Global| Jul 07 2020

Global| Jul 07 2020German IP Makes First Gain in Three Months: Still Not Impressive

Summary

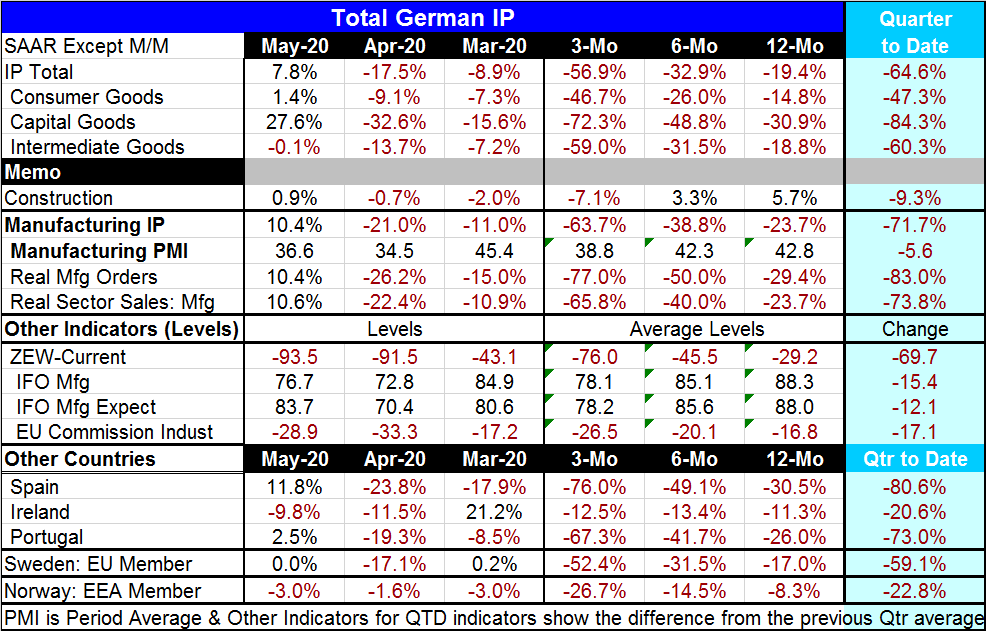

Germany logged its first rise in IP in three months. Even so, the gain was less than expected and the ongoing drop in German IP overall as well as by sector (see graph) remains severe. The EU is preparing some sort of a stimulus [...]

Germany logged its first rise in IP in three months. Even so, the gain was less than expected and the ongoing drop in German IP overall as well as by sector (see graph) remains severe. The EU is preparing some sort of a stimulus scheme and Italian markets are reacting well in anticipation that the programs will embrace grants instead of loans. And the situation may finally be ripe for that. Of course, Italy and several other EMU nations are wary of shipping on more debt as they are close to the Maastricht allowable levels of debt relative to GDP and they do not want to have austerity imposed (ever!) again.

Germany logged its first rise in IP in three months. Even so, the gain was less than expected and the ongoing drop in German IP overall as well as by sector (see graph) remains severe. The EU is preparing some sort of a stimulus scheme and Italian markets are reacting well in anticipation that the programs will embrace grants instead of loans. And the situation may finally be ripe for that. Of course, Italy and several other EMU nations are wary of shipping on more debt as they are close to the Maastricht allowable levels of debt relative to GDP and they do not want to have austerity imposed (ever!) again.

The EU Commission's outlook

The EU Commission has just said that euro area economy will sink deeper into recession than it previously thought due to the effects of the pandemic. It looks for the euro area to contract a record 8.7% this year before growing 6.1% in 2021. This outlook compares with the EC's May forecast of a 7.7% slump and 6.3% growth. The EU Commission claims that its revised forecast comes amid concerns about the U.S. economy after a surge in infections across various U.S. states. Germany, which has had fewer Covid-19 deaths, is expected to log a 6.3% contraction, less pronounced than May's forecast of 6.5%.

There is still uncertainty about the U.K.-EU Post Brexit trading relationship that could alter this outlook. And of course, elsewhere global conditions remain touch-and-go.

The German condition

For now, German IP is rebounding led in the month by capital goods, the sector where output is nonetheless down the most over three months, six months and 12 months. Germany is looking to adopt more stimulus, but it is hampered by the fact that about 60% of German output is exported and depends on foreign demand not on German demand. The difficulty of this situation is compounded by the fact that Germany sells a lot to fellow EU members but at the same time has been a main enforcer of Maastricht rules. Since many EU nations are near their Maastricht debt limits, their ability to use stimulus is limited. That confluence of events comes back to bite Germany. With the German economy still struggling, the economic situation could finally be ripe for Germany to get behind an EU stimulus plan that would deliver grants to members allowing fellow EU members to stimulate their economies without encroaching on their Maastricht parameters.

The quarter-to-date data continue to show there is weakness all around. German sector output, manufacturing as well as construction, all show trends that are still worsening quarter-to-quarter. And German surveys are weakening as well with the ZEW, IFO and EU Commission surveys showing ongoing weakness even in the face of recent strengthening. The Markit manufacturing PMI gauge that is up-to-date though June shows more increase in the PMI gauge in June but still a substantial drop in the Q2 average compared to Q1 for Germany's manufacturing PMI.

Data in the table also show trends for several early reporting European countries and all are showing ongoing and generally deepening weakness over three months compared to six months and 12 months. Ireland is a bit of a contrary case. But even with three of five fellow European nations failing to show output declines in May, the declining profile trends are clear and weak.

Whether Europe should be cutting its outlook because of U.S. trends is debatable. Europe has its own problems with virus flareups and its own institutional impediments including high country debt levels and its own Maastricht rules that limit flexibility as well as the absence of any formal fiscal coordination – apart from preaching constant restraint.

The EMU was formed with safeguards in place to assure monetary policy would be controlled and never inflationary and to see that fiscal abuse would not occur. The formation saw the risk of excess stimulus from the start and there were really no provisions made to combat the prospect of excessive weakness. Now that excessive weakness has proved to be an issue and a repeat issue for several EU members or more, the bloc finds itself without formal tools to deal with it. The hard money Europhiles continue to worry and wring their hands over current ECB policy since its balance sheet is growing and its policy embraces a structure that includes negative interest rates.

Even so, the problem in the EMU and the EU is weakness, not inflation. The ECB has been undershooting its inflation goal for some time and still there is little recognition by the countries with firepower that stimulus is what is missing. But maybe with German growth weak and hogtied to weakness in the rest of the zone a new day is about to dawn. That prospect is worth watching.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief