Global| Jun 21 2018

Global| Jun 21 2018French Manufacturing Gives Steady Signal As Services Edge Ahead

Summary

The French manufacturing sector gives a steady signal in June but at a level that is off-peak. French services tick higher on the month. In general, the French indexes are moving in concert with those from Germany’s IFO index. Europe [...]

The French manufacturing sector gives a steady signal in June but at a level that is off-peak. French services tick higher on the month. In general, the French indexes are moving in concert with those from Germany’s IFO index. Europe appears to be falling off peak and it is unclear how far it will fall or what is the cause. The weakness in the European data began to show before there were any movements being made on the tariff front. By now that tariffs and countermeasures are in train we can expect activity measures to incorporate their impact. In testimony yesterday, U.S. Commerce Secretary Wilbur Ross said there would have to be a more painful international environment before U.S. trade negotiations can reach their objective. German automaker Daimler surprised markets with an announcement today warning that trade tensions already were hitting sales.

The French manufacturing sector gives a steady signal in June but at a level that is off-peak. French services tick higher on the month. In general, the French indexes are moving in concert with those from Germany’s IFO index. Europe appears to be falling off peak and it is unclear how far it will fall or what is the cause. The weakness in the European data began to show before there were any movements being made on the tariff front. By now that tariffs and countermeasures are in train we can expect activity measures to incorporate their impact. In testimony yesterday, U.S. Commerce Secretary Wilbur Ross said there would have to be a more painful international environment before U.S. trade negotiations can reach their objective. German automaker Daimler surprised markets with an announcement today warning that trade tensions already were hitting sales.

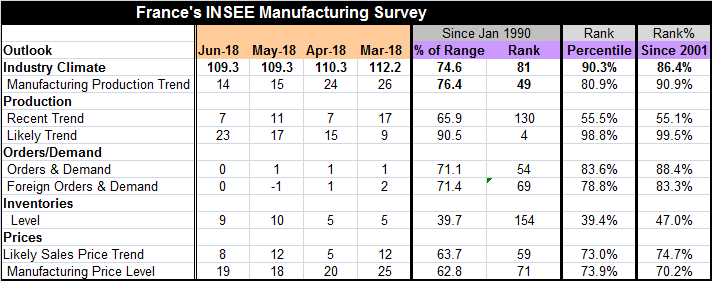

The INSEE manufacturing survey of French industry shows an unchanged 109.3 climate reading for industry in June. This index has been higher from August 2017 through March 2018, a period of eight months. The current index reading is some 4% below its peak reading on this previous period. That reading has an 86.4 percentile standing over its queue of values since 2001.

The production trend for manufacturing edged lower to 14 in June from 15 in May and carries a 90.9 percentile standing on readings back to 2001. There are also surveys for the recent trend and the likely trend. Interestingly the recent trend fell in June to a reading of 7 from 11 in May. This index has been as high as 23.3 in January. Now it is lower and at only a 55.1 percentile standing. However, the likely trend has jumped to 23 from 17. It has been building momentum steadily over the last three months and now has a 99.5 percentile standing. There is no mention in the survey why with the recent trend deteriorating the outlook is ramping up so sharply and doing so against contrary trends in Germany and for much of Europe based on Markit survey data.

Orders and demand are little changed month-to-month with total and foreign orders both showing a value of zero in June. For overall orders that is a slip from a +1 reading, but for foreign orders it is an improvement from a -1 reading. Total orders have a queue standing in their 88th percentile while foreign orders have a standing in their 83rd percentile.

Inventory metrics show little change on the month and with an overall reading close to its median on a 47th percentile standing.

Price trends show likely sales prices with less pressure as the index drops to 8 in June from 12 in May and logs a 74th percentile standing. The manufacturing price level is a tick higher in June at 19, up from 18 in May and has a weaker 70th percentile standing.

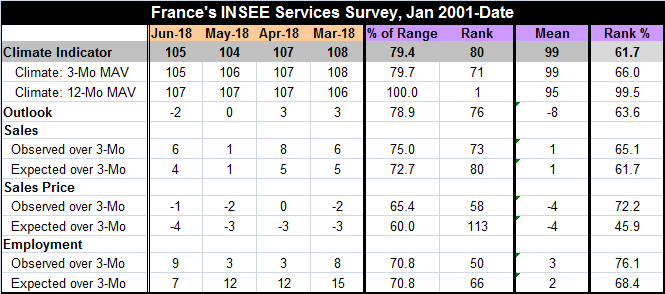

For services, the climate indicator edged up to 105 in June from 104 in May. However the three-month moving average (MAV) for that indicator moved lower and the 12-month indicator’s MAV was unchanged.

The outlook for the services sector slipped to -2 in June from zero in May to post a 63rd queue percentile standing.

Observed and expected sales both improved in June with observed sales at a 65th percentile standing and expected sales at a 61st percentile standing. Both of those are moderate but positive readings and standings.

Sales pries are still getting raw responses that are negative numbers. But the observed sales price strengthened with a survey response of -1 in June up from -2 in May as expected prices worsened to -4 from -3. Still, observed prices have a 72nd percentile standing with expected prices having a below median 45.9 percentile standing.

Observed and expected employment responses went in opposite directions this month. Observed conditions improved noticeably to a net reading of 9 in June up from 3 in May while expected employment fell to a net reading of 7 from 12. Observed employment over three months has a 76th percentile standing with expected employment over three months at a 68th percentile standing.

We see very little movement in the INSEE surveys of manufacturing and services between May and June. The manufacturing metrics tend to have higher queue standings, but there is irregularity and unevenness in both surveys. With trade tensions rising and a real life game of tariff retaliation taking place, it would not be surprising to continue to see this survey record even lower standings next month.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief