Global| May 24 2018

Global| May 24 2018French Surveys Show Tilt to Weakness

Summary

The INSEE manufacturing survey shows a steady reading for industry climate in May. The index fell in March and again in April. And now, in May, it has stabilized at this lower level. Still, the trend shows a loss of momentum. The [...]

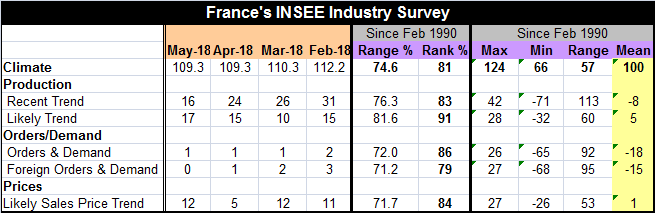

The INSEE manufacturing survey shows a steady reading for industry climate in May. The index fell in March and again in April. And now, in May, it has stabilized at this lower level. Still, the trend shows a loss of momentum. The percentile ranking for climate that puts the current reading in context by comparing it with past values is at its 81st percentile (the index has been stronger than this only about 19% of the time). This is a moderately strong reading.

The INSEE manufacturing survey shows a steady reading for industry climate in May. The index fell in March and again in April. And now, in May, it has stabilized at this lower level. Still, the trend shows a loss of momentum. The percentile ranking for climate that puts the current reading in context by comparing it with past values is at its 81st percentile (the index has been stronger than this only about 19% of the time). This is a moderately strong reading.

The recent trend for production has taken sharp turn for the worse in May despite a steady keel on the climate index. The recent trend gauge has dropped to 16 from 24 in one month’s time and is as low as it has been in the last 12 months. In the last six months, there has not even been a reading on this metric as low as 23. The step back to 16 is a severe drop. The production trend has pulled back this much or more month-to-month less than 7% of the time since 1990. And the production trend metric itself has now fallen for four months in a row.

However, the survey for the likely trend shows a bounce this month as it advanced to a reading of 17 in May from 15 in April. Despite ongoing decay in the recent trend, the likely trend is expected to show improvement. This reading is tied for the fourth highest likely trend reading in the last 12-months. And it has a 91st percentile queue standing.

Why is the likely trend higher in the face of a decaying actual trend? The survey stands mute on that issue. Orders, for example, show a steady reading at a level of 1 where the reading has been for three-month running after dropping in March. Orders and demand have an 86th percentile standing. A second reading, aimed at the foreign market, shows that foreign orders and demand slipped to a net reading of zero in May from 1 in April, 2 in March and 3 in February. This metric has been steadily weakening. And it has a 79th percentile standing.

Last of all, the likely-price-trend metric has spurted, rising sharply to 12 in May from 5 in April. It was last at 12 in March. So this reading is back to where it has been in the March-February period rather than simply having risen sharply. On close inspection, it is the April drop that is out of line. However, the price reading has had some volatility and has been broadly moving higher over the last 12 months or so.

On balance, the manufacturing survey seems to have a lot of weaknesses in contradiction to what emerges as stability in the climate headline and in the likely trend. The decay in foreign orders and easing in orders overall, coupled with a sharp drop in the recent trend for production, should put the industrial sector on notice for a bumpy road ahead. Still, the percentile standings of the survey components have remained strong even as these performance metrics have demonstrated erosion.

In contrast the survey of the services sector shows a clearer sense of erosion and lower assessment of strength overall. This survey documents well the ongoing slippage it is experiencing.

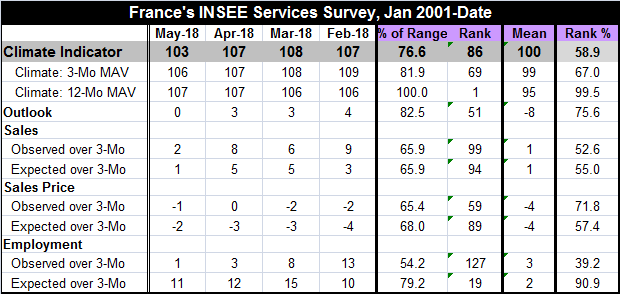

The service sector climate indicator sank to 103 in May from 107 in April. On a timeline back to 2001, the May reading ranks in its 58th percentile, a much weaker standing than for climate in industry and manufacturing. In fact, you can see the deterioration in the climate index by looking at the ranking of its averages over 12 months and three months compared to its current level. Those rankings show a continuing drop. The average climate reading over the last 12 months actually has a 99th queue percentile standing that erodes to a 67th percentile standing for the three-month average and erodes further to 58.9 for the current observation. Obviously, the French services sector is under stress.

Part of this could be the national rail strike in action. The railway workers just rejected the recent government changes to modernize the sector. And the rail strike is disrupting the economy as it drags on. But it is hard to separate the impact of these events from other themes that are in play. Just yesterday the Markit PMI gauges showed a rather broad tendency for EU, German and even U.S. services sectors to be the laggards in comparison to manufacturing. The same tendency seems to be present in France in these reports from Insee today.

Beyond the climate reading, the outlook is deteriorating as well. The outlook metric for the month stands at zero, down from 3 in April, although it does not have a very long recent history of positive readings. The outlook metric at a reading of zero has a 75th percentile standing, right at the border of the top 25 percentile of its historic queue of data.

We have two metrics for sales: one is for observed sales patterns over the last three months and the other is for those patterns executed over the next three months. Both metrics show decay. The more severe decay is for past patterns while the future has a more recent and smaller erosion in place. Still, both sales surveys show readings that historically are mid-stream. The past trend has a 52nd percentile standing while the expected trend has a 55th percentile standing. Each of those standings is just marginally above its own historic median (which occurs at the percentile rank of 50).

For prices we have prices observed over the past three-months and those expected over the next three months. Observed trends have decayed a bit this month while expected trends and observed trends both have firmed slightly over the past four months. Past observed price trends have a queue percentile standing at their 71st percentile; looking ahead, the ranking for expected prices drops to its 57th percentile. Services firms are not expecting a step up in inflation. The ECB has had a hard time getting inflation higher. The inflation data for France generally show a bit more price pressure in France than elsewhere in the EMU. However, this survey is a counterpoint to that trend.

The final services metrics are for employment both the past trend and the future expected path measured over three months. Observed employment trend show a steady and relatively pronounced drop-off from February on. And although the expected trend decays from March, the May reading is still above its February level. Broadly speaking, the outlook has been rather stable since mid-2016 and the current outlook reading remains in that same range setting minor ups and downs aside. But the observed trend has decayed more noticeably and done so recently. The observed trend has a very low 39th percentile standing while the expected trend continues to have a strong 90th percentile standing.

What we see in these surveys is either a resilient survey respondent or one in denial. While there are mostly weakening past trends, the outlooks sometimes weaken in unison and other time’s they ignore the trend and continue to point to better times ahead. There often is no way to understand the optimism.

The Markit PMI survey released yesterday showed a step back is in progress in the EMU, Germany, and France. There have been other hints of an economic slowing as well. Globally, consumption data seems to have been weak. Japan’s PMI metric weakened in May, but the U.S. saw resilience in its Markit PMI readings.

There is no global implosion afoot, but there is evidence of a growth spurt that has run its course. This raises questions about how much growth Europe will post and what sort of inflation pressure might be supported. There are new questions about OPEC as oil prices swirl about $80/barrel. Iran is an oil producer and it is still in play over the nuclear deal that the U.S. pulled out of and that Europe wants to remain in force. Venezuela another oil producer has severe economic problems that have impeded its ability to produce and export oil.

On balance, the growth and inflation outlook is more up in the air that it has been in the past year. Meanwhile, geopolitical events in Asia remain ‘sensitive.’ As a U.S.-North Korea meeting hangs in the balance. China has militarized the islands it grabbed and said it would not militarize. China has been pressuring more small nations to cut ties to Taiwan. The U.S. has pressed China on sonic disturbances aimed at one of its diplomatic missions in China that have caused brain damage to a staffer. The Chinese claim no knowledge of the event.

If you thought that the North Korea meeting was coming and that tensions were simmering down, you were mistaken. Of course, the rhetoric over the U.S.-North Korea meeting itself and been rarified but today North Korea did destroy the tunnels that it has used for nuclear testing so it looks like rhetoric and troubles aside the U.S. and North Korea are headed for an historic meeting of some sort. How all the geopolitical turmoil and events affect global growth is anyone’s guess. But usually this kind of uncertainty is not good for growth or for investment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief