Global| Nov 26 2018

Global| Nov 26 2018German IFO Shows Slippage in Conditions and Expectations

Summary

Both the German manufacturing IFO gauge and the Markit manufacturing gauge show fading trends in Germany. Still, the topical readings range from weak to very strong, depending on the nature of the response. Generally, current [...]

Both the German manufacturing IFO gauge and the Markit manufacturing gauge show fading trends in Germany. Still, the topical readings range from weak to very strong, depending on the nature of the response. Generally, current conditions metrics are firm to very strong while expectations range from strong (construction) to quite weak (manufacturing).

Both the German manufacturing IFO gauge and the Markit manufacturing gauge show fading trends in Germany. Still, the topical readings range from weak to very strong, depending on the nature of the response. Generally, current conditions metrics are firm to very strong while expectations range from strong (construction) to quite weak (manufacturing).

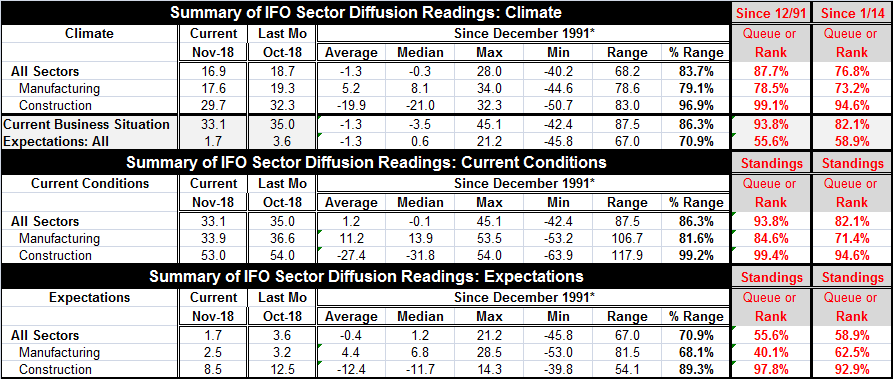

In November all the climate readings backtracked. The all-sector reading fell by 1.8 points, with manufacturing falling by 1.7 points and construction by 2.6 points. The current business situation slipped by nearly two points in November while expectations also were off by nearly two points.

Despite equal step backs for current conditions and expectations, the two readings are at very different places. On the long stretch of data since 1991, the current business situation ranks in the 93.8 percentile of its queue of data – an extremely strong reading. In contrast, expectations rank in their 55.6 percentile. Expectations are just a nudge or so above their median (of 0.6) which occurs at a ranking of 50%. In contrast, not only is the current business situation reading high-ranking, that fact is reinforced by its median being at -3.5, leagues of distance from its current 33.1 reading.

Quite obviously, the current readings are strong and solid and impressively firm. Separately, the manufacturing sector has an 84.6 percentile standing with construction at a 99.4 percentile standing.

Breaking form, expectations show construction still extremely solid and strong at a queue standing of 97.8 percentile compared to manufacturing where the standing is at its 40th percentile, well below its median (median is at 6.8 compared to the topical expectations reading of 2.5).

Both the IFO and the Markit indexes are telling the same story on the deflation of the manufacturing sector.

The ongoing weakness in global equites and ongoing drop in oil prices are not reasons to increase confidence in the economy. So far, no policymaker has referenced them.

Central banks increasingly are going to be in the spotlight. So far, no one has blinked. But growth is slowing and the Baltic dry goods index has been backing lower, pointing to weakening trade volume.

One growing problem internationally is that many governments seem to have less of a mandate for their mission. Theresa May has been struggling with accomplishing and defining her Brexit mandate without much support even now with a deal in the offing. The EU is dealing with rogue Italy and Brexit opportunism from Spain and France. Taiwan’s government has just lost support. In the U.S., Democrats have seized the House and the political environment is far from harmonious. Geopolitical tensions still simmer with Saudi relations pressured everywhere in the wake of the Khashoggi killing and increasingly over the unpopular war in Yemen. China is still assertive over its South China Sea hold. Russian has just aggressively seized several Ukraine vessels in the Black Sea. Of course, U.S.-Iranian relations are in a poor state.

These events provide a background of instability to an economic environment that had been gradually repairing itself after a long deep recessionary episode but has itself become less vibrant and has begun to show some weakness. The risks in this system are mounting and becoming more complex and because trade tensions seem to be the centerpiece of instability the weakness has drawn in and undermined all players. There is no indelible source of strength anymore. The outlook is up for grabs. No one has gotten extremely pessimistic, but the potential for bad events to engage and take control is now a palpable risk.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief