Global| Dec 13 2019

Global| Dec 13 2019Friday 13 of December 2019: An unlucky day for Japan's Tankan

Summary

Japan's Tankan report has been a closely watched and key indicator of Japan's economy for some time. The manufacturing barometer, which is considered the bellwether of this index, fell to zero in Q4 2019 from 5 in Q3. That drop marks [...]

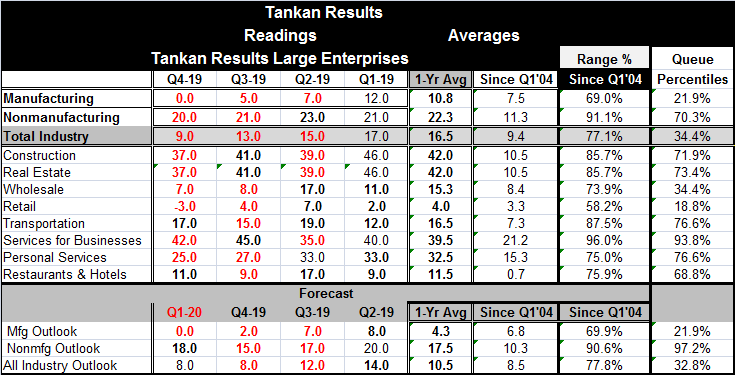

Japan's Tankan report has been a closely watched and key indicator of Japan's economy for some time. The manufacturing barometer, which is considered the bellwether of this index, fell to zero in Q4 2019 from 5 in Q3. That drop marks four straight quarters of erosion. And the last quarter-to-quarter increase for the index was posted in Q4 2017; thus, marking two full years since the index has logged an improvement. The quarter-to-quarter and year-on-year slippages in the barometer are the longest strings of decline since the Great Recession and its aftermath.

Japan's Tankan report has been a closely watched and key indicator of Japan's economy for some time. The manufacturing barometer, which is considered the bellwether of this index, fell to zero in Q4 2019 from 5 in Q3. That drop marks four straight quarters of erosion. And the last quarter-to-quarter increase for the index was posted in Q4 2017; thus, marking two full years since the index has logged an improvement. The quarter-to-quarter and year-on-year slippages in the barometer are the longest strings of decline since the Great Recession and its aftermath.

The large manufacturing firm Tankan gauge itself is at its weakest point in 27 quarters (six and three quarters years). The index was last lower in Q1 2013 when at a value of -8 it was concluding a five quarter stretch of negative readings that were an after-shock of sorts from the Great Recession's primary impact, a period of seven negative readings in a row with the deepest impact a negative reading of -58.

Clearly, this is a situation that the Bank of Japan does not want to be in. The burden of supporting the economy has fallen fully on the shoulders of the BOJ since fiscal policy has been put off-limits because of the Japan's massive debt-to-GDP ratio. The adoption of a consumption tax earlier this year with the economy still struggling and with inflation clearly undershooting was itself a clear message that large scale fiscal policy is out-of-bounds; yet, the BOJ has done just about all it can do. Japan's economic slippage may now be casting its fate on the performance of the global economy and on hopes that an end to the U.S.-China trade war will have sufficient collateral benefits.

Ranking the Tankan reading on all values since Q1 2004 produces a queue percentile standing for the headline manufacturing gauge in its 21.9 percentile, nearly the bottom one fifth of its historic queue of data. This reading has been this weak or weaker only about 22% of the time since end-2001.

The nonmanufacturing gauge that also slipped month-to-month but only by one point has a much higher 70.3 percentile standing. In contrast, it has been higher only about 30% of the time. Clearly, Japan's nonmanufacturing sector is and has been carrying the economy. The Tankan all-industry gauge slipped to 9 from 13 and has a 34.4 percentile standing

I plot the manufacturing outlook gauge as well as the all-industry outlook gauge and the nonmanufacturing outlook gauge in the chart. The manufacturing outlook has fallen to a reading of zero in Q1 2020 from 2 in Q4 2019. The manufacturing outlook has the same percentile standing as the Tankan headline in Q4 at a 21.9 percentile. The nonmanufacturing outlook has an even stronger standing than for the Tankan assessment in Q4 as it is up to the 97.2 percentile. For some reason, the nonmanufacturing outlook has improved to 18 for Q1 2020 from 15 in Q4 2019. But the nonmanufacturing sector gets a small weight in the all-industry outlook which is unchanged quarter-to-quarter and has a Q1 2020 standing in its 32.8 percentile, a bit weaker than its standing in Q4 in its 34.4 percentile.

On balance, this is a disappointing result and weaker than expectations. A positive Tankan reading was expected for the fourth quarter. Some tax breaks for green autos did help to reduce the impact on the auto sector which was hit hard this quarter. In addition, typhoon Hagibis took a toll on the Tankan's Q4 reading. At a zero net reading, the Tankan tells us that optimists and pessimists are at a stand-off in the Tankan diffusion index format. Despite fiscal policy being fundamentally shackled, there are some modest fiscal stimulus efforts being implemented. But clearly Japan's economy remains a creature of the global economic environment and perhaps the most important determinant of its fate lies outside its own domain in the hands of the U.S. and China who just may have cut a deal to improve the global trade environment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief