Global| May 07 2010

Global| May 07 2010German IP Continues To Run Up

Summary

In the midst of chaos in markets in the aftermath of the US stock market snafu on Thursday and ongoing turmoil over Greece in Europe despite the Greek bail-out being substantially approved by all parties, Europe’s growth is looking [...]

In the midst of chaos in markets in the aftermath of the US stock market snafu on Thursday and ongoing turmoil over Greece in Europe despite the Greek bail-out being substantially approved by all parties, Europe’s growth is looking better. German IP rose by a sharp 4% in March on the same day that the US was reporting nearly 300K in job gains for April. Ironically, in the midst of such upbeat growth reports markets are starting to get negative on global growth prospects over Greece.

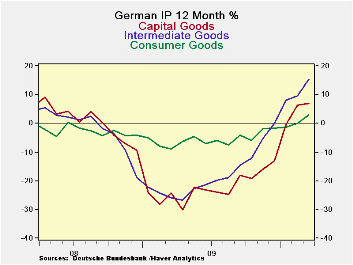

The German report on strong IP shows us building strength over three-months compared to six- months. Both MFG and construction are building momentum. Unfortunately the output of consumer goods continues to not just lag but to decline and the pace of decline for consumer goods output has accelerated. But for intermediate and capital goods, output is advancing and accelerating strongly. Germany has a two-tier economy. One tier seems to be strongly supported by capital goods spending and orders linked to strong international demand. The other tier is its consumer goods sector that is weak both in Germany and abroad leading the output in that sector to falter. Still the message overall is that IP is advancing and doing so with strength and good solid underpinnings.

Our main point here, is that growth both in Europe and in the US is looking better, not worse despite what markets are doing. As for analysts, in an effort to look ‘smart’ they are always looking for a way to explain the ‘decline du-jour.’ But the recent news has been good, not bad. In recent days we have seen patches approved to stopper those things that could have gotten out of control and hampered growth. I’m not sure we want to throw a party for the March German IP report and the April US employment report (and its revisions) but we do have on balance net good news over the past two days. And that is not what markets are trading to. In the end, that is a point to ponder. But it’s not a reason to throw out the good news and go rummaging in the trash bin of old news for an excuse to explain what appears to be an irrational act by the markets, and one that could easily be reversed in the coming weeks. Markets have seemingly irrational sharp sell offs from time to time. Accept it. Think about it. But don’t let it cripple you or lead you to shove a square peg through a round hole to get closure.

| Total German IP | |||||||

|---|---|---|---|---|---|---|---|

| Saar exept m/m | Mar-10 | Feb-10 | Jan-10 | 3-mo | 6-mo | 12-mo | Quarter- to-Date |

| IP total | 4.0% | -0.2% | 0.1% | 16.4% | 3.9% | 8.6% | 3.7% |

| Consumer | 1.7% | -2.3% | -0.3% | -3.5% | -0.2% | 2.9% | 1.2% |

| Capital | 4.4% | 1.2% | -1.7% | 16.4% | 1.3% | 6.9% | 3.9% |

| Intermed | 3.5% | -0.1% | 3.4% | 30.2% | 9.2% | 15.3% | 8.5% |

| Memo | |||||||

| Construction | 26.7% | 0.0% | -14.2% | 39.8% | 12.1% | 1.6% | -27.3% |

| MFG IP | 3.4% | 0.0% | 0.6% | 17.4% | 3.7% | 9.7% | 5.0% |

| MFG Orders | 5.0% | 0.0% | 0.1 | 49.1% | 18.7% | 26.0% | 28.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief