Global| Aug 18 2020

Global| Aug 18 2020German Employment Growth Is Whacked in Q2

Summary

German employment growth took the expected hard hit in Q2 as jobs contracted at a 5.3% annual rate quarter-to-quarter. The year-over-year change is a drop of 1.3%. Clearly, the impact of the virus on employment levels has been [...]

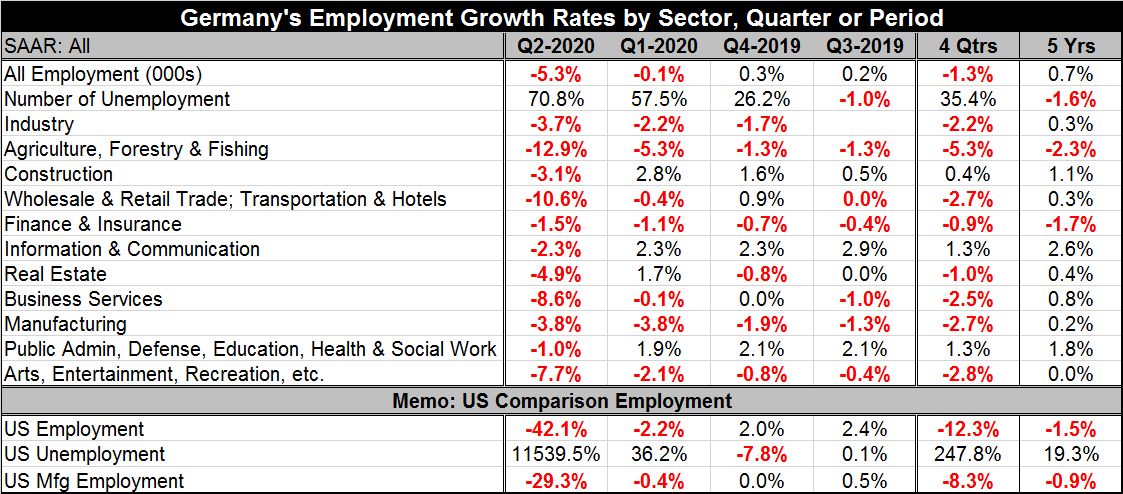

German employment growth took the expected hard hit in Q2 as jobs contracted at a 5.3% annual rate quarter-to-quarter. The year-over-year change is a drop of 1.3%. Clearly, the impact of the virus on employment levels has been substantial affecting trends over the past year and greatly disrupting any events in the current quarter.

German employment growth took the expected hard hit in Q2 as jobs contracted at a 5.3% annual rate quarter-to-quarter. The year-over-year change is a drop of 1.3%. Clearly, the impact of the virus on employment levels has been substantial affecting trends over the past year and greatly disrupting any events in the current quarter.

German employment falls for two quarters running and the number unemployed has been rising for three quarters in a row as a slowing in global trade trends had preceded the strike of the virus.

Manufacturing employment in Germany has been sliding quarter-to-quarter for four quarters in a row. Of the 11 sectors in the table, five of them show persistent quarter-to-quarter declines in employment over each the last four months. The sector ‘business services’ comes close to that mark but instead can complain of four straight quarters without an increase in employment since employment was flat in one of the last four quarters and declining in the three others.

Despite this lingering aspect of weakness, there is no doubt that the real force of job loss came from the virus as the number unemployed rose sharply in Q1 and even more sharply in Q2. And in Q2, the bottom fell out of the job market as employment levels dropped sharply.

Levels of employment have been hit up and down the line with agriculture and forestry surprisingly hard hit and wholesale, retail, transportation & hotels not so surprisingly hard hit. The virus is very hard on the service sector.

In its monthly report, the Bundesbank, however, has set some strong expectations for Q3. It said Germany's economy is set to grow at a sharp rate in the third quarter, after a record fall in the second quarter due to the impact of the coronavirus containment measures. However, it tempered that optimism by adding that activity levels are likely to remain well below the pre-crisis level for some time more. The virus was a difficult thing to combat but its lingering reinfections pose at least as big a challenge for the future as if startups and shutdowns were they to continue that would greatly impact the economy and growth. Employment levels could remain depressed and stop-go policy could keep some professions and businesses on the sidelines for an extended and unintended holiday.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief