Global| Jul 07 2014

Global| Jul 07 2014German IP Marks Third Drop in a Row

Summary

German industrial production in May fell for the third month in a row. The trends for overall industrial production are now showing a steady decline from 1.2% over 12 months, to -3.3% over six months, to -10.9% over three months. The [...]

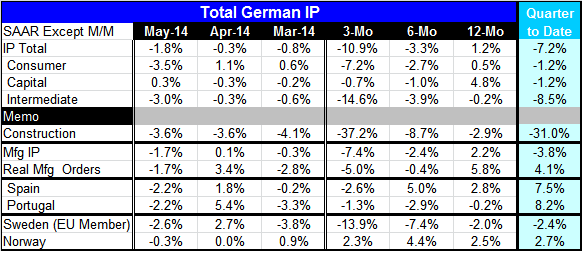

German industrial production in May fell for the third month in a row. The trends for overall industrial production are now showing a steady decline from 1.2% over 12 months, to -3.3% over six months, to -10.9% over three months. The chart of year-over-year trends shows continuing decelerations for consumer goods and intermediate goods with some rebound for capital goods output.

German industrial production in May fell for the third month in a row. The trends for overall industrial production are now showing a steady decline from 1.2% over 12 months, to -3.3% over six months, to -10.9% over three months. The chart of year-over-year trends shows continuing decelerations for consumer goods and intermediate goods with some rebound for capital goods output.

Looking at the sectors in May, consumer goods output fell by 3.5%, capital goods output rose by 0.3% and intermediate goods output fell by 3.0%.

The sequential growth rates show a steady, deepening contraction for consumer goods output. There is a steady and even faster deepening decline for intermediate goods output. For capital goods, growth is still in place over 12 months at a 4.8% annual rate, but over six months that slips to -1%, and over three months it holds at -0.7%. Slippage is evident for all the sectors even though capital goods is proving to be somewhat more resilient.

In the quarter to date, the declines are still virulent. Overall industrial production is declining at a 7.2% annual rate in the second quarter led by an 8.5% annual rate decline in intermediate goods with consumer goods and capital goods both falling at just a 1.2% annual rate.

Construction spending has been even weaker, falling by 3.6% in May and dropping at a 37.2% annual rate over three months on clearly devolving growth rates. In the quarter to date, construction output is falling at a 31% annual rate.

Manufacturing alone shows a descending set of growth rates, culminating in a -7.4% annual rate over three months. This is more or less in step with real manufacturing orders which rose at a 5.8% rate of growth over 12 months and then fell at a -5% annual rate over three months.

Germany is not alone in experiencing some weakness in these recent months. Spain and Portugal, both European Monetary Union members, showed declines of 2.2% each in industrial production in May. Portugal has negative growth rates for output over 12 months, three months and six months. Spain's negative growth rate appears only over three months, at a -2.6% annual rate. However, both Spain and Portugal are growing at solid growth rates in the second quarter on the order of 7.5% to 8%.

Outside of the monetary union, Sweden and Norway showed declines in industrial output in May. Norway's trend is more or less steady with growth rates around 2.5% over 12 months, six months, and three months. However, for Sweden, the growth rates show the now-familiar deteriorating trend. Growth is -2% over 12 months with output declining at a 13.9% annual rate over three months. Sweden shows output declining in the quarter to date at a 2.4% annual rate. Norway has output increasing in the quarter to date at a 2.7% annual rate.

As always, there are countries that will do better and countries that will do worse. But the clear picture that we get this month is that output across Europe appears to have weakened. It's quite surprising to see Germany post three negative growth rates in a row, but that's exactly what it's done. Germany last had three straight months of output declines in November 2012. Germany's weakness is broad-based and supported by a weak trend in orders. Although capital goods is somewhat more resilient, it too is showing declines over both three months and six months.

This obviously is not the environment in which ECB policies that are geared to stimulate credit growth are going to be the most successful. However, this is the background that the ECB has to work with. Conditions in Europe, appeared of taken a turn for the worse.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief