Global| Jun 25 2021

Global| Jun 25 2021German Confidence Continues to Build

Summary

The GfK survey for Germany projects confidence for the month ahead. The new projection is for July. After several months with the confidence reading stuck in single-digit negative numbers, the index for July moved up to -0.3. It’s a [...]

The GfK survey for Germany projects confidence for the month ahead. The new projection is for July. After several months with the confidence reading stuck in single-digit negative numbers, the index for July moved up to -0.3. It’s a reading that is just a touch below ‘neutral.’ At this level, the index sits at the two-thirds mark of its range of historic high-low values but still has a count (or queue) standing in its lower 12 percentile- that is very weak. The month’s projection is two thirds of the way up the range from its lowest to its highest values ever. But when ranked among all values, it still stands in the lower 12 percentile.

The GfK survey for Germany projects confidence for the month ahead. The new projection is for July. After several months with the confidence reading stuck in single-digit negative numbers, the index for July moved up to -0.3. It’s a reading that is just a touch below ‘neutral.’ At this level, the index sits at the two-thirds mark of its range of historic high-low values but still has a count (or queue) standing in its lower 12 percentile- that is very weak. The month’s projection is two thirds of the way up the range from its lowest to its highest values ever. But when ranked among all values, it still stands in the lower 12 percentile.

German Details

The details in the GfK survey lag; there are three component views in this category.

Economic Expectations: Economic expectations have increased again in June, rising to 58.4 after surging to 41.1 in May from 7.3 in April (wow!). In the face of that surge, economic expectations have kept on adding to improvement – a very good sign. Economic expectations have come a long way. They now stand high in both their high-low range as well as in their count percentile where they log a 97 percentile reading – rarely higher.

Income Expectations: Income expectations are moving up with strong strides as well, but this reading remains far below the standing for economic expectations. Income rose to 34.1 in June from 19.5 in May after May had jumped to that level from 9.3 in April. These gains bring income expectations up over their historic median value (above a count standing of 50%) at a reading of 57.5%. Its range standing is about 10 percentage points higher than this.

Propensity to Buy: The propensity to buy (PTB) is on a different track from that of income- and economic-expectations. One difference is that it is much more subdued at a count standing in its 34.3 percentile; it is below its historic median and near the bottom one-third among all historic readings. Another is that while it is improving its transit high has been slow. It rose to 13.4 in June from 10.0 in May and that gain makes it one month in a row. Yet, another difference is the low standing of the index compared to its April level; it is lower on balance over the last two months quite unlike the other two component gauges that are surging over this period. The PTB is not along for the ride.

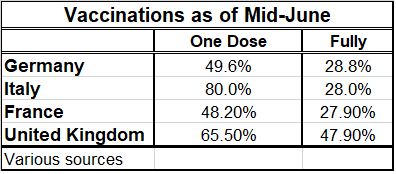

Vaccination Progress

Vaccination Progress

Germany: For now German confidence is rising but it is still low by historic standards. Economic expectations are running high and income expectations are improving and run slightly above their historic midpoint but all that is not translating to a strong buying propensity just yet. Germany is still under-vaccinated and virus risk may be more of a factor in Europe than in America for now. However, Germany and others have been making great progress. Still, there is a cautionary tale from Israel as an unexpected surge in infections has caused Israeli authorities to put their guard back up and to re-impose mask-wearing and other distancing rules. I guess the answer is that just because you are in a clearing does not mean you are actually out of the woods. I cannot seem to find very up to date data for Israel, but as of March, Israel had vaccinated 57% of its population as least once, and 53.3% with a second dose as well. Its number should be much higher by now. Europe shows that it is now at a similar place (slightly behind…) to where Israel was in mid-March. German numbers show 50% of the population with one shot and 28.8% fully vaccinated and the German rollout has been going very strong (Source here).

Italy, France and the U.K.: Italy, France and the U.K. also are reporting improvements in confidence. Italy leads that parade with confidence having a count standing in its 94.8 percentile followed by France at 59.5% and the U.K. at 52.4%. All of them also show a trend to improving confidence scores since at least March. The U.K. is a minor exception with its confidence reading stuck at -9 for two months running.

Summing up

With more vaccinations (see the small table above), there are more opportunities to open the services sector more fully and that adds to jobs, to incomes and to confidence and it makes people more confident that they are on the road to normalcy. Still, the step-back in Israel which has been a virus success story is a warning. And countries have had mixed feelings and mixed progress about vaccinations for the young. So question marks about the rate of future progress remain. For right now Germany is making strong progress and for these selected economies in Europe the trends are favorable as well.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief