Global| Apr 15 2019

Global| Apr 15 2019French Retail Sales Survey Continues to Weaken

Summary

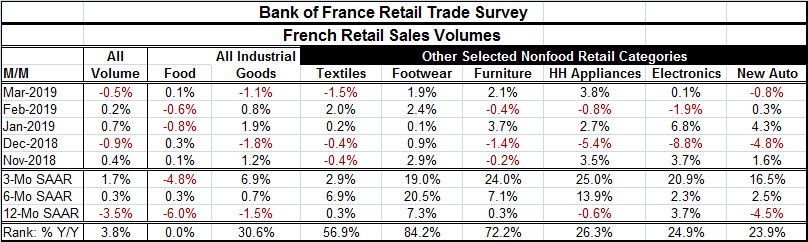

The volume of retail sales fell month-to-month, according to the Bank of France retail trade survey. Over 12 months, the gauge is falling by 3.5%. However, it is getting some traction as sales expand at a 0.3% pace over six months and [...]

The volume of retail sales fell month-to-month, according to the Bank of France retail trade survey. Over 12 months, the gauge is falling by 3.5%. However, it is getting some traction as sales expand at a 0.3% pace over six months and at a 1.7% pace over three months despite a 0.5% decline in March. It may not be vigor, but it does look like life. Of course, as we know from Game of Thrones, just because it moves does not mean it is alive.

The volume of retail sales fell month-to-month, according to the Bank of France retail trade survey. Over 12 months, the gauge is falling by 3.5%. However, it is getting some traction as sales expand at a 0.3% pace over six months and at a 1.7% pace over three months despite a 0.5% decline in March. It may not be vigor, but it does look like life. Of course, as we know from Game of Thrones, just because it moves does not mean it is alive.

The survey includes 17 industrial goods categories plus foods. Industrial goods make up 57% of the index with food comprising 43%. The table includes a sampling of six of the key 17 industries, plus the industrial goods sub-aggregate that includes all 17 industries but excludes food.

The European economies have been weakening. And the French economy has been disrupted by the 'Yellow-Vest' protestors. French manufacturing and services PMIs have been weak. Manufacturing output has been especially hard-hit in Europe. Yet, French retail sales show some sign of struggling to stabilize.

A growth rate accounting

Note the metric at the bottom of the table for each category. It is the percentile rank standing of each of the March year-on-year growth rates ranked against its own performance over all such growth rates since November 2001. Notably, these ranking show the weakest year-on-year food sales of the entire period. Household appliance sales, electronics sales and new auto sales each are in or near the lower quartile of their ranked growth rates of the past 18 years. The metric for all industrial goods is in the bottom 30% of its queue of ranked data putting it solidly in the lower one-third of its distribution. Textiles at a 56th percentile rank are above their median (median occurs at a rank of 50%). Furniture (72%) and footwear (84%) are firm to strong. Sales momentum in France clearly is touch-and-go with overall sales volume growth weaker just 3.8% of the time dragged down by historically weak food sales.

Weakness in March

The BoF survey shows sales trends in eight categories, a count that includes a sub-aggregate for all industrial goods sales plus food. There is also overall measure of retail sales volume. Among the seven nonfood categories, there is a decline in two in March, textiles and new autos. These two declines, along with weakness in industries not displayed in the table, were enough to drive the industrial goods sales measure negative in March despite strong gains in appliances, footwear and furniture and a small rise in electronics. Industrial goods sales aggregate, however, had strong gains in January and February.

Growth trends are uneven across industries

Over three months, six months and 12 months, industrial goods sales are swinging from a 12-month decline at a 1.5% nominal pace to a small 0.7% gain over six months and to a strong 6.9% nominal annualized gain over three months. In fact, over three months, there are very strong double-digit sales gains (annualized) in appliances, furniture, electronics, footwear and new auto sales. Textile sales gained at a 2.9% pace and total industrial goods sales rose at a 6.9% pace over three months. Over six months, there are strong double-digit gains for footwear, appliances, furniture and textiles; all of which rise at a solid pace while electronics and autos make gains more or less in line with inflation. Total industrial goods sales manage a 0.7% rise over six months. In contrast, the 12-month decline features a significant drop in new auto sales and a small drop in appliance sales. Apart from that, there are solid gains in footwear sales, a moderate gain for electronics and weak sales gains for furniture and textiles over 12 months.

Food for thought...

Smoothed year-on-year trends show some recovery in nonfood sales as the survey period comes to contain more recent periods when the 'Yellow Vest' protests have settled down. But indusial goods sales still appear to be restrained and the three-month average of year-on-year food sales percentage change is negative for 11 months running. That is not a good sign. Historically, when food sales turn negative, industrial goods sales either slow or contract. This run of weak food sales is long and something to be watched. Food sales are down in two of the most recent three months with the March gain only a skinny 0.1% increase.

European risks

Europe is still at risk to the UK's decision on Brexit. Britain does not seem to get a consensus on the conditions under which it will leave. Meanwhile, elections in Finland have given the ruling SDP a real scare as the anti-immigration party nearly won. Meanwhile, Italy has been trying to gather up the dissenting parties in the EU for a larger role in the voice on policy in EU matters. In some sense, it is a shame that European leaders are so deaf to the concerns of their people. There are widespread concerns about the migrant problems. The current way of dealing with migrants simply dumps most of the issue in the backs of the Greeks and the Italians and the new Italian government has begun to fight back and to close ports to ships carrying migrants. The land bound or Northern EMU states have shunted the distress to the Mediterranean states and escaped being involved in most of the involuntary refugee care. And one of the main reasons that the U.K. voted to leave the EU was over the heavy hand the EU wielded over migrant issues. That led to an overall backlash against rulemaking in Brussels. But very clearly the same issue that led the U.K. people to vote to leave the EU is the condition that continues to vex many people in current member countries who are not given a direct voice on the issue. But they did find a voice in Finland's elections and previously in Italy's. Where next?

What's next

The next bit of conflict the EU will be dealing with is the trade negotiation with the United States. The EU Commission has just cleared the way for negotiations to start. The EU has made it clear that agriculture barriers and subsidies are not on the table. France, a huge beneficiary of the EU agricultural system is wary about bargaining with the U.S. and wants to throw climate change into the pot especially since the Trump Administration pulled out of the Paris Accord. The talks have not started and already they are not progressing very well!

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief