Global| Nov 06 2020

Global| Nov 06 2020German IP Recovery Progresses

Summary

German industrial output rose by 1.6% in September, faster than its 0.5% rise in August, keeping the expansion in output and recovery on track. German output is accelerating from 12-months to six-months to three-months and it is [...]

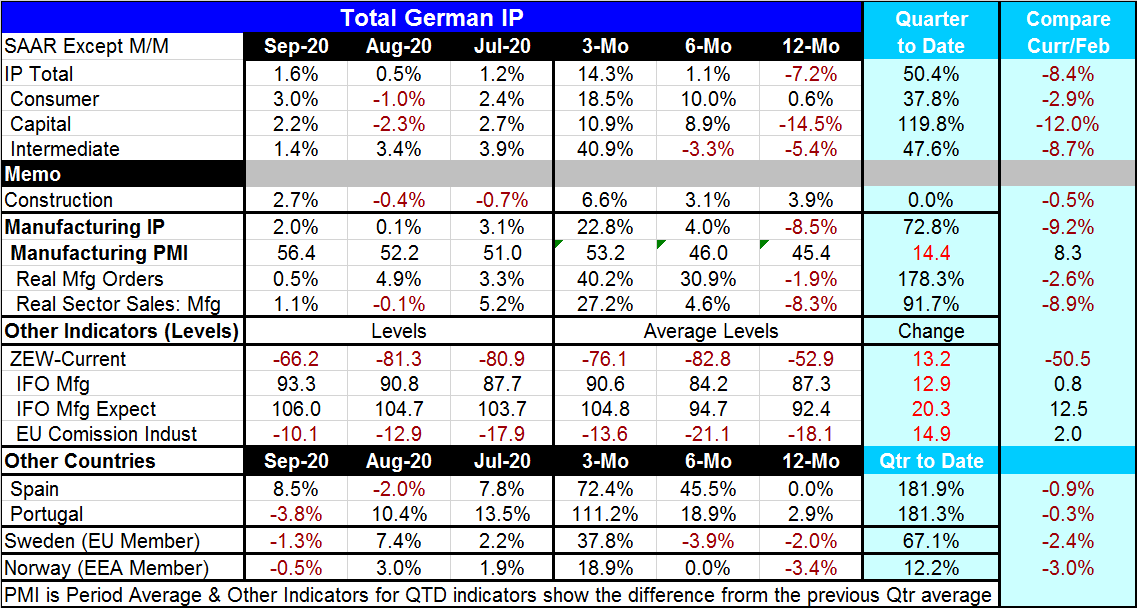

German industrial output rose by 1.6% in September, faster than its 0.5% rise in August, keeping the expansion in output and recovery on track. German output is accelerating from 12-months to six-months to three-months and it is expanding in the just completed third quarter at a very robust 50% annualized rate. It is still a recovery in progress despite those strong figures as the level of output in October is 8.4%% below where it stood in February.

German industrial output rose by 1.6% in September, faster than its 0.5% rise in August, keeping the expansion in output and recovery on track. German output is accelerating from 12-months to six-months to three-months and it is expanding in the just completed third quarter at a very robust 50% annualized rate. It is still a recovery in progress despite those strong figures as the level of output in October is 8.4%% below where it stood in February.

Sector recovery is afoot

All three sectors consumer goods, capital goods and intermediate goods have output lower than their respective February levels. Manufacturing as a whole has output lower by 9.2%. Construction sector output is lower by 0.5%. However, all three sectors and manufacturing as whole show output is accelerating from 12-months to six-months to three-months. Construction output is not quite on that same path, but its pace over three months is faster than over 12 months.

Manufacturing, real sector sales, and the Markit manufacturing PMI all show progressive acceleration for manufacturing, underpinning this notion of ongoing recovery. The Markit manufacturing PMI is even stronger in September than it was in February, showing essentially a 'complete' recovery.

Other metrics show substantial progress

A few indicator metrics also chime in with stronger readings for September than in February. This includes the IFO for manufacturing, the IFO manufacturing expectations index, and the EU commission industrial index. These indexes, which are formally more about breadth than strength, indicate that the breadth of the expansion has progressed faster than its strength. We know this since the IP itself measures strength and manufacturing is lower by 9.2% from its February level.

Elsewhere in Europe

There are also four other early reporters of IP results in Europe. Of these four, only Spain shows a rise in IP in September as Portugal, Sweden and Norway log declines on the month. However, all but Sweden still show progressive acceleration from 12-months to six-months to three-months. All show strong growth in the quarter as well. Norway's IP growth is 'strong' but not on a par with the other economies listed here. And all four show that IP in September is below its level as of February but by smaller percentages than Germany ranging from a shortfall of 3% in Norway to a shortfall of just 0.3% in Portugal.

As always the future is about the virus...

Of course, the way forward depends less on the statistics of momentum in the table and more on the virus which has spread again and is requiring widespread counter-policies across Europe. In this process manufacturing tends to be less affected than the service sector yet it, too, will be affected by the reductions in activity.

Everyone is watching and waiting to see how effective these more limited closures will be is stopping the spread compared to early in the year when they fell like a hammer blow and knocked the global economy out. There is every effort being made to avoid that this time around but still the policy aim is to block the spread – that has not changed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief