Global| Nov 07 2013

Global| Nov 07 2013German IP Drops but Expansion Lies Ahead

Summary

German orders are rising strongly despite a sharp drop in industrial output in September. As goes capital goods so goes German output. So it is not surprising that a 0.9% drop in output was caused mostly by a 2.1% drop in the output [...]

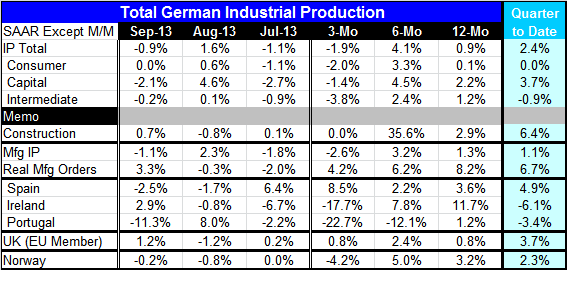

German orders are rising strongly despite a sharp drop in industrial output in September. As goes capital goods so goes German output. So it is not surprising that a 0.9% drop in output was caused mostly by a 2.1% drop in the output of capital goods. Over 12-months the 0.9% increase in industrial production is led by a 2.2% gain in the output of capital goods.

German orders are rising strongly despite a sharp drop in industrial output in September. As goes capital goods so goes German output. So it is not surprising that a 0.9% drop in output was caused mostly by a 2.1% drop in the output of capital goods. Over 12-months the 0.9% increase in industrial production is led by a 2.2% gain in the output of capital goods.

However, in September output was weak on a broad front. This weakness followed strong gains in August. But over three-months IP is falling.

Because of the pattern of the strength, IP is still rising strongly in Q3 compared to Q2. In September the quarter to date calculation is a full quarterly growth calculation. On that basis IP is up at a 2.4% annual rate in Q3 driven by a 3.7% gain in capital goods output. Construction output is surging in the quarter, rising at a 6.4% annual rate. Manufacturing output is only up at a 1.1% annual rate in the quarter. However, the reason to remain optimistic on German output is that orders are so strong. Real orders are rising at a torrid 6.7% real annual rate in the quarter. And orders bear a close correlation to German manufacturing IP.

The growth rate for contemporaneous German manufacturing IP and Real Orders year-over-year growth strikes a strong R-squared relationship of 0.82, marking a strong and positive correlation between real orders and real manufacturing output. But with the orders gain led by one-month the correlation on the year-over-year growth rates rises to 0.90. Then, if we lead orders by two months, the R-square rises to 0.94. On longer leads the correlation diminishes.

With these statistical results in hand, the one month set back to output is hardly disturbing given the strong guidance we are provided with for the future by German orders.

Other early-reporting EMU countries echo strength in Q2. Ireland and Portugal, among the EMU and non-EMU countries in the table, show falling IP in Q3. The UK leads the pack in IP growth in Q3, but that has been a clear developing theme for the UK recently. Its economy is looking more stable and UK auto production has continued to churn out steady gains.

Industrial output tends to be more volatile than GDP. What we see in the table are encouraging signs of IP growth in Q3. That is encouraging for GDP results as well. But the eurozone still has issues. The European Central Bank just cut its key lending rate from 1% to 0.5%, acknowledging the region's need for more help. Unfortunately 50bp lower in rates is no panacea. One of the main problems in EMU as in the US is the lack of credit growth. Such a small drop in rates will not increase demand much and may make lenders more wary to advance funds at such low rates believing that rates are going to have to rise from these levels, possibly adversely impacting borrowers. To counter such expectations both the Federal Reserve and the ECB are trying to use forward guidance. We have yet to see any evidence that it is working.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief