Global| Jul 12 2016

Global| Jul 12 2016German Inflation Edges Up As Euro Area Picture Gets Murky

Summary

Rising inflation in Germany with still-weak conditions in the rest of the euro area is a prescription for more intense euro area conflict. And that may be what is now in train. Germany in June posted its second monthly HICP hike in a [...]

Rising inflation in Germany with still-weak conditions in the rest of the euro area is a prescription for more intense euro area conflict. And that may be what is now in train. Germany in June posted its second monthly HICP hike in a row. After being flat on a year-over-year basis in May, the HICP is rising in June albeit by the skinny margin of 0.2%.

Rising inflation in Germany with still-weak conditions in the rest of the euro area is a prescription for more intense euro area conflict. And that may be what is now in train. Germany in June posted its second monthly HICP hike in a row. After being flat on a year-over-year basis in May, the HICP is rising in June albeit by the skinny margin of 0.2%.

Overall trends are rising

The chart shows that German inflation is accelerating based on time series plots of three-month, six-month and 12-month growth rates. Headline inflation has been gathering momentum. Still, on all these horizons inflation is still below EMU-wide target of just-under-2%. And these trends are for Germany alone, not for the whole EMU which is what the ECB targets.

German components show pressure is rising

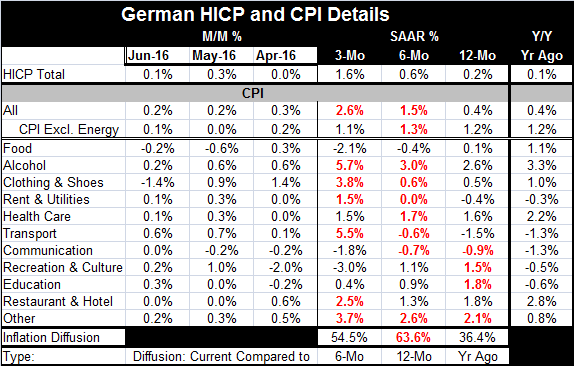

Looking at trends by components in Germany's domestic CPI, we find that among the 11 major inflation categories inflation has diffusion characteristics that are showing some pressure. These are ISM-like diffusion readings applied to inflation rates for each period. The three-month diffusion calculation compares all component inflation rates over three months to all of them over six months. The six-month diffusion metric comparisons are for six-month component trends by category to each over 12 months. The 12-month metric compares 12-month inflation component trends to 12-month inflation for components one year ago. On these comparisons, German inflation is accelerating over three months with a mild diffusion reading at 54.5, above the neutral reading of 50. Over six months diffusion shows broader inflation acceleration with a value of 63.6. But compared to one year ago, inflation is still not very broad-based with diffusion well below 50 at a very low diffusion reading of 36.4.

Some commonalities

Over three months and six months, the common areas of inflation pressures are alcohol, clothing and shoes, rent and utilities, transportation, and `other.'

HICP vs. German domestic CPI

The overall German CPI shows steady acceleration from 12-month to six- month to three-month as inflation intensifies from a 0.4% pace to a 1.5% pace to a 2.6% pace. The HICP trend shows steady pressure building as well but on lower gains with three-month inflation as the highest on the sequence but only with a rise at a 1.6% pace. The German inflation definition shows ex-energy inflation trends are for the most part moving sideways with inflation nearly nailed at a 1.2% not just on the 12-month, six-month and three-month sequence but also for 12-month inflation one year ago in June.

The German view

German officials have consistently referred to the EMU inflation environment as moderate rather than as weak or low.

The IMF on Italy

In this environment, the recent IMF comments on Italy are shocking. It has urged Italy to get on with fixing banks and has suggested that it deal with the EU bail-in provisions `appropriately.' This is a one-word dismissal of very thorny problem for Italy. German banks were fully bailed out of their exposure to Greece and elsewhere by the government because it was done before these new `Cyprus rules' were put in effect. Now Italy is caught on the `wrong side of tracks' under the new rules. These rules may be politically just too controversial to be followed. Apart from the banking sector problems per se, the IMF has project two decades of lost growth for Italy as it comes to grips with its various economic problems. The IMF sees Italy all-but stagnating while the rest of Europe grows. This is a politically charged outlook especially with Italy's Five-Star Movement gaining traction.

Britain getting a new PM - almost

Britain has a new PM `on tap', but the position is not official until the candidate meets with the Queen who is out of the country presently. But once that position is filled by current Home Secretary Theresa May, Britain will be in a position to move ahead on its extraction from the EU.

EMU outlook is SURPRISE rosy!

Today the joint forecast compiled by Italy's Istat, France's Insee and the Germany's Ifo think tank projected somewhat stronger growth in the EMU area for this year. The full year growth of 1.6% is faster -yes, faster- than its previous projection (made in April) of 1.4%. Despite all the `noise' about the impact of Brexit, this triad of euro-insiders does not see any disruption to GDP growth this year for the EMU.

It's official: China loses on South China Sea

China officially lost its case in the tribunal's decision on its South China Sea grab. It's a ruling China has warned everyone that it was preparing to ignore. Now the weight of word opinion is squarely against China.

OPEC and the oil outlook

OPEC launched a more optimistic forecast in which it sees demand rising and oil supplies in better balance in 2017.

More U.K. stimulus...still more talk than action

In the U.K., BOE Governor Mark Carney has again hinted at more stimulus.

Japan unveiled

In Japan, the government has drastically cut its inflation outlook tacitly admitting that things are much worse than they previously projected. Inflation simply is not moving away from zero, the way policy had previously said it would. This opens the door for more stimulus and the BOJ is expected to mount a new program. The government's new inflation projection for the current fiscal year has been cut to 0.4%, down from the 1.2% pace that had been projected in January.

Summing up the Apples and Oranges

Clearly there are a number of difficult trends in play ranging from economic to geopolitical. With oil prices firming, the worst of the deflation scare may be behind us, but prices still are not rising with nay gusto or anywhere near target in the EMU, Japan, or the U.S. Japan has a very long period (and it continues) of weak prices that has been in place long before oil became an issue. It would be unwise to think that all the price weakness issues will be solved by oil or even to assume that the OPEC outlook is the correct one. Russia continues to run down its various financial reserves because it just can't make its budget work at current oil price levels. In short, there are a lot of unsustainable things that are still sustaining. And the path for the U.S., the largest global economy, remains unclear although there is less of sense of concern over it in the wake of the recent U.S. job report for June. Still, the news out of Asia where China spreads its main influence continues to show weakness.

The global economy remains in a rough patch. But in Germany inflation may be returning to a more normal level and that could bring more policy conflict to Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.