Global| Dec 18 2019

Global| Dec 18 2019German IFO Assessment and Expectation Improve

Summary

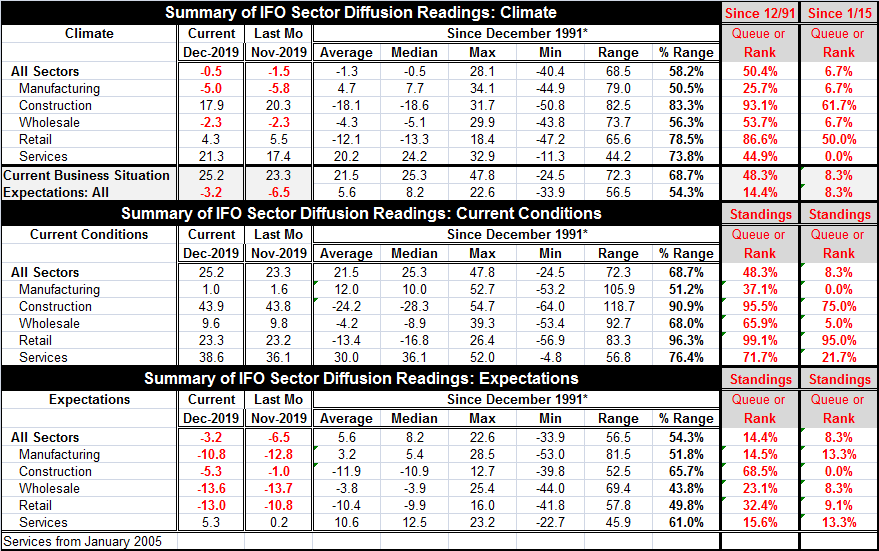

The IFO climate gauge improved to -0.5 in December from -1.5 in November. This improvement pushed the percentile standing to its 50.4 percentile in December from the 47.1 percentile previously, in November. Still, the ranking over the [...]

The IFO climate gauge improved to -0.5 in December from -1.5 in November. This improvement pushed the percentile standing to its 50.4 percentile in December from the 47.1 percentile previously, in November.

The IFO climate gauge improved to -0.5 in December from -1.5 in November. This improvement pushed the percentile standing to its 50.4 percentile in December from the 47.1 percentile previously, in November.

Still, the ranking over the shorter period from January 2015 is in its lower 7th percentile. Construction and retail have standings above their respective median (50%) marks over the longer period- they are pushing the all sector index higher (although retailing did slip this month). Manufacturing and services (both of which improved this month) are longer term weakening forces on the all sector climate index. Wholesaling right now ranks close to the all sector standing.

Both the current business standing and the expectations readings improved month-to-month in December. The current business situation is close to its longer term median ranking at its 48.3 percentile. The expectations index is still lagging its median badly with a 14.4 percentile standing. And expectations have a very low standing despite a substantial month-to-month improvement of over three diffusion points.

Current conditions improved month-to-month with the diffusion reading up to 25.2 in December from 23.3 in November. The improvement in the current index was driven almost wholly by the service sector improvement. Manufacturing and wholesaling were slightly weaker. On the other hand, construction and retailing made the smallest month-to-month improvements possible. On the whole, the improvement in climate, while technically benefiting from the higher current index, is mostly a creature of improved expectations.

Expectations in December improved in four of five sectors with a sizable worsening in retailing being the exception. Manufacturing made a substantial monthly improvement, wholesaling made a technical improvement, construction gained sharply and services have improved month-to-month by over five diffusion points. Expectations overall improved by a bit more than 3 diffusion points.

The IFO does show a bottoming in downward momentum. The expectations series shows the beginning of a rebound but it is still slight.

The German boom phase has unwound. What is not yet clear is that the deceleration phase as truly ended and it is not yet established if there is an improvement of any substance ahead. The data hint at such a development, but hints are not bankable. For expectations, all the December sector readings are negative except services. Only retailing and construction have long-term averages that are negative for expectations. Moreover, expectations’ rank standings are weak on both long- and short-term comparisons (far right hand columns in the table). The sole exception in that over the long haul the construction reading still rates as ‘firm’ even though it is at a low over the period since January 2015. Apart from that, all sector expectations are unambiguously weak.

The ZEW survey has been more upbeat at least on its macroeconomic expectations. For the IFO, there are expectation improvements in gear for the past three months, but they are still relatively modest and, as is the case even for the ZEW survey, expectations remain very low-ranking. This month’s IFO allows Germany to end the year on a brighter note and one with hope, but there is not a strong case for improvement to be made in this survey yet nor in actual global events or conditions.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief