Global| Jun 24 2020

Global| Jun 24 2020French Surveys Rebound

Summary

The graphics tell the story clearly enough. French industry and services indexes plunged and have since seen a substantial rebound. But even a substantial rebound leaves the levels of the indexes shy of where they had been – and by a [...]

The graphics tell the story clearly enough. French industry and services indexes plunged and have since seen a substantial rebound. But even a substantial rebound leaves the levels of the indexes shy of where they had been – and by a long shot- compared to the period before the virus began taking a toll on the economy.

The graphics tell the story clearly enough. French industry and services indexes plunged and have since seen a substantial rebound. But even a substantial rebound leaves the levels of the indexes shy of where they had been – and by a long shot- compared to the period before the virus began taking a toll on the economy.

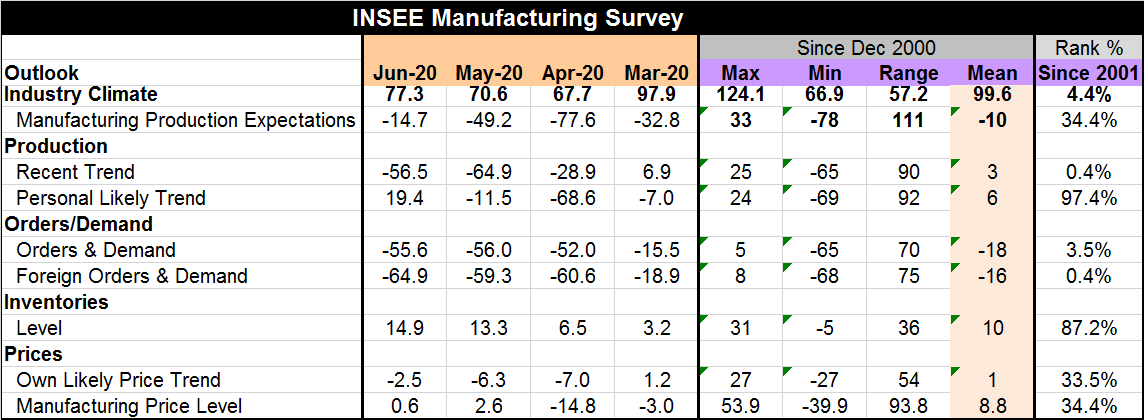

The industry climate index climbed to 77.3 in June from 70.6 in May; its low point was 67.7 in April. The current reading still has a bottom-scraping 4.4 percentile standing.

Manufacturing production expectations have risen strongly from a low of -77.6 in April to -49.2 in May to -14.7 in June. Despite these huge strides, the June index level has a 34.4 percentile standing that tells us it has been lower about one-third of the time.

In contrast, the recent trend of production has improved much less, rising to -56.5 in June from -64.9 in May. It has a 0.4 percentile standing and is rarely weaker than it is in June. However, in sharp contrast to the national trend, most firms seem to feel that their individual trend is going to fare much better. That reading is up to 19.4 in June from -11.5 in May after hitting a low of -68.6 in April. It has a 97.4 percentile reading. The individual outlook is about as optimistic as the overall outlook is pessimistic. Something has to give thee…

Meanwhile, orders and demand languish with a reading in the negative mid 50s where it has been for the last three months. Foreign orders have slipped a bit further in June. Both orders and foreign orders have extremely weak rank standings.

Inventory levels are high, showing a reading that militates against a view of production ramping up sharply.

Prices continue to show a net negative reading for the own price trend. For overall prices, the reading has slipped to a +0.6 net reading in June. But both price trend assessments have rankings at the border of the bottom one-third of their historic queue of values and are consistent with each other.

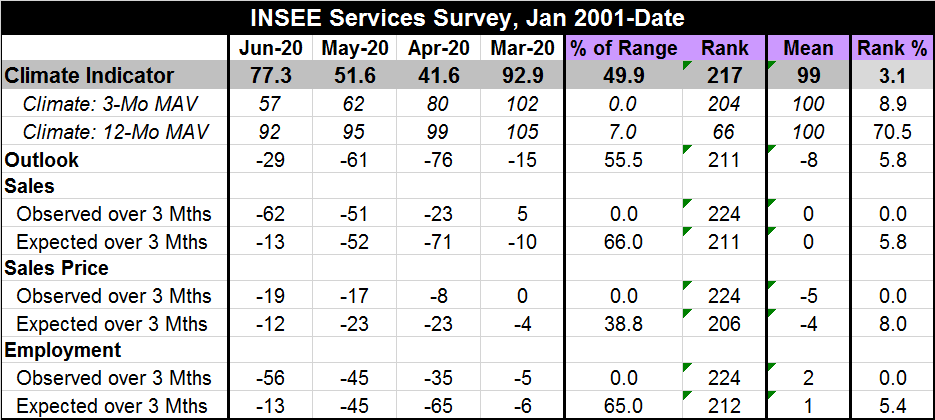

The services index has ramped up from a low of 41.6 in April to 51.6 in May to 77.3 in June. Like the path for industry, the services headline has only a 3.1 percentile standing despite its strong comeback.

The outlook has similarly climbed back, making sizeable gains only to log a 5.8 percentile standing.

Observed sales over the past three months crashed and continue to erode posting the lowest percentile standing on this timeline.

Expectations for sales three-months ahead imploded then surged. But at the end of that roller coaster ride, sales expectations have been weaker only 8% of the time, a still very poor reading.

Observed and expected employment trends mirror sales trends with observed employment sinking to a low in June- an all-time low. Expected employment has steadily and importantly improved and yet has only a 5.4 percentile standing.

The message in these surveys is quite clear. While there is a rapid 'v' recovery in progress, it has a very long way to go. Yet, problems with the virus and in resetting economic activity especially in the services sector have to be solved to reestablish growth. It is unclear how that need and the concept of 'full recovery' will go hand-in-hand. It is also unclear how or if the recent revival of the virus will truncate the ongoing recovery or if the virus revival will prove to be short lived. The survey illustrates the trend and clearly depicts the challenges of moving on. It offers no answers.

Services also rebound

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief