Global| Nov 07 2014

Global| Nov 07 2014German IP Rebounds in September but Sinks in the Quarter

Summary

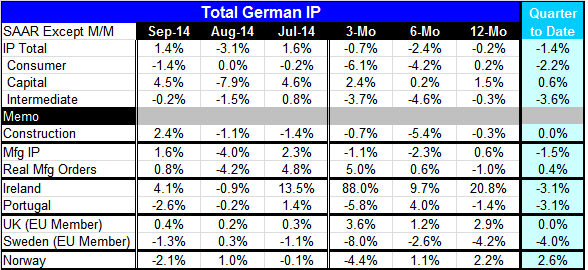

German industrial production rose by 1.4% in September, offsetting part of the 3.1% August decline. Over three months, output is declining at a 0.7% annual rate, not quite as bad as a 2.4% annual rate drop over six months, but the [...]

German industrial production rose by 1.4% in September, offsetting part of the 3.1% August decline. Over three months, output is declining at a 0.7% annual rate, not quite as bad as a 2.4% annual rate drop over six months, but the drop has accelerated from the 0.2% decline over 12 months. The bad news is that industrial production in Germany is steadily declining over all these horizons. The good news is that the acceleration did not pick up pace over the last three months.

German industrial production rose by 1.4% in September, offsetting part of the 3.1% August decline. Over three months, output is declining at a 0.7% annual rate, not quite as bad as a 2.4% annual rate drop over six months, but the drop has accelerated from the 0.2% decline over 12 months. The bad news is that industrial production in Germany is steadily declining over all these horizons. The good news is that the acceleration did not pick up pace over the last three months.

However, the pace of decline did accelerate for consumer goods as output fell by 1.4% in September and sequential growth rates see consumer output falling from 0.2% over 12 months to -4.2% over six months and to -6.1% at an annual rate over three months. Intermediate goods output is not exactly steadily decelerating, but the pattern is not reassuring either, with a -0.3% pace over 12 months and an accelerated drop to -4.6% over six months then with the pace of decline abating slightly, declining at a slightly blunted, but still steep -3.7% over three months. That drop is less than the pace of decline over six months but much greater than the declining pace over 12 months. Capital goods output trends are erratic and a little bit more positive. They are growing 1.5% over 12 months, gaining just 0.2% over six months but then rising at a 2.4% annual rate over three months.

Manufacturing output bounced back in September, rising 1.6% after falling 4% in August. Its trend is eroding but not with acceleration; it shows a 0.6% gain over 12 months, a 2.3% annual rate drop over six months, and that drop is trimmed to-1.1% over three months.

Construction output rebounded strongly in September, rising 2.4% after falling 1.1% in August. It has negative growth rates over three months, six months and 12 months, but it does not have a steady decelerating pattern.

Looking at German real manufacturing orders to assess the future, we see that orders rose by 0.8% in September following a 4.2% decline in August. The pattern for orders is actually an accelerating pattern as orders are down 1% over 12 months, rising at a 0.6% pace over six months and at a 5.0% annual rate over three months. The orders data suggest that this slowdown and contraction is going to be reversed.

On a quarter-to-date basis, however, German output is still falling, dropping by 1.4% at an annual rate in the third quarter, led by a 3.6% annual rate of decline in intermediate goods and a 2.2% annual rate of decline in consumer goods. This set of declining forces is blunted somewhat by a 0.6% gain in capital goods. Construction sector output in the quarter is flat. Manufacturing output alone is falling at a 1.5% annual rate in the third quarter, while real manufacturing orders are up by 0.4%.

Looking at output trends in some of the other European Monetary Union and European Union members that report output early, we see mixed results for September. In Ireland output is up a sharp 4.1%. In Portugal output is down by 2.6%. In the UK output is up by 0.4%, continuing a steady string of increases. Sweden's output is down by 1.3% and Norway's output is off by 2.1%.

Three-month trends in these members show an enormous 88% annual rate gain in Ireland and a 3.6% annual rate gain in the U.K. Sweden shows an 8% annual rate drop. Portugal shows a 5.8% annual rate drop and Norway shows a 4.4% annual rate drop. Over 12 months, Ireland still shows a strong 20% annual rate gain and the U.K. logs a 2.9% annual rate gain. We see declines over 12 months in Sweden at -4.2% and Portugal at -1.4%. Norway turns to a 2.2% gain over 12 months.

We continue to see irregularity in the output trends of the early reporting EMU and EU members. Apart from Ireland and its unique case, we are seeing deterioration or weak growth in most countries. The U.K. is an exception, showing generally steady growth in output.

Economic news lately has not brought many silver linings to the accumulating clouds of bad news. Today's geopolitical news adds to the overcast pallor. There is a report from Ukraine that Russia has sent a column of tanks across the border into Ukraine's territory, potentially setting the stage for renewed conflict. This, I think, is completely predictable as the Russian economy continues to be racked by the effects of sanctions. Russian companies continue to assert their health, but the performance of the ruble on foreign-exchange markets is more telling than any interview with a Russian banker. The more pressure that Russia is made to feel, the more that it is going to want to get in return for its suffering. And that's the bad news for Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief