Global| Sep 09 2016

Global| Sep 09 2016German Export Drop Sets Markets' Teeth on Edge

Summary

There is nothing quite like the day of reckoning. You can skate along with all sorts of beliefs and ideas then one day out of the blue something happens that turns that world upside-down and exposes a whole new heretofore unthought-of [...]

There is nothing quite like the day of reckoning. You can skate along with all sorts of beliefs and ideas then one day out of the blue something happens that turns that world upside-down and exposes a whole new heretofore unthought-of reality. And despite some sporadically weak economic numbers the German export performance seems to have been the catalyst for a re-think today. Welcome to re-think Friday.

There is nothing quite like the day of reckoning. You can skate along with all sorts of beliefs and ideas then one day out of the blue something happens that turns that world upside-down and exposes a whole new heretofore unthought-of reality. And despite some sporadically weak economic numbers the German export performance seems to have been the catalyst for a re-think today. Welcome to re-think Friday.

German trends

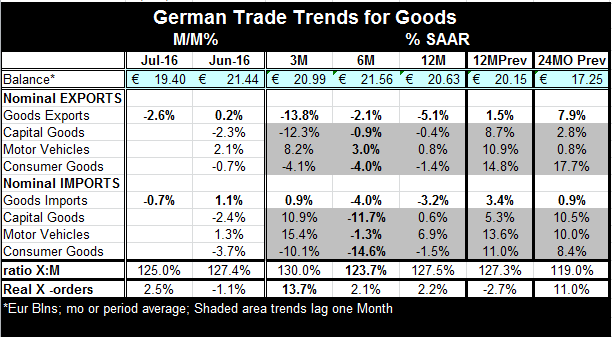

German exports fell by 2.6% in July. They are falling at a 13.8% pace over three-months and falling at a 2.1% pace of six months. Over 12-months they are lower by 5.1%. On these same time lines (see table) German imports also are weak but they have actually gained some pace.

One interesting contrary note is that German real export orders, a series that usually leads German exports, actually is showing life. Real German export orders are up by 2.2% over 12-months, at a 2.1% pace over 6-months and at a rousing 13.7% pace over three-months. Yet markets are not interested in this.

German exports to everywhere are falling

German exports to everywhere are falling year-over-year. German exports to EMU Area countries fell by 6% year-on-year. German exports to EU countries not in the EMU arrangement fell by 4.8%. German exports to countries outside the EU fell 13.8%. While there is clear weakness within Europe in both EMU and EU areas, the greater weakness in German exports was to counties outside the EU/EMU arrangement. The IMF was been warning and cutting its outlook. The OECD leading indicators released yesterday continued to show a slow drip of weakness. The notion of weakness should not be a surprise to anyone.

Exports: The straw that broke the camel's back?

It may not be just German exports, but they might be the proverbial straw that broke the camel's back. Yesterday markets were sensitized to risk by the ECB's decision to do nothing. While markets may have thought that the ECB might make Zen monetary policy this month (just what I wanted: Nothing!) they were nonetheless disturbed the actuality of the event along with the description of why the ECB is still sitting on its hands instead of using them to fend off weakness may also be off-putting.

German export weakness does NOT stand alone

German export weakness is perhaps more disturbing because of Germany being the most competitive economy in Europe. If Germany is weak others must be even worse off... Even so there has been some unexpected weakness in industrial output across EMU. Nine of the original EMU member countries have announced IP figures for July and of these nine only Finland and Ireland have logged output increases in July. Germany (-2.2%), France (-0.3%), Spain -2.2%), The Netherlands (-0.8%), Luxembourg (-1.5%), Greece (-2.3%) and Portugal (-1.0%) all have logged month-to-month IP declines in July. France and Spain each have logged a string of three declines in a row. Now German exports are falling and somebody is sitting up to take notice. What? There's weakness here? It's gathering pace? Hmmm...might not be good.

US weakness too

One place seemingly immune to this sort of pessimism is the United States. Not that data there are doing well. The August PMI indices from the ISM, in fact, say each index fall and each sits below the 20th percentile in its own historic queue of data (each weaker only 20% of the time). These are not good results. The MFG ISM in the U.S. is below 50, signaling outright contraction. August auto sales were weaker and Ford Motor declared the great bull market in auto sales to be over. And, of course, there is a three-quarter-long legacy of extremely weak US GDP growth and ongoing issues with productivity.

Flat and too-low US inflation yet a rate hike looms?

With U.S. inflation and wages still subdued with no recent uptrends as inflation has flat-lined in recent months with the headline a full percentage point below its "target" the Fed is NONETHELESS rumored to be "on the fence" about a rate hike. Several major Wall Street houses are calling the odds of a September rate hike at 50/50. I find this absolutely astonishing.

A strange game afoot?

But then some people see ghosts. Some take pictures of UFOs. Others claim to have seen Big Foot. So who knows what other people really see. It is quite curious to me that in this global environment and with the US economy in its own particular environment of disappointment anyone could take seriously the prospect of a Fed rate hike in September. By my way of accounting- and I have been either watching the Fed from the outside or working there since 1977 - there is some strange game afoot.

Is a catastrophe brewing?

It is not surprising to see Europe react to this news of weak German exports especially with exports weak to everywhere. It is not surprising to see markets reacting adversely to news of a nuclear test by North Korea. But this is a world that has been limping by and making its way by ignoring its problems and growing conflicts. When you do this they tend to bottle up then explode forth. There is real risk in that.

Protectionism is bad...now GO HOME!

The G-20 just met and the issue of protectionism was a live one. All attendees had a stake in trying to make progress but in the face of that need we got was some rhetoric. It's as though my Treasury Secretary and President went to China for a G-20 meeting and all I got was this Tee-shirt.

China skates again

China was not confronted over its intransigence in the South China Sea. What's the plan to deal with that? Nor was it confronted about its treatment of foreign firms operating in China. This has been a beyond kick-the-can-down-the-road mind-set by global "leaders". We so desperately need international monetary reform yet G-20 leaders act as though all it's all fine if they can just keep more trade restrictions off the books... Well the financial end is important and been missing since GATT. No one polices exchange rates and trade done at the wrong exchange rates does not count as Free-Trade. And exports can be restricted and companies' operations can be manipulated without putting up new formal barriers to trade...and that is happening, too.

Scared is what scared sees and feels

I think people are seeing the impact on trade flows and they are getting scared. Hanjin, a large S Korean shipper, has gone into receivership and that is going to foul up trade flows even more. Ships are in such great excess and that excess is being scrapped as fast as possible- doing no good for an already under pressure steel industry that hardly needs more competition from "scrap". Reality bites and sometime bites hard and it will bite the hand that has fed it. Ignoring it will not do anyone any good. Yet that has been the way of the world since at least the financial crisis and actually for much longer. No one wants to do the hard work. China is handled with kid gloves on all issues. No one wants to confront China over its multi-dimensional intransigence that has culminated in it projecting its own view across the globe. It is not that China will not accept global standards it's that we now must operate under its rules and under laws of its choosing and making. If we let China's South China seas claim stand, who knows what's next? China is dictating policy and international law. Where will that stop? Weak German exports may simply come to look like a walk in the park if we sit by and watch.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief