Global| Apr 25 2017

Global| Apr 25 2017French Manufacturing and Service Sectors Weaken But Stay on Trend or Hold Recent Gains

Summary

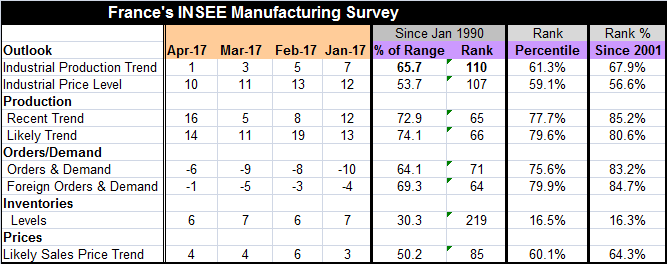

The French manufacturing sector trend index is down to 1 in April from 3 in March. However, the recent-trend was up and the likely-trend was up on the month. The industrial price level reading has softened over the past four months [...]

The French manufacturing sector trend index is down to 1 in April from 3 in March. However, the recent-trend was up and the likely-trend was up on the month. The industrial price level reading has softened over the past four months but only slightly. Orders and demand as well as foreign orders and demand are slightly stronger since January. Inventory levels are low and hardly subject to any reassessments recently. The likely sales price trend in manufacturing is very steady at a moderate 64th percentile ranking in its range since 2001. There is no evidence of inflation building.

The French manufacturing sector trend index is down to 1 in April from 3 in March. However, the recent-trend was up and the likely-trend was up on the month. The industrial price level reading has softened over the past four months but only slightly. Orders and demand as well as foreign orders and demand are slightly stronger since January. Inventory levels are low and hardly subject to any reassessments recently. The likely sales price trend in manufacturing is very steady at a moderate 64th percentile ranking in its range since 2001. There is no evidence of inflation building.

I will refer to the ranges since 2001 since I have those for both manufacturing and services. Prior to 2000, the service sector data were quarterly. The manufacturing table however also has rankings back to 1990. Series ranked on the shorter time span are generally somewhat stronger, a clear indication that the recent period is weaker than the full historic period.

The manufacturing sector ranking shows the IP trend at its 68th percentile with the recent trend at its 85th percentile and the likely trend at its 80th percentile. The recent and likely trends are quite reassuring. The industrial price level is at its 56th percentile, only slightly above its median for the period (median occurs at 50%). The likely sales price is a bit stronger but still moderate at its 64th percentile. Orders and demand, both for overall and foreign, only stand at in their low 80th percentiles, good solid-to-strong readings.

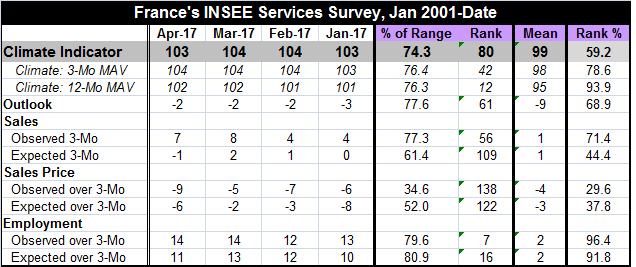

The services picture is not too different but is softer overall. The service sector climate indicator ticked lower in April but has been in a very narrow one-point range over the last four months. The three-month average is steady as is the 12-month average.

The outlook has been steady for three months running after making a slight improvement in February. Observed sales ticked lower in April but still hold most of the sizeable uptick logged in March. Expected sales moved lower and are the weakest in seven months. Observed sales prices have been weakening as the year goes by. Expected sales prices are soft. Employment and expected employment changes by month have been positive and in a narrow range with expected sales moving two notches lower in April.

In terms of the standings of the variables for the services sector, the climate indicator is at a moderate 59th percentile queue standing. The moving averages of climate are generally higher-ranking and that is not a good sign. That points to some climate slippage. Still, the outlook has a 68th percentile standing. Observed sales have had a solid 71st percentile standing, but expected sales have now slipped to 44th percentile standing - a below median signal. These are weaker results than for manufacturing. The sales price shows a weak observed pattern over three months with a 29th percentile standing and a weak expected pattern at a 37th percentile standing. The employment situation, however, is solid and strong with a past observed pattern at a 96th percentile standing and an outlook at a 91st percentile standing.

On balance, these are pretty solid results for France. They are not quite as upbeat as the Markit PMI data especially not for services, but they are pretty positive assessments. Manufacturing is showing revival and is still something to watch and to compare with actual figures since French actual manufacturing IP shows three monthly declines in a row as of February and a year-on-year drop of 0.5%. The survey indicators have been stronger than the traditional accounting style reports internationally. So we do look at these signals with a grain or two of salt.

Still, the INSEE survey has been around for a long time and it is signaling an upbeat outlook for manufacturing even if it is a bit more cautionary for services. For now all signals are still positive.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief