Global| Nov 24 2014

Global| Nov 24 2014German Ifo Gauge Bounces Back

Summary

The Ifo gauge in November surprisingly rose, posting a 2.3 value after logging a -0.6 value in October. All sectors showed improvement in November compared to October with two of them still logging net negative values. The current [...]

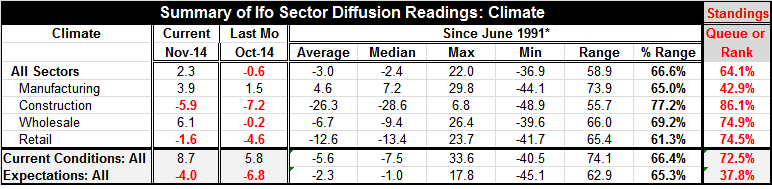

The Ifo gauge in November surprisingly rose, posting a 2.3 value after logging a -0.6 value in October. All sectors showed improvement in November compared to October with two of them still logging net negative values. The current condition index rose smartly month-to-month to 8.7 in November from 5.8 in October while expectations continued to be negative at -4, but rose from -6.8 in October.

The Ifo gauge in November surprisingly rose, posting a 2.3 value after logging a -0.6 value in October. All sectors showed improvement in November compared to October with two of them still logging net negative values. The current condition index rose smartly month-to-month to 8.7 in November from 5.8 in October while expectations continued to be negative at -4, but rose from -6.8 in October.

Before we get too excited by this reversal, be sure to look at the chart and notice how small the rebounds are compared the slippage that we've seen in 2014.

One month is not enough to reverse momentum. Indeed the issues facing the euro area continued to be approximately what they had been in recent months. But with China cutting rates, with Japan doubling up on its quantitative easing program, and with Mario Draghi sounding like he's ready to throw down the gauntlet on quantitative easing, markets are getting more optimistic and we saw that in the ZEW report issued previously and in the responses to today's Ifo report.

Optimism, however, is not enough. In a survey released today by Markit, global optimism has turned out to be at its weakest point in the last five years. Geopolitical developments continued to be touch-and-go, with the result of an OPEC summit uncertain and with Iran at a stalemate with the West as its deadline for deal on its nuclear capabilities runs to a close. And of course the Middle East is still under attack from Islamic extremists.

In this environment, the all sector index in the Ifo survey stands only in its 64th percentile. It is short of the top third of its historic range of values. The manufacturing sector sits in the 42nd percentile of its historic queue of values; thus, marking it as weaker only 42% of the time and stronger 58% of the time. The construction sector, with the weakest absolute reading in November, has a queue standing of 86.1. The construction sector has been so weak during this period that a -5.9 reading leaves it in the top 14% of its historic queue! Wholesaling stands in the 74th percentile of its historic queue, just outside the top 25%. And retailing stands, similarly, in the 74th percentile, just short of its top 25%. Both wholesaling and retailing took sharp upward movements in November from October.

Turning to the current and expectations readings, we find that the current conditions index is still relatively firm in its 72nd percentile, higher only 28% of the time. Expectations, however, sit in the 37th percentile and are higher 63% of the time. Expectations are sitting just a slight distance above the lower third of their historic range.

As we ponder these developments, what we see in Germany is a current situation that is still relatively good in the face of expectations that have been cut back sharply this year. Economic conditions throughout the euro area are still difficult, but there's increasing optimism or hope that Mario Draghi will be able to take monetary stimulus to a new level, despite objections from Germany and a select few other EMU members.

There has been no breakthrough on a growth side involving individual European Monetary Union countries. There is no shift involving the use of fiscal policy or even on the monetary front. On the monetary front, there are hopes and there are expectations that things will change. The big change in Europe has been the continuing weakness in the euro exchange rate.

And while people in the market will say they understand it, to an economist it's one of the most curious things you could imagine. The euro area has the largest current account surplus relative to GDP of any major economic unit in the world. Yet its currency is falling, and this action will cause its current account surplus -already huge- to get even bigger. Meanwhile, the United States, which continues to run a huge current account deficit, has its currency running higher. This will make its deficit larger (all other things equal). When these processers are studied in academic circles, exchange rates are supposed to make the opposite movements from what they are making here in the real world. Exchange rate changes are supposed to restore equilibrium in the current account imbalance- not make the imbalance worse. But of course, at the moment, currencies are being driven by growth differentials, not by current account imbalances. The EMU's huge current account surplus stems as much from its level of competitiveness as it does from its depressed economic circumstance which leads to weak imports.

In short, the world's economies are in such sad shape that economic processes are in gear to make international imbalances even worse, and this can't be reassuring. Global imbalances were behind the financial crises we are just emerging from (trying to emerge from). The rising Germany's Ifo index today is slightly reassuring. However, we have to wonder how much of it is related to real-world events and how much of it is speculation about something the European Central Bank may not be able to do. And furthermore, how much of it is being made in the back of a declining euro exchange rate, a decline that is continuing to exacerbate international imbalances?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief