Global| Feb 08 2021

Global| Feb 08 2021German IP Is Flat in December: Trends Mixed

Summary

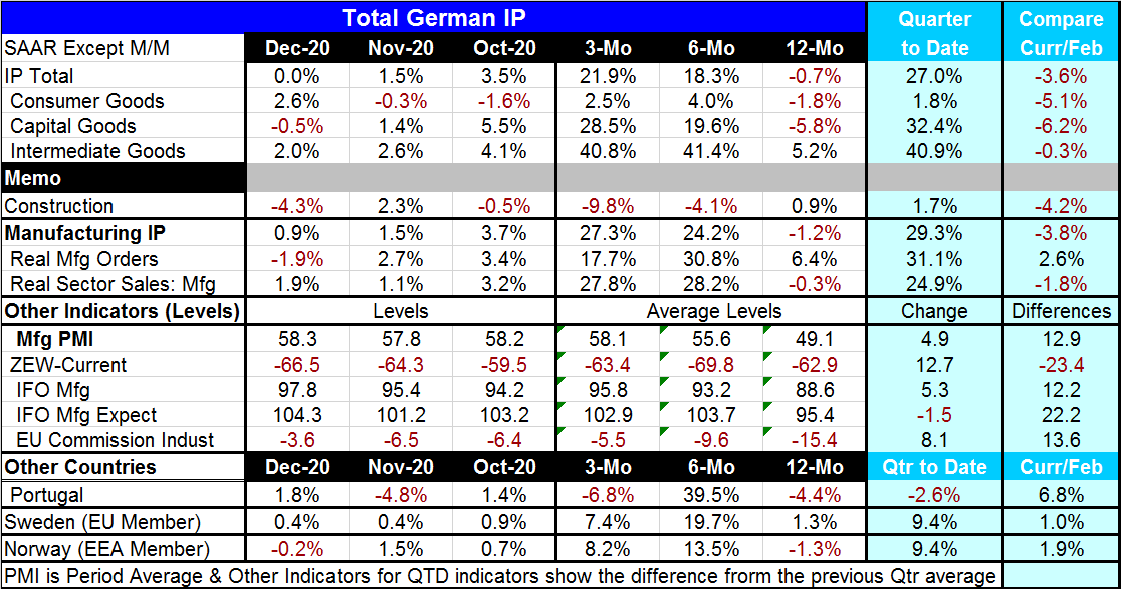

German IP data show several diverse and sometimes opposite trends. The graphic depicts year-on-year growth rates over 12 months and those show conditions that are either steadily improving (intermediate goods) or continuing to show [...]

German IP data show several diverse and sometimes opposite trends. The graphic depicts year-on-year growth rates over 12 months and those show conditions that are either steadily improving (intermediate goods) or continuing to show growth erosion possibly with a touch of an improving trend as well (capital goods and consumer goods).

German IP data show several diverse and sometimes opposite trends. The graphic depicts year-on-year growth rates over 12 months and those show conditions that are either steadily improving (intermediate goods) or continuing to show growth erosion possibly with a touch of an improving trend as well (capital goods and consumer goods).

However, the recent three-month patterns- call this the micro-trend- shows momentum fading to zero in December for the headline with consumer goods gaining as capital goods and intermediate goods trends showing growth erosion.

The sequential growth rates for 12-months to six-months to three-months are more uniformly solid; they show overall acceleration and acceleration for capital goods and a strong progression for intermediate goods. Three-month growth rates are positive overall and strong in each sector, except for consumer goods where growth is positive but quite moderate.

However, construction shows a mixed monthly pattern and a deteriorated sequential pattern.

Manufacturing IP, manufacturing new orders and manufacturing real sales show strong three-month growth rates and generally a progression to more strength.

The manufacturing PMI shows a progression to strength. The current ZEW index shows some slight six-month to three-month improvement on a still deeply negative reading. The IFO manufacturing index shows progressive improvement; manufacturing expectations for the IFO show an improvement to six-months and then a step-back at three-months. The EU Commission gauge shows ongoing improvement amid weak ongoing readings. However, the survey data especially the manufacturing PMI and the IFO expectations have values available for January and those are generally weak or weaker. Into January, the EU Commission index for German industry is an exception and it continues to improve.

Quarter-to-date data now pertain to the completed fourth quarter. Most categories are up on the quarter and most are also quite strong. The exceptions are consumer goods output that is up at only a 1.8% annual rate, construction output that is up at only a 1.7% annual rate and the IFO manufacturing expectations reading that actually backtracks on the quarter.

The survey data show improved conditions in December compared to their levels in February except for the IFO current index. Manufacturing headline and sector readings are mostly still below their February (pre-virus) levels of output. Manufacturing orders are an exception; they are higher.

Gong viral...

And of course much of this is driven by the virus that had been impacting Germany late in December and into the New Year as well. Trends do not matter much because you cannot extend them forward unless the virus permits it. Backward-looking trends mostly document what the virus has done in terms of picking up or simmering down. Not surprisingly, the sequential data show improvements as the economy has built momentum from the early 2020 virus disaster from, roughly, March onward. But the 'micro trend,' monthly, over the last three-months, is more tempered because the virus has been striking again.

The bad news on the day is that in South Africa they have stopped the rollout of the AstraZeneca vaccine because a new study says it is not very effective against the strain of the virus that is circulating and dominant in South Africa. Other countries are going to continue to use it. That event is not a game breaker for Germany in any way, but it is certainly an event to take note of and a warning. The South African strain has spread. "Top Oxford University vaccine researcher Sarah Gilbert said a modified version of the AstraZeneca vaccine that will be effective against the South African strain would likely be available by fall" (Source; for more detail here). Since the future is all about vaccines and how effective they are and how well their roll out can progress, the news from South Africa is chilling as well as the delay in formulating a vaccine that will be effective is a definite turn for the worse on the virus front.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief