months and over 12 months. Consumer goods real-sector sales are actually improving from a 0.8% pace over 12 months to 2.8% over six months and to 5.6% over three months. Capital goods are relatively steady at 4% over 12 months, a 2.5% pace over six months, and back to a 5.2% pace over three months. Intermediate goods show a little bit of weakness with a 3.2% gain over 12 months, giving way to a 0.8% gain over six months which rebounds to a 1.6% pace over three months.

This foreign order weakness comes, in some sense, out of the blue. Order statistics in winter and around yearend can be somewhat suspect and orders seem to have some special factors embedded in them so that orders data any time of year can be volatile. Nonetheless, patterns in these recent data and their longer-term patterns are perplexing. The GfK consumer climate index continues to climb higher. The German Chamber of Commerce just lifted its outlook for the year ahead. German statistics on the whole tend to be expansionary although far from being ebullient.

Still, Germany and the European Union show that orders, after an early strong romp out of the gate following recession, have continued with their deceleration. German orders now are doing no better than those for the rest of the European Monetary Union despite all the ballyhoo of a strong German economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief