Global| Sep 16 2019

Global| Sep 16 2019French Retail Trends Turn Flat or Worse

Summary

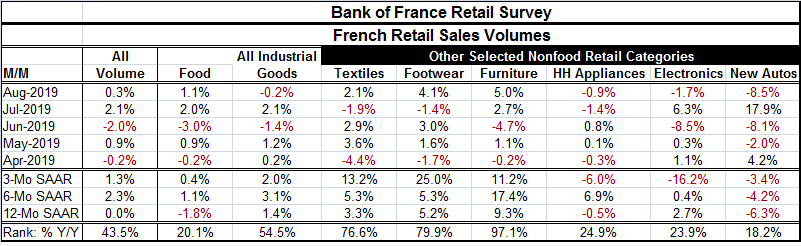

Chart shows weakening auto sales and weakening sales of all industrial products including autos Retail sales volumes in France are showing some growth but very little strength. Total sales volumes are up by 0.3% month-to-month in [...]

Chart shows weakening auto sales and weakening sales of all industrial products including autos

Chart shows weakening auto sales and weakening sales of all industrial products including autos

Retail sales volumes in France are showing some growth but very little strength. Total sales volumes are up by 0.3% month-to-month in August and rising at a 1.3% pace over three months and at a 2.3% pace over six months. But those ‘stepped up' growth rates only bring the 12-month pace of sales back to zero.

If we rank the sector performance based on 12-month growth rates back to 2002, three of the six selected sectors show relatively strong or firm growth and three others (autos, electronics and household appliances) show a rank that is extremely weak in the bottom 25th percentile of all growth rates since 2002 or lower. Furniture sales, up by 9.3% over 12 months, have a 97th percentile ranking; they have been weaker only about 3% of the time. Textiles and footwear sales have standings in their respective 70th percentile decile which makes these rankings relatively firm.

For all industrial goods, the sales rate ranking comes in at its 54th percentile, just barely above the median pace for the period (median pace is at a ranking of 50.0). The 12-month sales pace of industrial goods is 1.4%, but the six-month pace gets up to a respectable 3.1% then the growth rate slips back to 2% over three months. Consumer demand in France is not robust.

What's worse is food sales. Food sales have a very low 20th percentile standing. The year-on-year growth rate has been this weak or weaker only 20% of the time since early-2002. Over 12 months, food sales are lower by 1.8%, but they rise at a 1.1% pace over six months and at a skinny 0.4% pace over three months. This is, however, really weak and surprising for foods where sales usually have consistent, even if low, growth rates.

France seems in need of the sorts of stimulus the ECB is providing. But France will also be hurt by the rising oil prices in the wake of the attack on oil facilities in Saudi Arabia. France does not seem to have a consumer that will be able to brace well for shocks.

...And the shocks are coming. We cannot tell how many or how severe they will be. But this attack on Saudi Arabia is only the beginning. It rips away the mask of invulnerability that the Saudis have worn and it tells us clearly that Saudi oil production is not to be taken for granted. Then there is the question of who struck the Saudi's. I suspect that there is fairly uniform agreement on this even if it is not spoken in public. Probably the same ‘people' that blew up the tankers in the Gulf of Oman in mid-June… probably the same people that have rounded up and herded then captured oil tankers taking them from international waters to their own control to hold them and to hold the ships' crews for their own advantage and leverage. These sorts of acts make it clear how little leverage Iran has and what lengths it has to go to in order to try to have any global influence.

I don't think this is an avenue on which Iran can ride to get back what it has lost. I believe there is no getting around the conclusion of Iran having a hand in this since the technological demands were beyond the Houthi and so who is left to blame? Iran is now ‘cleverly' declaring that it is sure no one could have launched an attack from its territory laying out its fallback position pretty clearly. But that is not likely to stand or to fool anyone. It is more likely that there will be some significant reprisal and that will lead to escalation because of this act.

A flare up of militarism in the Gulf will be good for no one. Neither can we tell where the Hong Kong protests that have gotten hotter will go. Nor does anyone know how Brexit will work out but it is clear that Boris is willing to play ‘bull in a china shop.' But is he willing to be a bull in a china shop when Halloween rolls around and things get serious? However, it does give us a great dress up choice for our next Halloween costume party.

And as always, there are plenty of other things that can go wrong. China is finally admitting that it is slowing and that even a command economy faces constraints and can't choose its growth rate. Will this new reality make Xi more willing to deal or more stubborn? European politics also have all sorts of old alliances shifting from Germany to Spain to Italy and more. The British Empire itself could come apart at the seams as Scotland seems to be seriously considering another referendum since the U.K. adopted Brexit. Since the Irish back stop is the main reason for all trouble, it sure is looking like that small patch of real estate is going to have huge costs for the U.K. or for what's left of it.

France: the Bottom line

France: the Bottom line

France has been the one country in the EMU that despite its troubles and slowing has finally been seeing its PMI gauges outperforming those of fellow members. While the rest of the EMU has been dragged down, France has showed some resiliency in manufacturing and for services. But how long can that last? Moreover, some of France's outperformance came about because France had previously been so impacted. It is not clear how sturdy the French economy can be or what sort of adverse development it can power through. France has no room in its budget as it is already doing battle with the EU Commission over its finances. In short, France may be at the end of short-lived golden period as it spars with the slowing forces in the EMU and hopes to benefit from ECB policy. Troubles in the Middles East are going to undermine some of the help that will be brought to France courtesy of the ECB. Of course, France will have the advantage of a French woman running the ECB. But that is not likely to get it much in the way of special treatment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief