Global| Jul 08 2008

Global| Jul 08 2008German Industrial Output Now Points Clearly Lower – All Sectors Soften

Summary

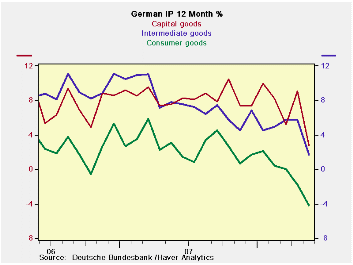

The weakness in German industrial output is spreading and cumulating. Consumer goods output is off by 4% Yr/Yr a strong drop for an inflation adjusted series. Capital goods and intermediates goods output are still up Yr/Yr but are [...]

The weakness in German industrial output is spreading and

cumulating. Consumer goods output is off by 4% Yr/Yr a strong drop for

an inflation adjusted series. Capital goods and intermediates goods

output are still up Yr/Yr but are slowing sharply. Over three months

each of these major sectors is undergoing a compounded negative growth

rate that is in double digits. Consumer goods and capital goods output

are lower over six months as well.

In the table see also reading on MFG output and orders. These

series also show double digit loses over three months (annualized).

Moreover in the quarter to date (April & May) taken

over the Q1 average, all major sector growth rates are negative. MFG is

down at an 8.3% pace and MFG orders are off at a leading 12.3% pace.

The German Zew and IFO indices have been showing weakness. The

EU Commission indices for Germany are weak as well and the EMU-wide

indices show gathering downward momentum for the Zone. The Markit (NTC)

indices are sharply lower for MFG and Services.

While a lot of Europeans are saying ‘no’ to recession it looks

as though circumstances are changing. And that should be no surprise

given the wimpy puny actions of the ECB as inflation has run rampant

over its target. EMU-wide headline inflation is over 4% and the ECB

ceiling for it is 2%. I’d be more forgiving in my assessments if the

ECB gave us some new policy direction. I am, for example not very

critical of the Fed with the nearly the same inflation metrics in the

US. The Fed ‘targets’ core inflation and this is actually still

behaving and is within its ‘comfort zone’ on some measures. But the ECB

is a stubborn headline inflation targeter and it is way behind the

curve yet it is hiking rates by only 25 bp and saying a series of rate

hikes does not lie head? How does one makes any senses of that?

Especially as Euro-finance ministers were screaming at the ECB for even

that rate hike and today they are saying that they never pressured the

ECB at all. No, this is not a script for a US day-time soap opera

entitled ‘As The World Churns’…

What can all this mean?

It either means that the ECB has lost its mind, or that the

ECB is convinced that the strong euro is helping to slow the economy

sharply, making a policy to crush inflation now unnecessary and unwise.

Yet the 25bp hike was needed to bolster its own credibility with

inflation so far out of line. But of course not even the one-mandate

ECB can say that. With Germany weakening given its standing the

strongest economy in EMU the ECB must find the news of weaker German

industrial output as ‘welcome.’ The strong euro is doing its job so

that the ECB does not have to do so much itself directly. That means

that the ECB may be able to forego any more rate hikes as the weak EMU

economy will now do the heavy lifting to abate inflation pressures.

| Total German IP | |||||||

|---|---|---|---|---|---|---|---|

| Saar except m/m | May-08 | Apr-08 | Mar-08 | 3-mo | 6-mo | 12-mo | Quarter to-Date |

| IP total | -2.4% | -0.2% | -1.0% | -13.5% | -1.7% | 0.8% | -8.8% |

| Consumer | -1.4% | -2.9% | 0.8% | -13.2% | -5.7% | -4.2% | -14.7% |

| Capital | -3.9% | 2.7% | -2.2% | -13.1% | -3.0% | 2.7% | -4.9% |

| Intermed | -1.8% | -1.9% | 1.0% | -10.2% | 1.0% | 1.7% | -7.9% |

| Memo | |||||||

| Construction | 1.1% | -3.5% | -13.1% | -48.2% | -0.7% | -1.6% | -42.4% |

| MFG IP | -2.6% | -0.3% | -0.3% | -12.2% | -1.9% | 0.9% | -8.3% |

| MFG Orders | -0.9% | -1.7% | -0.5% | -11.9% | -10.7% | 0.2% | -12.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief