Global| Jun 10 2015

Global| Jun 10 2015French Manufacturing Continues to Struggle

Summary

French industrial production has hovered around a zero annual growth rate for several years. May's 2.1% month-to-month drop leaves IP shrinking by 3.7% year-over-year. Sequential growth rates show that recent IP trends have become [...]

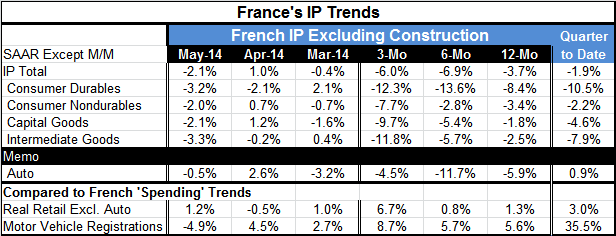

French industrial production has hovered around a zero annual growth rate for several years. May's 2.1% month-to-month drop leaves IP shrinking by 3.7% year-over-year. Sequential growth rates show that recent IP trends have become even weaker than their declining year-over-year pace.

French industrial production has hovered around a zero annual growth rate for several years. May's 2.1% month-to-month drop leaves IP shrinking by 3.7% year-over-year. Sequential growth rates show that recent IP trends have become even weaker than their declining year-over-year pace.

While some (and slightly more up to date) PMI gauges show some progress in French industry, the industrial output report itself is still less than encouraging.

Trends for consumer durable goods output are negative and deteriorating. Trends for consumer nondurable goods are negative and becoming increasing weaker. Capital goods output also is showing declines on all horizons and declines that are getting progressively steeper. The same is true of nondurable goods trends. The picture for industrial production is bleak on all horizons and for any type of goods. A separate look at auto production shows negative growth rates on all horizons, but they are not progressively deteriorating.

When we compare these output trends to spending trends in France, we see that output trends are far weaker than are French spending trends. Year-over-year output is down by 3.7% while real retail spending (ex-autos) is up by 1.3% and motor vehicle registrations are up by 5.6% (auto output is down by 5.9%).

Two months into Q2, French IP growth is shrinking at a 1.9% annual rate and all components are falling faster. French spending is rising in the new quarter.

The French industrial sector is still struggling. The weaker euro exchange rate has not helped the sector to recover. France may still be finding competition within the euro area (where the euro devaluation does not help it) be too much for it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.