Global| Mar 13 2020

Global| Mar 13 2020German HICP Accelerates As the Virus Tears Through the Global Economy

Summary

The German HICP pace rose to 1.8% year-over-year from a 1.6% pace last month. The acceleration happened because one year ago in February the HICP was flat compared to rising by 0.2% this month. The core pace is lower at 1.5% year over [...]

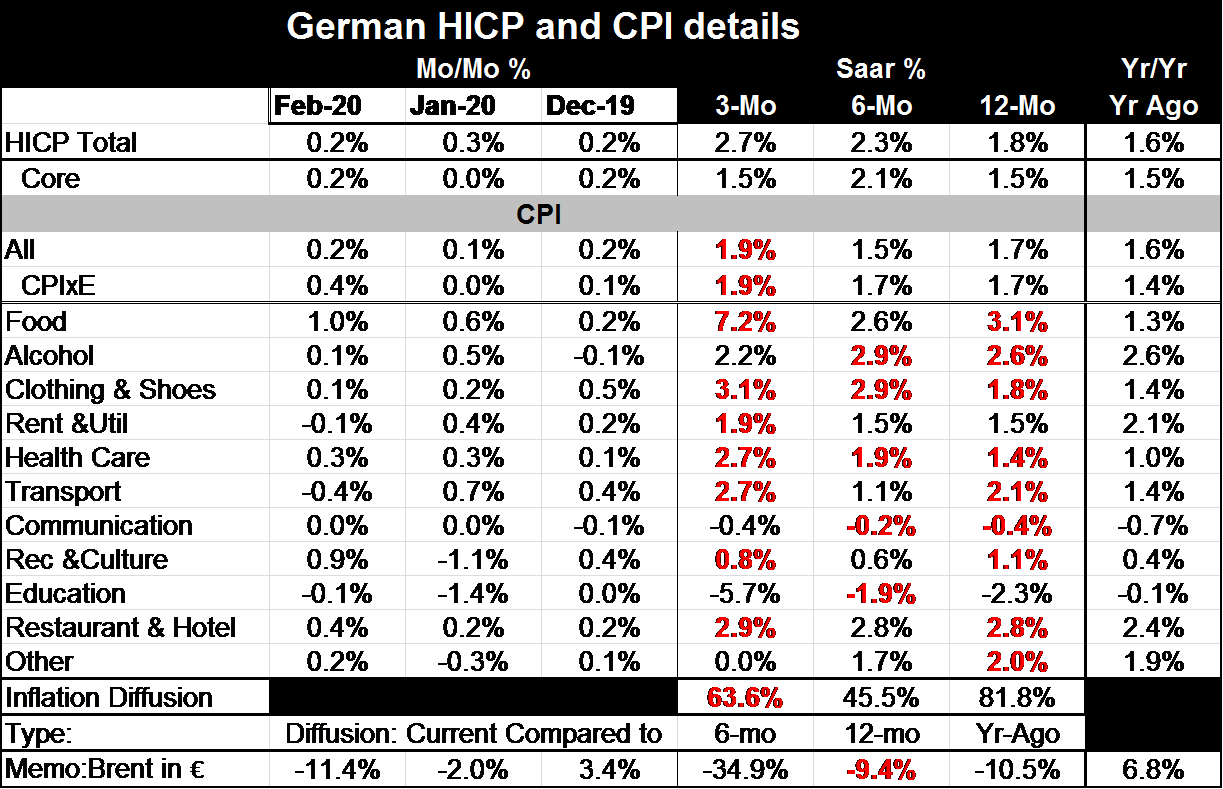

The German HICP pace rose to 1.8% year-over-year from a 1.6% pace last month. The acceleration happened because one year ago in February the HICP was flat compared to rising by 0.2% this month. The core pace is lower at 1.5% year over year pace. Both German metrics are well within the `just less than 2% bounds' for overall EMU inflation.

The German HICP pace rose to 1.8% year-over-year from a 1.6% pace last month. The acceleration happened because one year ago in February the HICP was flat compared to rising by 0.2% this month. The core pace is lower at 1.5% year over year pace. Both German metrics are well within the `just less than 2% bounds' for overall EMU inflation.

German inflation accelerates

German inflation generally is accelerating. The 3-month pace exceeds the 6-month pace and the 6- month pace exceeds the 12-month pace the 12-month pace is even higher that it was one year ago.

The acceleration is broad based

Inflation acceleration is confirmed by diffusion data. These data show that 63% of the major German price categories saw their price changes accelerate over 3-months compared to 6-months. Only 45% saw acceleration over 6-months compared to 12-months. But 81.8% saw acceleration of their 12-month change compared to the 12-month change of one year ago. Inflation only fails to show broad acceleration over 6-months and even then the diffusion rate is only 45.5% close to the 50% balanced marker.

Oil prices are chronically weak

Interestingly over these time segments oil prices generally have been falling. But more interesting is that right now oil prices are plunging.

German core rate shows modest pressure

Core inflation for the German CPI shows inflation at 1.7% over 12-months up from a 1.4% gain over 12-months one year ago. The pace over 6-months is also at 1.7%. Over three-months the core measure rises at a 1.9% pace, which essentially is the ECB targeted pace for the Euro-Area overall.

German inflation normalizes

Inflation in Germany shows signs of normalizing at the desired pace with unemployment at its lowest mark since German re-unification. Still all is not well in Germany and of course Germany is also in the grip of the coronavirus. But corona has many more implications for growth than for inflation. But if corona weakens the economy, it likely will weaken the inflation trend as well.

Outlier or harbinger

Corona is coming and spreading in Germany as well as over the rest of Europe, Angela Merkel has dropped her support of the zero new debt policy. Clearly Germany is going to face a weakening force like the rest of Europe and it will have to find some way to combat that. Individual countries in the EMU do not have monetary policy to use since the ECB provides an umbrella policy for the whole area. Individual countries will have to use fiscal policy to make any country-level impact. Italy, of course, has the most advanced set of problems. We can't be sure if Italy is a harbinger or an outlier for other European countries.

Italy Vs S Korea

A comparison of Italy to South Korea shows two countries that reported outbreaks at the same time. But Italy's have progressed faster and Italy has more deaths and infections. By comparison South Korea has had more success and that is being attributed to S Korea having depended more on testing, aggressive testing (More). Testing, knowing and responding to real information has been a better approach than blanket isolation or shutting down segments of the economy. Of course China, a country that has a totalitarian regime, used quarantine and containment enforced by Big-Brother tactics to quell the outbreak in Hubei rather quickly. Draconian can work. But then it is draconian.

What to expect (very little guidance...)

As we look ahead we must admit that there are very different national experiences so far. Testing seems very important. But a shortage of test kits and other needed medical equipment is slowing the application of science-based solutions everywhere. The internet is still spewing lies and half-truths. Don't go there for any serious information unless you go to a CDC or other nationally endorsed sites. Forget social (anti-social) media. There is a lot of dis-information. And no policymaker anywhere has yet to stand up to say that this virus is going to slow growth and it might even contract GDP but that this is the way we will slow its spread. We will return to growth when the crisis is passed so it makes sense for everyone to fight it together now to truncate its spread and reduce its eventual impact on the economy. Instead, policymakers speak as though they are going to do things to support growth. Polices are needed to support businesses and people harmed by the virus not policies to try to offset the virus impact and keep growth "strong". That is not possible. So I am still waiting to hear some leader, any leader, say something that makes sense to me.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief