Global| Aug 04 2005

Global| Aug 04 2005German Factory Orders Advance 2.4% in June: Good Rebound After Sluggish Winter

Summary

Manufacturers' new orders in Germany increased 2.4% in June, following a similar 2.3% gain in May. Forecasters had expected that after the good May rise, orders would be flat in June, so this was a pleasant surprise. This month, it [...]

Manufacturers' new orders in Germany increased 2.4% in June, following a similar 2.3% gain in May. Forecasters had expected that after the good May rise, orders would be flat in June, so this was a pleasant surprise. This month, it was orders from domestic German customers that gave the push, while in May, foreign customers' orders had the lead. As seen in the table below, foreign orders have been particularly strong over the past year, although domestic orders have shown moderate growth as well.

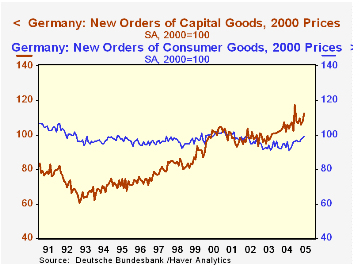

Further encouragement to the German outlook came from the fact that capital goods orders had the greatest strength. These rose 4.2% in the month and stand 12.9% above a year ago. Among individual industries, the year-on-year pattern highlights this strength in electrical equipment and transport equipment. Consumer orders are also rising, but less vigorously.

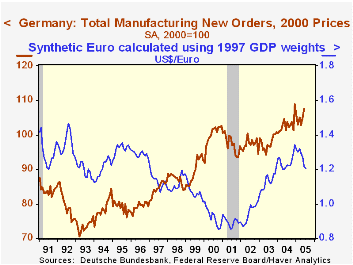

Press commentary today highlighted the decline in the euro so far this year as a factor supporting both domestic and foreign orders in the German factory sector. But the second graph doesn't seem to bear this out. Foreign orders turned higher before the currency value began to fall. Possibly the uptrend would have faded without the boost from a cheaper euro, but the currency value was not the initial force in the upturn. Rather, we would surmise that for both domestic and foreign orders the recent increases have come as the post-Y2K recession ran its course. Perhaps this performance will work its way into the consumer sector and help to improve the sluggish retail trade trends we discussed here yesterday.

| Germany % Changes, Months seas adjusted |

June 2005 | May 2005 | Apr 2005 | Year/ Year | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|

| Total | 2.4 | 2.3 | -2.2 | 9.0 | 6.4 | 0.6 | -0.3 |

| Domestic | 4.0 | 0.6 | -0.5 | 6.8 | 4.3 | -0.1 | -3.4 |

| Foreign | 0.8 | 4.9 | -4.6 | 11.1 | 8.9 | 1.5 | 3.5 |

| Capital Goods | 4.2 | 1.9 | -3.2 | 12.9 | 7.7 | 1.2 | -0.9 |

| Consumer Goods | 0.8 | 1.2 | 1.4 | 9.0 | 1.2 | -3.6 | -3.0 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief