Global| Apr 02 2009

Global| Apr 02 2009French PPI Shows Year/Year Weakness

Summary

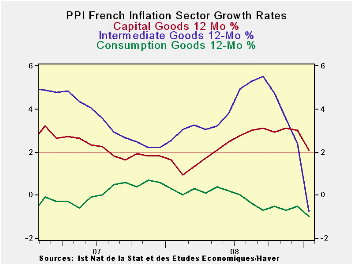

Headline and sector inflation rates for France are showing consistent declines. The core is also on a decelerating trend. Excluding construction the PPI is falling over rapidly. Anyway you cut the inflation signals at the PPI level [...]

Headline and sector inflation rates for France are showing

consistent declines. The core is also on a decelerating trend.

Excluding construction the PPI is falling over rapidly. Anyway you cut

the inflation signals at the PPI level France is showing weakness in

prices.

Still, at the Summit in London, French and German leaders are

focused on patching up the global regulatory system. The persisting

downward pressure on prices suggests that weak growth is still public

enemy number one. The ECB got on board today with a rate cut, but once

again it was about half the magnitude of the cut that the market

expected. Markets retreated after early day strong advances when they

saw the meager cut. Markets regained some ground on the Trichet remark

that there could be more cuts. Markets are playing attention to

everything.

European nations are better protected from bad times compared

to the US as evidenced by their higher continuing rates of unemployment

and more generous social welfare programs.

But the recent backtracking in the Baltic Dry index and

continuing sharp downward pressure on inflation of all sorts in France

are harsh reminders that the recession is still with us and is still

virulent. France was one of the few EMU countries in which the Markit

Manufacturing PMI rose in March. Even so in the EU-Commission scheme of

things France’s industrial sector slipped in March, consumer confidence

stayed at a cycle low, the services sector was on a cycle low and

overall sentiment continued to slip. Weakening price trend are just

another way to underscore this sort of very broad weakness. It is hard

to look at the current needs of the global economy and to square it

with some of the policy work being done in international forums and by

central banks. Being mindful of fiscal discipline is good and wary of

setting of inflation too, but there is a time and place for those

worries and this time and place seem inappropriate for them.

Still European stock markets are hopeful of some sort of turn

in the economy and they are improving. That fits the policy tack of the

European policymakers which is to not worry about growth because enough

has been done. The ECB wants to turn attention to being mindful of

launching irascible inflation trends by not overdoing it. The mixed

signals of the times offer justification for just about anything. Only

time will tell if an opportunity was missed or a hand overplayed.

| France PPI | |||||||

|---|---|---|---|---|---|---|---|

| m/m | Saar | ||||||

| France | Feb-09 | Jan-09 | Dec-08 | 3-Mo | 6-Mo | Yr/Yr | Y/Y Yr Ago |

| Total | -0.6% | -2.6% | -1.1% | -15.6% | -- | -- | -- |

| Consumer | #N/A | -0.6% | 0.0% | -2.4% | -1.6% | -1.0% | 0.3% |

| Intermediate | #N/A | -2.7% | -0.7% | -16.6% | -8.7% | -0.8% | 2.5% |

| Investment | #N/A | -0.6% | -0.1% | -1.8% | 0.4% | 2.1% | 1.6% |

| PPI excl Food and Energy | #N/A | -1.5% | -0.3% | -8.6% | -4.4% | 0.1% | 1.7% |

| HIPP excl Constructions | #N/A | -2.2% | -1.2% | -18.9% | -13.0% | -2.9% | 5.4% |

| Shaded growth rates lag by one -month | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief