Global| May 08 2013

Global| May 08 2013German IP Rises; Makes Gain in Q1

Summary

German industrial production surprisingly rose by 1.2% in March building on a gain of 0.6% in February. These are the two first back-to-back gains in industrial production since April and May 2011 - and these gains are larger. These [...]

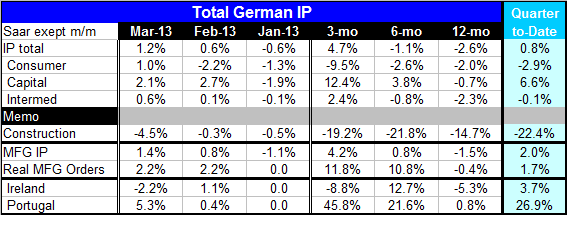

German industrial production surprisingly rose by 1.2% in March building on a gain of 0.6% in February. These are the two first back-to-back gains in industrial production since April and May 2011 - and these gains are larger. These advances cause industrial production to advance by 0.8% in the first quarter over the fourth quarter putting industrial production in the clear growth trajectory in the first quarter 2013. The main reason for this rise, is the contribution to output from capital goods. Capital goods output is up at a 6.6% annual rate in the first quarter over the fourth quarter base while consumer goods output is declining at a 2.9% annual rate and intermediate goods output is declining at a thin 0.1% annual rate.

German industrial production surprisingly rose by 1.2% in March building on a gain of 0.6% in February. These are the two first back-to-back gains in industrial production since April and May 2011 - and these gains are larger. These advances cause industrial production to advance by 0.8% in the first quarter over the fourth quarter putting industrial production in the clear growth trajectory in the first quarter 2013. The main reason for this rise, is the contribution to output from capital goods. Capital goods output is up at a 6.6% annual rate in the first quarter over the fourth quarter base while consumer goods output is declining at a 2.9% annual rate and intermediate goods output is declining at a thin 0.1% annual rate.

Construction output fell by 4.5% in March and it continues to be week falling in a 22% annual rate in the first quarter. Isolating manufacturing industrial production rose by 1.4% in March piggybacking on a 0.8% gain in February and is up at a 2% annual rate in the first quarter compared quarter 2012.

We've already seen manufacturing orders rising strongly for two months in a row they are up at a 1.7% annual rate in the first quarter adding to the signal that we see from industrial production this month.

The euro-Zone continues to struggle ahead through difficult times. The French economy has been getting weaker. The Italian economy is beginning to deal with some of its political difficulties but so far it seems only to have a temporary solution. Spain and France have been given some extra time to reach their respective budget deficit goals, that could take some pressure off of them in the near-term. But by and large economic activity is still struggling and Germany continues to emit the firmest signals among the countries in the Eurozone. The question is this: "Is the German economy really getting better?"

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief