Global| Oct 25 2018

Global| Oct 25 2018German Assessment: Current Conditions Flatten As Expectations Lag

Summary

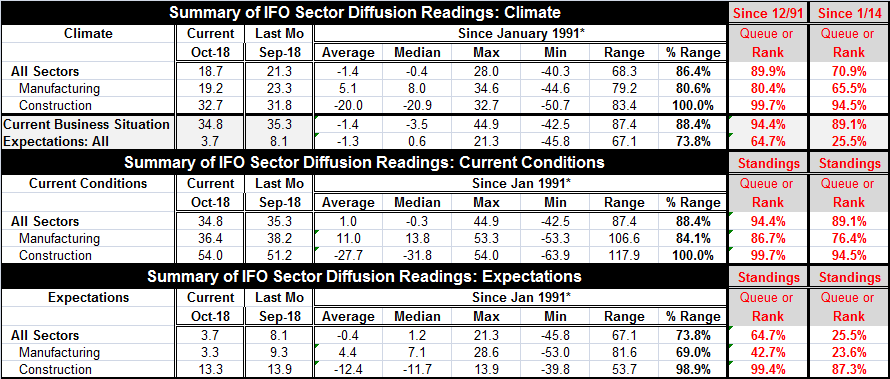

The German IFO reading for October shows that the climate reading steps back to 18.7 from September's 21.3. The index has a standing at its 89.9 percentile at the border of the top 10% in its queue of historic readings. Clearly, [...]

The German IFO reading for October shows that the climate reading steps back to 18.7 from September's 21.3. The index has a standing at its 89.9 percentile at the border of the top 10% in its queue of historic readings.

The German IFO reading for October shows that the climate reading steps back to 18.7 from September's 21.3. The index has a standing at its 89.9 percentile at the border of the top 10% in its queue of historic readings.

Clearly, economic climate in Germany is still excellent. But just as clearly, all is not well with the German economy. German problems spread across the political landscape to the economic frontier. Angela Merkel's coalition is losing its footing and within the coalition Merkel has been losing her grip. Moreover, the entire EU framework is under pressure from a determined new ruling order in Italy that is set on breaking through existing EMU rules in order to gain some policy options apart from shrinking government's spending and role after nearly ten years of no-growth while obeying the rules.

Current economic conditions in Germany remain quite solid and strong. PMI data show a bit more slippage that is on a shorter horizon. The IFO report has been quite strong for a while. On a shorter framework back to January 2014 that aligns it with ordinary PMI data availability, the IFO shows weaker readings all around but mostly for expectations. Most of the weakness is for the part of the report that is already showing some loss of momentum. Expectations for manufacturing over the period from January 2014 are in their 23.6 percentile below their longer-term standing of 42.7%. On the shorter timeline, expectations for construction fall to their 87.3 percentile from their 99.4 percentile standing in the longer sample. Expectations of all of the IFO reporters, however, are at a much weaker 25.5 percentile standing compared to the longer period ranking at its 64.7 percentile.

The shorter horizon makes the point that relative weakness is more of an issue than is absolute weakness. Overall, the IFO shows a very solid Germany economy with an exceptionally solid construction sector. All current readings are firm-to-strong. But by trimming the outlook back to the four and three-quarters years, current performance is less robust and expectations exhibit major issues.

If we view the economy as if it were an organic entity, the problem is getting not its blood through the manufacturing sector. This result has been echoed by the Markit PMI data. Markit data stress the services and manufacturing sectors and show a German private sector with a 5.2% ranking since January 2014. Manufacturing has rank in its 27th percentile compared to services in their 20th percentile. The PMI approach shows a lot more weakness in the Germany economy than what the IFO suggests even when we put the two reports on the same timeline. But generally the Markit and IFO readings have moved together.

If we view the economy as if it were an organic entity, the problem is getting not its blood through the manufacturing sector. This result has been echoed by the Markit PMI data. Markit data stress the services and manufacturing sectors and show a German private sector with a 5.2% ranking since January 2014. Manufacturing has rank in its 27th percentile compared to services in their 20th percentile. The PMI approach shows a lot more weakness in the Germany economy than what the IFO suggests even when we put the two reports on the same timeline. But generally the Markit and IFO readings have moved together.

The German IFO report and its detail dovetails nicely with today's announcement of ECB actions. The weakening in the European economy has been clear. The closely watched PMI data have lost momentum in the EMU as they have lost momentum in Germany. And yet, the European Central Bank has a program laid out to begin to withdraw stimulus. At today's ECB meeting, the Bank announced that it was going to go ahead with the announced schedule of withdrawing excess liquidity. I regard the announcement in view of the economic facts as somewhat surprising. But along with the announcement today that keeps the course for exiting its stimulus program in place, also carries a caveat. Mr. Draghi warned about the economic slowing effectively putting the plan to stay the course in jeopardy despite the adoption of its schedule. A the end of the day, Mr. Draghi was willing to throw a bone to the hard money factions in the EMU that want the stimulus program unwound, but he was not willing to leave too much meat on it. While the message is that the ECB is headed down the road to withdraw stimulus, the message also is the opposite; that the plan itself is on probation depending on economic performance.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief