Global| Feb 25 2016

Global| Feb 25 2016German Confidence Unexpectedly Ticks Higher

Summary

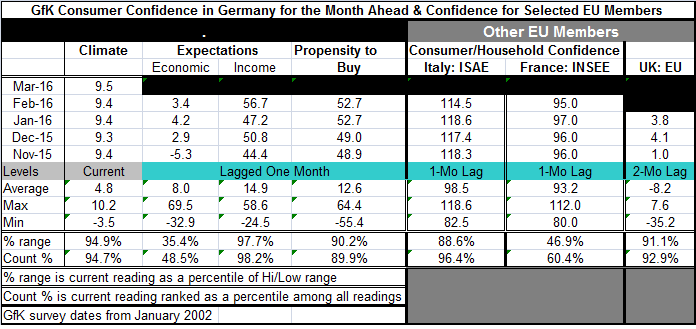

Germany's GfK consumer climate look-ahead gauge for March shows an unexpected increase of one tick to 9.5 from February's 9.4. In February, the gauge was flat with its economic component lower, income expectations strongly higher and [...]

Germany's GfK consumer climate look-ahead gauge for March shows an unexpected increase of one tick to 9.5 from February's 9.4. In February, the gauge was flat with its economic component lower, income expectations strongly higher and the propensity to buy unchanged. The components which lag the headline have been turning up from their recent local lows. The March uptick in the overall reading is the second gain in three months.

Germany's GfK consumer climate look-ahead gauge for March shows an unexpected increase of one tick to 9.5 from February's 9.4. In February, the gauge was flat with its economic component lower, income expectations strongly higher and the propensity to buy unchanged. The components which lag the headline have been turning up from their recent local lows. The March uptick in the overall reading is the second gain in three months.

Germany's confidence measure is near the top 5% of its historic range, an exceptionally high reading, especially considering that the index has been back tracking and flattening. Its components that lag by one month show a very moderate below midrange reading for the economy which has a below-median 48.5 queue percentile standing. The propensity to buy measure has an 89.9 queue percentile standing. Income, with its huge rise in February, now has a 98.2 percentile standing - it has been this high or higher less than 2% of the time historically. The income index was only stronger than February in June and July of 2015. After that, Germany's confidence swoon began to set in. But now the components for confidence all are past their local lows and the question seems to be whether Germany is really done weathering its storm. Is confidence really ready to advance from here on out? Is it possible? I think not.

ZEW, IFO and Migrants

This is a surprising question since the ZEW and IFO Indices were so weak in February. Germany also is fighting politically both inside Germany and with other EMU members on how to deal with migrants. The migrant issue is tearing the EU region apart in its own way as it threatens Schengen, the most loved aspect of the EU that gives members freedom of movement inside the area. Two days ago Macedonia closed its borders shuttering migrants in Greece. Today Greece withdrew its diplomatic envoy from Austria over a dispute concerning migrants. Greece is being made the scape goat for migrant entry and dispersion. Migrants now are being made to pile up there fueling intra-European tensions. Germany has a number of special unrest issues related to public disorder that are directly attributable to the presence of migrants in Germany. Yet, this does not appear to be a factor for Germans in assessing their own environment.

To be sure, the last set of Markit manufacturing and services gauge did not find happy circumstances in Germany. And the weakness in the IFO gauge settled mostly in its climate component rather than in the current component. But the difficulties in expectations would seem to make a strong headwind against the prospect of a persisting advance in German consumer sentiment. This will be something to watch.

Beyond Germany

There are also relatively recent readings on confidence for Italy, France and the U.K., all large fellow EU member economies. Italy just reported out today a relatively large drop in its confidence reading for February. Confidence in Italy has fallen by more month-to-month only about 3% of the time historically. Still, Italy's reading stands in its 96th percentile when evaluated on the same time line as Germany's. But Italian and German confidence gauges are moving in opposite directions. The French gauge from INSEE fell by two points in February and has a very modest 60th percentile standing in its historic queue of data. The French reading has been relatively flat in recent months. The U.K. measure lags Germany by two months, not just one. Its January reading, however, has a 92.9 percentile standing, despite edging lower, a quite strong showing.

Summing Up

Consumer confidence and retailing continue to be measures that are relatively strong in the EU/EMU (95th percentile as of January). The manufacturing gauges are weak (57th percentile as of January) as they are everywhere even though auto sales/production data are still relatively strong. These are common configurations of these reports from the U.S. to Europe. Still, there has been evidence of service sector erosion and in the German IFO framework in February the retail sector took a big step lower. This is not an environment in which one expects to see consumer measures showing improvement. In that sense, Germany is the outlier as everyone else in the table took a step back in their most recent reports. In addition, as the U.K. measure moves up the calendar, we will get a fresher view on how the prospect of Brexit is affecting it; in fact, that concern could spill over and affect other EU members as well. There already are pronounced exchange rate impacts afoot. There is no shortage of troublesome issues to keep your eye on these days.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief