Global| Jun 08 2020

Global| Jun 08 2020German Industrial Production Follows New Orders Lower; Records One-Month Drop in IP at -17.9%

Summary

The German industrial data are very consistent. All measures are showing extreme weakness in April. April data have been among the most consistently weak in Western economics. In April output in the capital goods sector is the weakest [...]

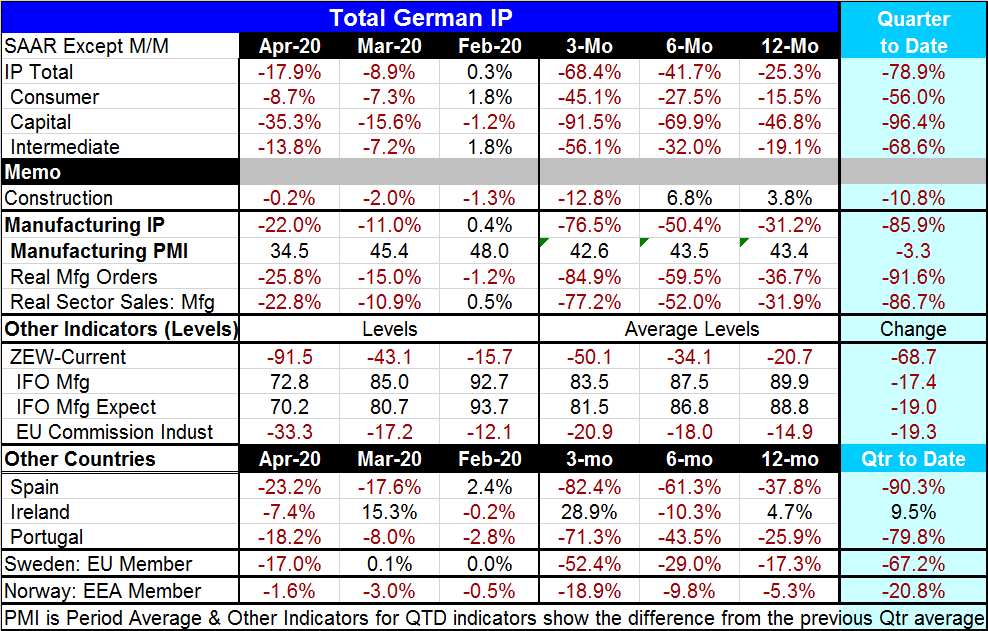

The German industrial data are very consistent. All measures are showing extreme weakness in April. April data have been among the most consistently weak in Western economics.

The German industrial data are very consistent. All measures are showing extreme weakness in April. April data have been among the most consistently weak in Western economics.

In April output in the capital goods sector is the weakest for Germany. In April intermediate goods is the second weakest sector with consumer goods being the least-weak sector (still quite weak however) in all in manufacturing. The construction sector has been much more modestly affected.

Manufacturing output alone fell by 22% month-to-month in April after a 11% decline in March. While capital goods lead the way lower in the quarter-to-date data with an annualized decline at a pace of -96.4%, all of manufacturing has output falling in the quarter at an 85.9% annualized rate. By comparison, construction is contracting in the quarter-to-date at a -10.8% annualized rate.

Industrial indicators also have fallen sharply as of April. The ZEW current index fell to a net reading of -91.5 from March’s -43.1. The IFO manufacturing gauge fell to 72.8 in April from 85.0 in March. The IFO expectations reading for manufacturing also fell to 70.2 in April from 80.7 in March. The EU Commission industrial reading fell to -33.3 in April from -17.2 in March. There is no disagreement among the various industrial indicators about what is going on.

Various European countries from different regions with different ‘economic systems’ show essentially the same pattern of behavior as the aggregate data. Spain shows a deeper decline for output in April than in March but shows extreme weakness in each of these two months. Ireland has output dropping at a 7.4% annual rate in April after rising in March. Despite that drop Ireland is the only country in the panel with IP up on balance over three months. Portugal’s drop in output is severe in April and couples with a drop in March as well. Sweden has an especially larger drop in output in April after a tiny increase in March. Norway shows a decline in output in April and shows a smaller decline than in March making it an exception to the weakening trend in April. Still, Norway’s output is weakening and falling faster from 12-months to six-months to three-months.

On a quarter-to-date basis, Ireland actually shows an increase in output in the making as of April, early in the new quarter. It also logs an increase on balance over 12 months and is the only country doing that.

By and large the weakness seems to be sweeping across Europe with a great deal of uniformity. Countries are having much the same experience with their economies as they fight off the effects of the coronavirus and this goes for Sweden, too, a country that did not lockdown the way other European countries did.

However, now across Europe the lockdowns are ending and there is a phase-in toward more normal economic activity and that will be restoring growth at some pace in the coming months. Everyone is wary and aware that the economic reopening also introduces a risk of a new spread in the virus so that is being watched closely.

A new wrinkle adversely affecting growth is the European adoption of the U.S.-sourced Black Lives Matter protests. There are demonstrations in many places including London. In Bristol, a statue of a slave trader has been torn down. In the U.S., of course, the disruptions and sometimes rioting has been worse. Over the past few days, the worst of the U.S. looting and rioting seems to have been quelled.

Still, everyone is looking forward to the end of the lockdown and the opening up of various economies that is now in progress. The reopening will be controlled and step wise. But since it is coming from such a weak base, the impact on economic data could still be quite large. And that could be true for a number of months running. However, economies will not be getting back to 100% anytime soon. But economies that get back to 90% of normal could still drive some impressively strong figures through yearend. Then the hard work would have to start. And we would have to hope that no second wave of infections has been set off by the growth process.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief