Global| Jul 05 2019

Global| Jul 05 2019German Factory Orders Shrink-- The Message Is Clear

Summary

Germany's factory orders fell by more-than-expected in May. Total orders decreased 2.2% month-on-month in May, in contrast to a 0.4% rise in April. Domestic orders advanced by 0.7%, while foreign orders fell by a large 4.3%. Orders [...]

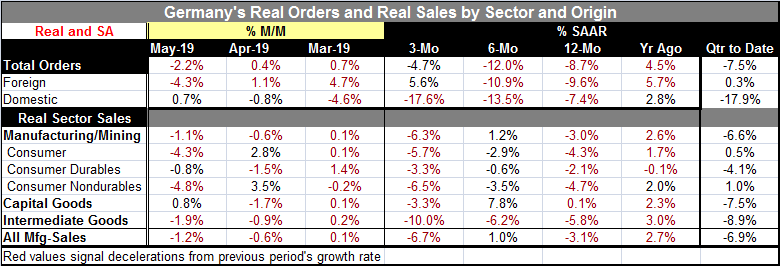

Germany's factory orders fell by more-than-expected in May. Total orders decreased 2.2% month-on-month in May, in contrast to a 0.4% rise in April. Domestic orders advanced by 0.7%, while foreign orders fell by a large 4.3%. Orders from the euro area skidded, dropping by 1.7% as orders from the non-euro area countries decreased by a much larger 5.7%.

Germany's factory orders fell by more-than-expected in May. Total orders decreased 2.2% month-on-month in May, in contrast to a 0.4% rise in April. Domestic orders advanced by 0.7%, while foreign orders fell by a large 4.3%. Orders from the euro area skidded, dropping by 1.7% as orders from the non-euro area countries decreased by a much larger 5.7%.

Order weakness in perspective

Year-on-year factory orders plunged 8.7%, bigger than any 12-month drop since a string of drops during the Great Recession from September 2008 through September 2009. Certainly, that comparison will attract attention. In this cycle, there are still other recent year-over-year drops of size as March saw orders drop over 12 months by 6%; in February orders dropped by 8% year-on-year. Orders are lower year-over-year for 10 months in a row. Foreign orders are lower over 12 months for nine months in a row. Domestic orders show 10 drops in a row for year-on-year changes. Foreign orders have fallen by 8.1% over this 9-month stretch of declines. Domestic orders have fallen by 7% over their 10-month string of declines. These declines are measured in real terms and reflect substantial cutbacks. While these are substantial declines in orders, they pale in comparison with recession declines; in the Great Recession, German orders fell intensely year-over-year for about six months in a row, posting declines of 30% or more in each month with lesser declines in adjoining months.

Out of area orders do worst

Fortunately, orders from within the euro area are dropping at a slower pace than from other areas. While there is widespread weakness in the euro area, the weakness in German orders from fellow EMU members suggests that the euro area downswing so far is being limited. We have seen EMU PMI gauges in manufacturing showing that overall manufacturing conditions are deteriorating but the PMI gauges are still sinking only modestly below their break-even values of 50.

Cross currents for orders

Trends for orders are somewhat confusing. Foreign orders show declines at about a 10% annualized rate for 12 months and six months but show growth over 5% (annualized) over three months (although the sharp decline in foreign orders in May hardly makes it look like they are out of the woods). Domestic orders are contacting steadily and at progressively faster rates of decline. The 12-month pace of decline is at -7.4% and the 3-month pace of decline is at a -17.6% rate.

Sector sales patterns

Sector sales (also expressed in real terms) show a somewhat erratic trend that ends with a downturn over three months. Manufacturing sales fell by 3.1% over 12 months then advanced at a 1% pace over six months before falling at a 6.7% annualized pace over three months. That pattern is largely thrust on the sector by capital goods where sales tick higher by 0.1% over 12 months then surge to a 7.8% pace over six months but pull back over three months as sales fall at a 3.3% annualized rate. Consumer goods output falls on all horizons, but the drop slows down a bit over six months compared to 12 months taking it away from a process of steady deceleration. Still, consumer goods are clearly weak and orders are dropping. Capital goods show some life, but that has faded, and intermediate goods sales simply plow lower, weakening sequentially on all horizons. All of that contributes to a trend that is poor.

Orders and sales: reinforced by recent IP trends

The weak orders and sales reinforce the weak PMI signals that now extend into June. Industrial production reports are dribbling in and they show a May decline in Spanish IP, Portuguese IP and Swedish IP against a small increase in Norwegian IP and another strong rise in output in Ireland. However, sequential 12-month to 6-month to 3-month growth rates for IP show expansion in Spain, Ireland and Norway. Portugal logs a 12-month drop then sales accelerate despite the May drop. Sweden actually has a modest 12-month and 6-month gain before output drops sharply over three months. Despite weakness this month, the scattered European results are mostly firm.

European trends more broadly

European trends for IP show little strength and tend much more to struggle. That message is reinforced by the manufacturing PMIs. EMU-wide retail sales are down by modest amounts for two months running. The U.K. shows a series of weakening measures, ranging from dropping productivity to reduced recruitment in the labor market to falling home prices and to a fourth monthly drop in auto production. In Asia, Japan posts a 6.5-year low in its leading economic indicators, but household income still managed to jump. The oil market still cannot get out of its own way; it is so concerned about the outlook that even with plan to cut output oil prices remain weak. Trends in Europe and globally continue to show weakness punctuated with only an occasional contrary bright spot or two. The steady drum beat to weak growth remains in gear.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief