Global| Jul 08 2019

Global| Jul 08 2019German IP Ticks Higher in May

Summary

German IP ticked higher in May, rising by 0.3% month-to-month after a 2% decline in April. German IP is declining over 12 months, six months and three months, but there is no trend deterioration. Growth is not getting progressively [...]

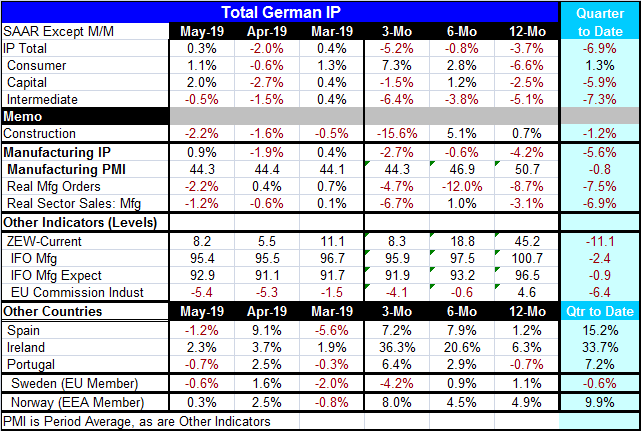

German IP ticked higher in May, rising by 0.3% month-to-month after a 2% decline in April. German IP is declining over 12 months, six months and three months, but there is no trend deterioration. Growth is not getting progressively weaker, but IP does continue to fall. The fall over 12 months is at a -3.7% pace and over three-months it is at a faster -5.2% annual rate.

German IP ticked higher in May, rising by 0.3% month-to-month after a 2% decline in April. German IP is declining over 12 months, six months and three months, but there is no trend deterioration. Growth is not getting progressively weaker, but IP does continue to fall. The fall over 12 months is at a -3.7% pace and over three-months it is at a faster -5.2% annual rate.

Sector trends for IP

The trends for the three principle sectors are complex. Only consumer goods show a clear trend with consumer goods output steadily accelerating on shorter timelines. Capital goods output hints at improvement with an output gain over six months and a lesser pace of decline over three months than over 12 months. Intermediate goods output shows declines on all horizons. The declines are at a sizeable pace on all timelines and the three-month rate of decline is larger than the decline over 12 months. Intermediate goods hint at a worsening trend. On balance, industrial production is not easy to pin down to establish a trend. Manufacturing shows the same complex patterns with slightly less of a decline over three months compared to 12 months.

Markit PMI and other indicators

The Markit manufacturing PMI has worked lower but has been declining more slowly even though it has remained below 50 since January. Manufacturing output has been declining year-over-year since November of last year. So the PMI and the IP results are more or less in step. Real manufacturing orders haves been declining on all horizons, but their rate of contraction has been slowing with an 8.7% pace of contraction over 12 months giving way to a pace of -4.7% over 3-months. Real sales, however, have the opposite pattern with declines over three months and 12 months and the larger rate of decline over three months.

Major German surveys

All the major German surveys, ZEW, IFO-MFG, IFO-MFG-expectations and the EU Commission MFG index for Germany show a clear and sizeable ramping down of momentum from 12-months to six-months to three-months. IFO expectations show some stabilization and even bounced higher over the last two months (March-to-May). The ZEW survey shows some improvement in May relative to April. The EU Commission index that fell sharply in April has nearly the same reading in May.

Quarter-to-date

On a quarter-to-date basis, nearly all the German metrics are showing deterioration compared to their averages of the previous quarter. Consumer goods output is the sole exception. Manufacturing output is falling especially hard in Q2 compared to Q1. The indicators all show substantial negative values indicating deterioration compared with their Q1 levels.

IP elsewhere in Europe

Other early European reporters generally show some IP pickup. Spain, Ireland, Portugal and Norway generally show improvement while Sweden shows deterioration in progress. All of these countries also show quarter-to-date improvement as well except for Sweden.

Summary

Despite the month’s gain in output, trends for Germany are complex. But on balance, they still show ongoing declines. There are mostly declines and weakness over three months and 12 months as well as quarter-to-date. The indicators that hint at stabilization in June show clear deterioration over all other periods. One or even two months is too short of an ‘observation’ to have much impact on thinking. There is little here for the ECB to like.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief