Global| Aug 07 2018

Global| Aug 07 2018German IP Falls and German Exports Run Flat

Summary

Germany's industrial production has been oscillating monthly. Output has fallen month-to-month in seven of the last ten months. But IP weakness has been greatest from January to April during this period. As we try to track the impact [...]

Germany's industrial production has been oscillating monthly. Output has fallen month-to-month in seven of the last ten months. But IP weakness has been greatest from January to April during this period. As we try to track the impact of coming trade wars, we look at series like foreign orders, exports and industrial output. For Germany, orders and output track relatively closely and the manufacturing PMI is another of those statistics in the mix that is more volatile than IP.

Germany's industrial production has been oscillating monthly. Output has fallen month-to-month in seven of the last ten months. But IP weakness has been greatest from January to April during this period. As we try to track the impact of coming trade wars, we look at series like foreign orders, exports and industrial output. For Germany, orders and output track relatively closely and the manufacturing PMI is another of those statistics in the mix that is more volatile than IP.

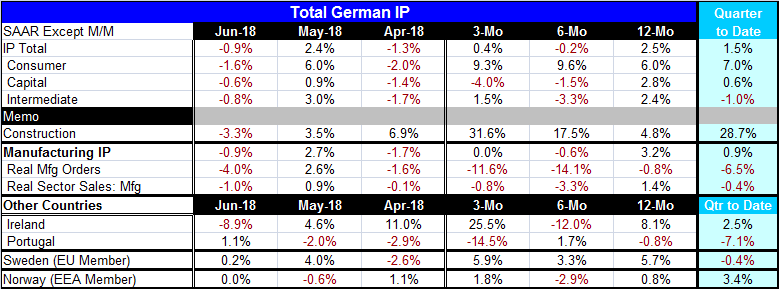

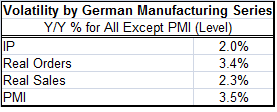

In terms of quantitative measures of volatility over the past four and one half years, we see that IP is the most tranquil of these measures. Year-over-year output gains currently are at 2.5% and year-on-year IP gains have been relatively stable in recent months despite monthly volatility. Manufacturing components show a clear deceleration in German capital goods output balanced by some tentative accelerating in consumer goods output and choppy intermediate goods output. Construction output has been strong and accelerating despite its hefty setback in June.

In terms of quantitative measures of volatility over the past four and one half years, we see that IP is the most tranquil of these measures. Year-over-year output gains currently are at 2.5% and year-on-year IP gains have been relatively stable in recent months despite monthly volatility. Manufacturing components show a clear deceleration in German capital goods output balanced by some tentative accelerating in consumer goods output and choppy intermediate goods output. Construction output has been strong and accelerating despite its hefty setback in June.

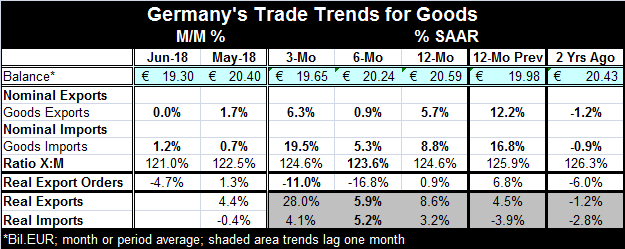

German exports and German foreign orders generally track reasonably closely, but they have diverged recently. Exports have seen their year-over-year growth pick up while foreign new orders have been cooling.

German exports and German foreign orders generally track reasonably closely, but they have diverged recently. Exports have seen their year-over-year growth pick up while foreign new orders have been cooling.

Monthly German trade data show exports have gone flat in June after a nice gain in May. Imports are surprisingly strongly in both May and June. Imports have accelerated over three months; three-month growth up to an annualized rate of 19.5%. On the same period, exports are up at only a 6.3% pace. Over 12 months, imports are rising at an 8.8% pace while exports are up at a more compact 5.7% pace. The massive German trade surplus is lower in June at 19.3 billion euros, compared to 20.4 billion euros in May and a 12-month monthly average of 20.6 billion euros. It's lower, but not by much.

German real trade flows lag one month. On that basis, it is exports that are accelerating and imports that have been muted with continued growth rates around 5% or less for 12-month, six-month and three-month. In contrast, export growth in real terms has exploded at a 28% annual rate on data up-to-date through May. German export data are unclear as to there being any trade war effects present in the data as of yet. Surging export volumes suggest that goods shipments may have been expedited ahead of pending tariffs. But we do not see a parallel shift for imports. Of course, import volumes/values are affected by energy where oil prices have been oscillating widely on global markets potentially obscuring any other effect in the data stream.

On balance, Germany seems to show signs of slowing growth. But this is after a period of acceleration. What is unclear as yet is whether the slowdown is going to overshoot or stabilize comfortably. While real manufacturing orders are dropping very rapidly, German output and exports are decelerating more moderately. The manufacturing PMI for Germany has rebounded in June. For the moment, it appears as if Germany is managing the slowdown transition just fine. Evidence of trade war impact is sketchy or nonexistent.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief