Global| Jan 27 2021

Global| Jan 27 2021German Consumer Confidence in February Is Projected Much Lower

Summary

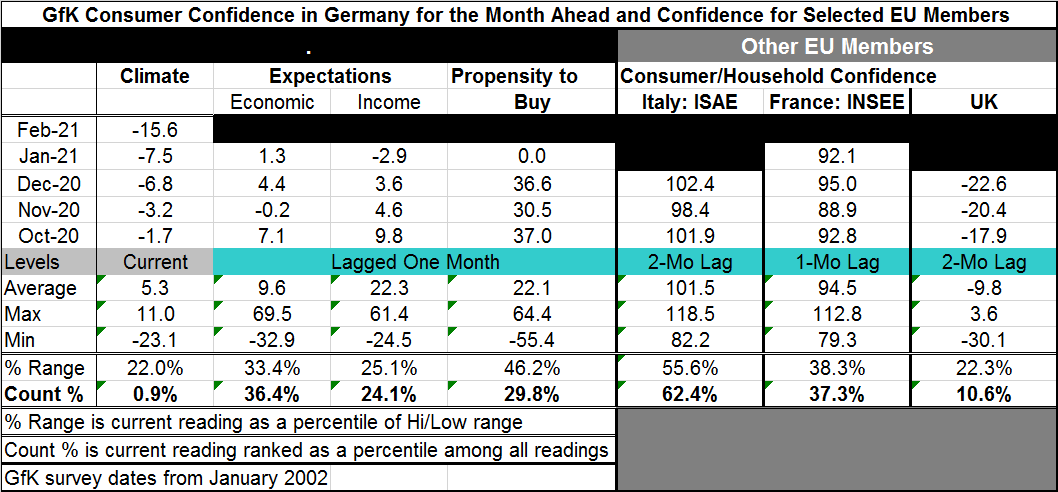

The forward-looking GfK consumer confidence/climate gauge for February has stumbled for the fourth month in a row. Month-to-month the climate gauge fell by 8.1 points, its largest one-month drop since May 2020. Broad headline and [...]

The forward-looking GfK consumer confidence/climate gauge for February has stumbled for the fourth month in a row. Month-to-month the climate gauge fell by 8.1 points, its largest one-month drop since May 2020.

The forward-looking GfK consumer confidence/climate gauge for February has stumbled for the fourth month in a row. Month-to-month the climate gauge fell by 8.1 points, its largest one-month drop since May 2020.

Broad headline and component drop in February

The GfK reading is a look-ahead construct for February. The index components are available only through January. On that basis, there were declines in all three components. The assessments are below:

• The smallest drop was for economic expectations where the index fell by just 3.1 points month-to-month (that is December to January in this case). It is the biggest one-month drop since the one posted in November of last year.

• The next smallest drop was for income expectations. That index fell by 6.5 points month-to-month and marks the largest monthly fall since April 2020 when the coronavirus crisis struck hard for the first time.

• The largest drop by far was for the evaluation of consumers’ propensity to buy. That reading plummeted by 36.6 points month-to-month and marked an even more extreme one-month decline than in the depths of the coronavirus crisis in early-2020. The buying climate drop is the most severe one-month drop since the index fell 65 points in one month in January 2007. It ranks as the second largest drop of all time.

Weak readings for the barometer levels

Not only were the drops in the month hefty, but the new levels of the headline and the components (components with a one-month lag, of course) are weak.

• The GfK headline for February has a 0.9 percentile standing. That means it has been this weak or weaker less than 1% of the time since January 2002.

• Economic expectations are near the lower one third of their queue of values residing at the 36.4 percentile mark in January.

• Income expectations hold down a 24.1 percentile standing, in the lower quartile of their historic queue of data as of January.

• The propensity to buy designation fell very sharply on the month as we saw above; it now has a 29.8 percentile standing. In standing terms, it is not quite as weak as income expectations, but it is weaker than economic expectations.

• All the components have somewhat similar low-in-the-queue standings. And with all of them that low, the reading on climate (for the next month of course) sank to the third lowest mark on record in February. In the history of this report (back to January 2002), there has never been a relapse so large after a massive plunge. The GfK index is in very unusual circumstances.

German economic assessment

The German economy is set to contract in the first quarter due to strict restrictions related to Covid-19 pandemic, the DIW Institute said Wednesday. DIW looks for gross domestic product to contract 3% in the first quarter of 2021 after what it estimates was stagnation in the fourth quarter. Germany’s economic lockdown has already been extended to mid-February.

Confidence elsewhere in Europe

Confidence readings for Italy, France and the U.K. also show adverse consumer attitudes. Since the virus spread is in yet another wave of spreading, in order to make fair like-to-like readings we need to show readings at the same point in time. But the Italian, French and U.K. readings lag the German GfK look-ahead approach so we cannot compare them to the German reading in February.

• However, French confidence was just issued today for January and it can be compared to the German GfK components. France’s 37.7 percentile queue standing for January is comparable to the standings for the GfK components.

• For Italy and the U.K., the lags for comparison are by two months as they both present December levels.

• In Italy, that reading has a 62.4 percentile standing. Italian consumer sentiment has in fact been resilient in the recent period despite having virus issues and now political problems as Italy will have to form a new government in part because there has been political infighting about who gets to determine how virus recovery funds from the EU will be spent. But these factors have not affected Italian consumer attitudes at least they were not paramount through December.

• As of December, the U.K. is already showing signs of the sort of double dip we are seeing in Germany as of February. The U.K. consumer reading fell hard when the virus struck, it recovered and now it is in a stage of descent again as of December that is challenging its June 2020 low reading. The U.K. is suffering a massive virus infection problem and it will probably show weaker results than Germany when the February numbers are in. As of December, U.K. confidence has a 10.6 queue percentile standing. That is much weaker than France or Italy but not yet down to the German standing for February.

Dark days for the virus – Do they still threaten?

On balance, the virus is once again doing devastating things to consumer confidence and to peoples’ lives.

• Country by country- There has been blow-back in Germany over the extended lockdowns; there have been days of rioting in the Netherlands over its curfew. Japan has invoked a state of emergency around Tokyo and more. A large part of China is under lockdown again. Various parts of the U.S. are experiencing differing conditions. California that was very hard-hit is starting to unwind its lockdown.

• New issues- The new development about the virus, however, seems to be less about its trend and more about the new strains that are emerging. There is a new U.K. strain that is faster-spreading and that now appears that it may be 30% more lethal as well. There is also a South African strain and a Brazilian strain that are different.

o Vaccine efficacy: Already developed vaccines still are effective vs. the U.K. strain. And Moderna thinks its vaccine is still effective enough against the South African strain (I have not been able to find out what that means exactly- sorry about the imprecision here).

o Production: AstraZeneca is having some production problems and that is vexing the EU.

o New approaches/actions? So it is still ‘all about the virus’ but the tilt of the news about the virus is beginning to shift and we are also able to see new risks on the horizon. Several European countries are now mandating that people wear more effective masks (Germany is one of those).

o Are tried and true tactics about to fail? We are very deep into yet another round of fighting with this virus and trying to come to terms with what it is and how to defeat it. The cost of stopping the spread remains high, but there is vaccination progress and also the (costly) acquisition of herd immunity. But there are concerns that if the virus mutates further, the vaccination and immunity attained through ‘acquired immunity’ might not apply to a new strain. If that were to become a reality, we could be back at square one and in real trouble since modern economies already are strained and frankly are not providing enough protection or compensation for those economically harmed by the virus as things stand. If they had to go back to ‘square one’ and do this all over again, it’s hard to imagine the economic damage that would entail.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief