Global| Jan 16 2020

Global| Jan 16 2020German Inflation Begins to Look More 'Normal'

Summary

Germany's inflation, in fact, is not back to normal or even in the normal range…yet. Even if it were, the ECB mandate is to run policy off of the EMU-wide inflation situation, not the German situation. Germany does have the lowest [...]

Germany's inflation, in fact, is not back to normal or even in the normal range…yet. Even if it were, the ECB mandate is to run policy off of the EMU-wide inflation situation, not the German situation. Germany does have the lowest unemployment rate in the EMU so if someplace is going to 'normalize' first, it would probably be Germany… probably.

Germany's inflation, in fact, is not back to normal or even in the normal range…yet. Even if it were, the ECB mandate is to run policy off of the EMU-wide inflation situation, not the German situation. Germany does have the lowest unemployment rate in the EMU so if someplace is going to 'normalize' first, it would probably be Germany… probably.

Undershooting is still the reality

Still, the facts show that German inflation continues to undershoot the old German goal of just less than 2%; it's the same inflation marker that applies to EMU-wide inflation. The chart shows that the undershooting and down-trending of year-on-year German consumer-level inflation is undergoing change; and although it is still undershooting, inflation is no longer decelerating. Six-month inflation has bounced higher and the three-month trend has a moderate uptrend in place. These are the circumstances that begin to make German trends look 'more normal' even if inflation is not yet back to normal.

The judgment of normalcy

It is also true that 'normal' looks different depending on where things have been. Since Germany has been chronically undershooting an inflation rate that is only beginning to snake back up into the normal range, it may not actually 'look normal' until the full inflation objective is realized.

Other inflation trends

Other inflation trends

And then there is the matter of inflation forces. The PPI-ex-energy shows that inflation forces more broadly conceived continue to trend lower without much hint of reversal. This calls to question whether the pressure in the HICP/CPI will remain in force. Inflation as a concept should refer to a broad price concept. And if a nation is truly experiencing inflation instead of just a shift in relative prices, all suitably broad gauges should reflect that trend. When that is not what is observed, it is possible that what is being experienced may not be lasting inflation but may be a more narrow sourced perturbance of some sort. And of course, globally, growth is still sluggish and global inflation is still undershooting in the EMU, Japan and the United States. Places that have some inflation issues generally are seeing pressure in food prices such as in India and China. China had cut off food imports from the U.S. as part of its trade war and then was hit by a terrible disease that required the elimination of its pigs, an important food source there.

More on German CPI trends

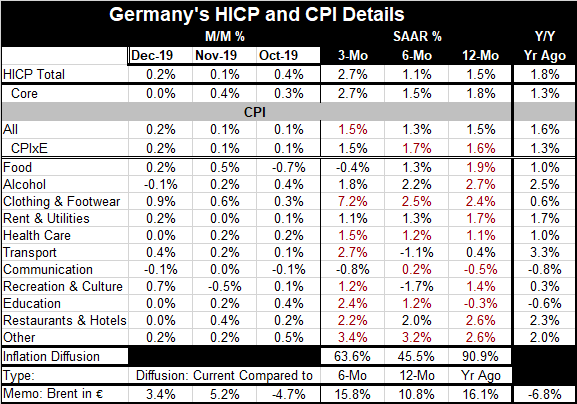

HICP trends show more of a burst in inflation than does the German CPI. Over three months, the HICP registers a 2.7% annualized pace of inflation for the core and headline measures, compared to a 1.5% pace for the CPIxE and headline in the German CPI. That's a big difference…Conversely, the CPI shows a bit more inflation in both the CPIxE and the headline over six months, compared to the HICP. Year-on-year, the HICP and German CPI measure the same modest 1.5% lift in the headline with the HICP core hotter at 1.8% and the CPIxE cooler at 1.6%.

Specific differences but fundamental agreement?

With different price definitions, calculating inflation over short-time periods will almost always give differences that are due to technical definitional factors rather than fundamental inflation forces. Another way to evaluate inflation is to do it item by item. In an aggregate price index, there will be myriad components and each will have somewhat different behavior. Each will get a weight. And that behavior discounted by its weight and summed up across all components of the price index becomes what the price index is and does. In the German table, I use the concept of diffusion to ask if all price components are behaving the same way over three months, six months and 12 months. Inflation diffusion is the result; it is presented in the table bottom, showing that inflation is broadly accelerating (accelerating over more than half the categories when the diffusion gauge is above 50%). The table shows diffusion at 63.6% over three months and at a whopping 90.9% over 12 months. Over six months, the 45.5% reading says that inflation is not accelerating on that horizon.

Diffusion and motivation

For diffusion, the shorter timelines are more prone to shifting; the year-on-year diffusion gauge is the most important. On that tenor, what we see is that inflation is accelerating in each category except for Transport (the calculation is based on full precision in the spreadsheet not just the one decimal rate presented in the table). Interestingly, in the year-ago period, Brent oil prices fell by 6.8% over that 12-month span while currently Brent prices are rising by 16.1% over 12 months. In the recent 12-month period the CPIxE pace is 1.6%, compared to 1.3% a year ago. So ex-energy inflation has stepped up quite apart from rising oil prices since the CPIxE excludes oil.

Slow and uneven up-creep

While the pick-up in inflation is indeed broad-based in the CPI, the CPIxE rate is up to just 1.6% over the past year compared to 1.3% one year ago. The up-creep in inflation is slow. Moreover, the CPIxE inflation rate is not accelerating over six months and three months rather it fluctuates and its rise is slower over three months than over 12 months. That suggest that what we are seeing is some trend pick up mixed with fluctuation.

Inflation...under my skin – or just the fear of it?

What all this means is that the various ways of getting at inflation, its trend and assessing to see its breadth to determine if a new trend is really locked into the bones of the data fails to provide an unambiguous determination. The PPI trend is opposite that of the HICP and CPI. And the PPI pertains to a different set of goods at a different stage of production. Still, the PPI message is so contrary and so clear and so long lived that it undermines any notion of 'inflation' being at immediate risk. This is especially true when the CPI itself behaves with some inconsistency. Still, there is some CPIxE acceleration and there is the calculation of breadth which produces an exceptionally high diffusion reading on year-over-year trends even if the effect on actual acceleration is small.

Inflation: the bottom line -Analytics vs. Extermination

The data seem to be suggesting that the inflation trend is stirring more than that it is fully awake or a full-blown danger. The muted effects and cross current in other data seem to suggest that a mild impact is in progress. If one has the hypersensitivity to inflation of most Germans, there could be more sensitivity to these findings. But inflation is still and has been undershooting; most others will find the proper alert status to be far below DEFCON one; it might not even reach the status of DEFCON five (the lowest status of U.S. defense condition readiness) for those applying nation defense ratings to inflation readiness and action plans. When inflation is below target, a little inflation simply IS your friend- at least it is if you take inflation targeting seriously. On this issue, we can question German motivations. Quite apart from the inflation mandate and language applicable to the ECB and policy goal, Germans and other 'inflation hawks' in the EMU seem to act as though any low inflation number is a good one regardless of how low it is. That is not inflation targeting and it is not what other members of the EMU signed up for.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief