Global| Jul 25 2019

Global| Jul 25 2019German IFO Gauge Sinks

Summary

The IFO climate gauge has fallen to its weakest reading since July 2013. On the two ranking columns in the table, we see it has the lowest reading since January 2015, but it has a much less weak if still equivocal reading with a near- [...]

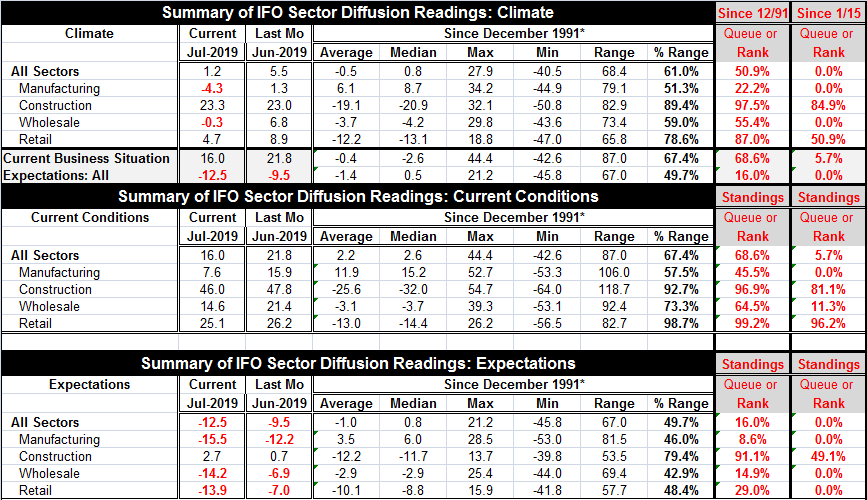

The IFO climate gauge has fallen to its weakest reading since July 2013. On the two ranking columns in the table, we see it has the lowest reading since January 2015, but it has a much less weak if still equivocal reading with a near-median 50.9 percentile standing on data back to 1991. Measured on a short leash, the IFO is very weak. Given more perspective, we find that economic conditions are not so drastically weak, but we do find them to be only at middling values and with slipping and weak expectations on any timeline and that pushes us back to fears of weakness. Whatever the levels of the variables, it is impossible to look at the chart and to come away unconcerned.

The IFO climate gauge has fallen to its weakest reading since July 2013. On the two ranking columns in the table, we see it has the lowest reading since January 2015, but it has a much less weak if still equivocal reading with a near-median 50.9 percentile standing on data back to 1991. Measured on a short leash, the IFO is very weak. Given more perspective, we find that economic conditions are not so drastically weak, but we do find them to be only at middling values and with slipping and weak expectations on any timeline and that pushes us back to fears of weakness. Whatever the levels of the variables, it is impossible to look at the chart and to come away unconcerned.

Trappings of weakness and oddities

The IMF has been cutting its outlook for global growth and the recent Markit manufacturing gauge for Germany continues to pound its way to weaker readings. Bloomberg News reports a new record high of $13.trillion in negative yielding debt. Excluding Japan from the data since its inflation rate is so low, Germany has 24% of that debt in a rest-of-world index. Germany is the epicenter of blooming crisis with depressed growth and negative interest rates at the core as it reverberates to global trade shocks.

Strange bedfellows

This is still a bit of Bizarro Land (if you can excuse the reference to some old Superman comic books (reference here). The reference is to a world in which things are essentially upside down and Superman is a bad guy. The application is this: while interest rates are below zero in Europe and a lot of debt instruments CHARGE interest instead of PAY interest, economic growth remains by and large still quite acceptable. Just today Spain reported that its structurally high rate of unemployment fell to 14% from 14.7%. While I will not try to convince you that a double-digit unemployment rate is great news, it would be the lowest rate for Spain since about 2008. So take what good news there is where you find it.

IFO meets Markit and IFO meets IFO

Expectations now are starting to flash the kind of warning signs that are more in sync with the state of monetary policy. Yet, current economic conditions are even keeling; true, they compare badly to what has been in place since early-2015, but the performance relative to a longer history is adequate. The chart shows manufacturing IFO and Markit manufacturing readings tracking quite well for the period since January 2015 when my Markit data begin. So there is no disconnect between the Markit signal and the IFO signal- manufacturing is weak. The Markit diffusion reading for German manufacturing is now quite low in absolute terms, below 45. It's weak. And the IFO time series inconsistencies in ranking various sectors are exposed by looking at the two periods and their differences then realizing that those differences are moot because there are consistent weak readings for expectations under both regimes. Whatever the current reading, there are expectations of weakness.

IFO by sector - construction

The IFO details show an even stronger construction sector in July and in June and sector strength for climate, current conditions and even expectations with the exception that the short period the standing for this vibrant sector is only near a neutral position at a 49th percentile standing.

Retailing, manufacturing and wholesaling

The retail standing is strong for current conditions on both timelines, strong to neutral for climate and weak on both timelines for expectations. After retailing there is no strength on any timeline. Manufacturing and wholesaling are weak to moderate on climate and current readings and both are exceptionally weak on the short timeline- but more disturbing is that they have lower 20th percentile or weaker standings on the longer timeline for expectations.

Current business situation and expectations

The overarching current business situation reading at 16 weakened in July from 21.8 in June, a sharp fall. The month's drop is outsized but not chilling; drops this large or larger happen one third of the time historically still that is not to diminish it. The current business situation has a 68.6 percentile ranking on the long horizon back to 1991. But expectations in July fell to a reading of -12.5 from -9.5 and have a 16th percentile reading on the long timeline; they have not been lower since January 2015.

The German situation

These statistics map out the present situation for Germany. Its services sector is going better, but its growth expectation is being cut back. With Boris Johnson in as Prime Minister in the U.K., German trade with the U.K. could be at risk to a hard Brexit which seems where this is headed. The EU has said the negotiations are over. Johnsons has said that Irish backstop is unacceptable even with a hard Brexit, but he has no power to change it. I guess Johnson finding himself between a rock and a hard place has chosen bluster. In this case, a hard Brexit will have also unfortunate consequences for Germany for which the U.K. is a significant export market. The U.K. imported about 75 billion pounds from Germany in 2016. And there is still a global slowdown and an ongoing U.S.-China trade showdown in progress. Germany is still at risk.

Who's zooming who?

The IFO survey echoes the concerns we saw expressed in the earlier ZEW survey as well as in the Markit PMIs. Only the U.S., where growth also has slowed, has sparked come recent counter indication of revival with a rebound in the Philadelphia regional manufacturing survey for July and an order rebound nationally in June for durable goods. It is still exceptionally difficult to tell what is going on or what the next trend is going to be both in the U.S. as well as globally. Last months' U.S. labor market snapped back and this week jobless claims continue to hug very low readings. But Asia and Europe show signs of ongoing and deepening weakness. The U.S. also shows signs of trade-induced weakness with declines in goods exports and flat goods imports over 12 months. But the U.S. remains much more of a domestic-oriented economy and a source for global demand rather than at risk to global demand.

Who is at risk to global demand?

When global demand outside the U.S. fades, the U.S. is not hurt by it as much. As I suggested at the outset of the U.S.-China trade war, China would be hurt more by it. Consumers can switch to buy other products or substitute vacations for consumer durable purchases or wait if import prices are too elevated by tariffs. But a producer facing slower sales lays workers off. When ‘workers' don't have income, they stop purchasing. The economic effect can be strong and immediate.

China and Germany, two peas in a pod?

China is using debt as a substitute to prop growth up but that is temporary, less effective and dangerous. Despite the way that the economics profession has portrayed this trade war and its tariffs, the U.S. is in the catbird's seat in the short term, at least. As we see with Germany, usually Europe's strongest economy, since Germany depends on trade and since trade is pulling back, Germany is feeling the pull back more than countries that typically have relied on their own domestic demand.

Risks remain

Global growth is being hemmed in; the risk of backsliding is acute. This is why central banks are acting or planning action because the risk they see is palpable. The ECB put us on notice just yesterday to easier policies. The Fed is expected to cut rates later this month. This will not be a classical central bank easing cycle, but it may be as important as any that came before.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief