Global| Jan 09 2014

Global| Jan 09 2014German IP Is on the Mend

Summary

Industrial production in Germany rose by 1.9% in November. This rise reflects a reversal from the decline in October from the drop in September. Over three months industrial production in Germany is now flat; it is rising by 5.4% at [...]

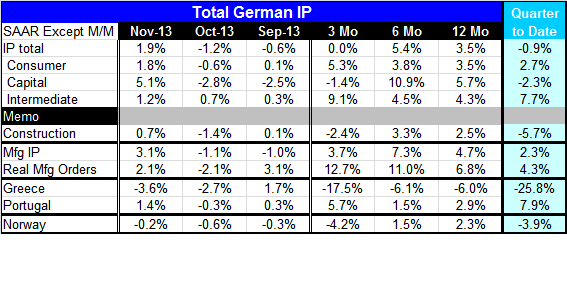

Industrial production in Germany rose by 1.9% in November. This rise reflects a reversal from the decline in October from the drop in September. Over three months industrial production in Germany is now flat; it is rising by 5.4% at an annual rate over six months and by 3.5% at an annual rate over 12 months. In the quarter-to-date, however, industrial output is falling by nearly 1% at an annual rate with the weakness led by the capital goods sector; its output is falling at a 2.3% annual rate.

Industrial production in Germany rose by 1.9% in November. This rise reflects a reversal from the decline in October from the drop in September. Over three months industrial production in Germany is now flat; it is rising by 5.4% at an annual rate over six months and by 3.5% at an annual rate over 12 months. In the quarter-to-date, however, industrial output is falling by nearly 1% at an annual rate with the weakness led by the capital goods sector; its output is falling at a 2.3% annual rate.

All sectors rebounded and posted positive growth in November. Consumer goods output rose by 1.8%. Capital goods output surged by 5.1%, following two consecutive months of substantial drops. Intermediate goods output rose by 1.2%, forming a continuous string of increases. Over three months consumer goods output is rising at a 5.3% annual rate. Capital goods output is shrinking a 1.4% annual rate and intermediate goods continues to rise at a very strong 9.1% annual rate over three months.

Holding output back the most is construction. While construction output rose by 0.7% in November, it fell by 1.4% in October. Over the last three months it is declining at a 2.4% annual rate and quarter-to-date it is dropping at a 5.7% annual rate. Construction is a relatively fickle sector in the winter months. If we exclude construction and focus on manufacturing, the production trend shows a clearer and stronger picture of output in Germany.

Manufacturing output is rising by 3.1% in November after two months of declines. It is making a 3.7% annual rate over the last three months, 7.3% over six months and a 4.7% annual rate over 12 months. In the quarter-to-date, manufacturing production is up at a 2.3% annual rate. Real manufacturing orders continue to point to strength; their three-month growth rate of 12.7% exceeds the six-month growth rate of 11% and their twelve-month growth rate of 6.8%. German orders are plowing ahead and so is industrial production. Those trends appear to continue.

Few EMU members have reported in November although we have another drop recorded for production in Greece and an increase in Portugal. Greece continues to struggle mightily. While PMI data had suggested the manufacturing sector was stabilizing, industrial production shows a sharp drop in November and a 17.5% annual rate of decline in output over the last three months. November's year-over-year percent drop is 6%. Greece's output is declining at a 25.8% annual rate in the current quarter.

Portugal, another country that has been saddled with the burden of austerity, shows a 1.4% rise in industrial production in November. Output in Portugal is growing a 5.7% annual rate over three months, up from 1.5% over six months and up from 2.9% over 12 months. In the current-quarter to-date, output in Portugal is rising at a 7.9% annual rate. Portugal's progress is looking solid and it is encouraging.

Norway, a non-EMU member, shows three consecutive drops in industrial production. Norwegian production is declining at a 4.2% annual rate over three months. Norway shows a steady progression to lower growth rates with its twelve-month growth rate of 2.3%, its six-month pace at 1.5% and a drop of 4.2% over the most recent three-months. In the quarter-to-date output in Norway is falling at a 3.9% annual rate.

On balance, Germany continues to point the way forward. German orders continue to be strong. However, Germany has an export-led growth economy. German strength tends to indicate a pickup in the rest of the world and Germany does not add its own domestic demand stimulus to the mix until later. Of late some German statistics have been mixed, but the industrial sector data are continuing to show expansion. That is a good sign for the European Union and for EMU. However, what we see in the case of Germany is that, while it had a nice rebound in November, its behavior in the quarter-to-date has still not put it in the plus column. The EMU members continue to struggle to get their feet under them and to post solid growth. Europe is still in transition.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief