Global| Apr 28 2020

Global| Apr 28 2020French INSEE Surveys Show a Sharp Shift in Sentiment

Summary

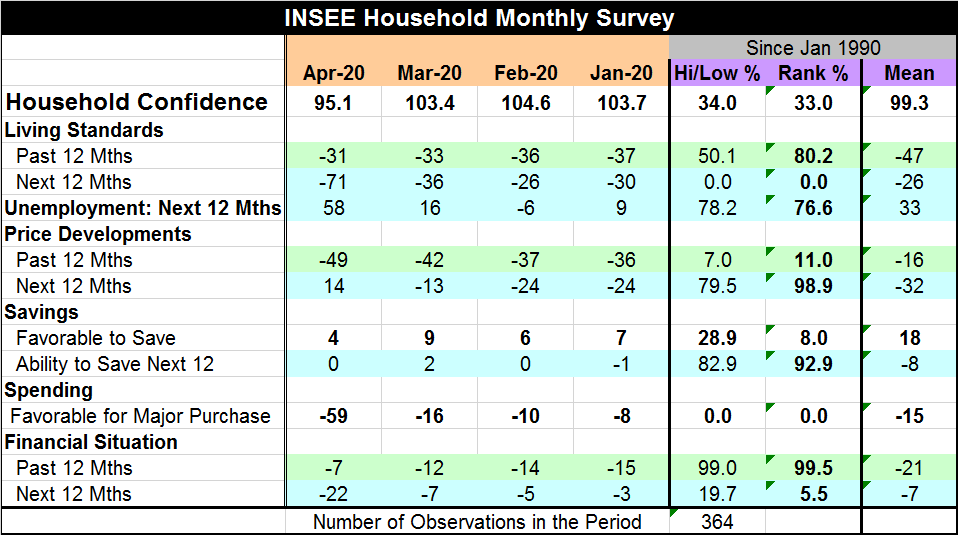

The French surveys have been very weak in April (graph/table). The household survey (table), despite its seemingly mild drop in April, has actually logged the largest month-to-month drop (a drop of 8 points) in the history of the [...]

The French surveys have been very weak in April (graph/table). The household survey (table), despite its seemingly mild drop in April, has actually logged the largest month-to-month drop (a drop of 8 points) in the history of the series back to 1972, according to the French statistical institution INSEE that issues the report.

The French surveys have been very weak in April (graph/table). The household survey (table), despite its seemingly mild drop in April, has actually logged the largest month-to-month drop (a drop of 8 points) in the history of the series back to 1972, according to the French statistical institution INSEE that issues the report.

In the chart, I present the sector indexes for manufacturing and services where the survey drops are far more eye-catching. Clearly France is recording weakness across manufacturing, in services and for the household sector in April. No one is being spared.

The drop in the household indicator is a record, but the level of the index reading is 'only' a bottom 33 percentile ranking in April. But even that might be misleadingly-firm based on the component readings.

The nitty gritty of the survey

• Living standards: The living standards responses show that the last 12-months rating slipped a bit but has an 80.2 percentile standing in April. In contrast, the next 12-month reading plunged to -71 from -36 and has its lowest rating since January 1990. Yikes!

• Unemployment: The next 12-months- has seen the indicator for expected unemployment rise to 58 from 16. That lifts the response to the 76.6 percentile (just a bit more than one-quarter of the time unemployment has been more firmly expected). French households have transitioned from having very low fears of unemployment to seeing the grim reaper of job loss at the door-step.

• Price developments: Over the past 12 months the rear-view assessment of price development has been slipping lower and lower; in April the backward assessment of past price developments fell to its 11th percentile admitting that a solid period of low inflation had passed. But the forward view which had diminished over the last two months has shifted sharply from just one month ago, rising from a -13 reading to a +14 reading. That response placed expected price developments over the next 12-months as being higher only 2% of the time historically. This inflation expectation undoubtedly stems from all the government action to prop up the economy as well as actions by the ECB. But in fact, these actions are not propping up growth and oil prices have touched lows not seen since 1986. It is not clear to me what inflation process survey participants think is in gear over the next 12-months, a period when I expect inflation to remain quite low and when growth is going to be reduced then mount a partial recovery.

• Savings: The environment in the past was not regarded as favorable to save with an 8th percentile standing. The period ahead shows little change in the ability to save which hovers at a high rating in its 90th percentile and has been around that standing for the last four months.

• Spending: Survey participants' view of the timing for making a major purchase crashes and burns in April, dropping to -59 from March's -16. There had been a steady but much, much, slower progression lower in the recent months. This month's reading is the lowest on record. Terrible time to spend.

• Financial situation: From the brim to the dregs. The financial assessment looking backward transits from some of the highest recorded responses in the previous months (a 99.5 standing in April) to a 5.5 percentile standing looking ahead to the next 12-months in April. The April survey response fell to -22 from -7.

The headline of the French survey does not do justice to communicating the pain and angst we see in the belly of the survey. It is a poor time to spend, inflation is stalking the consumer as is joblessness. It is hard to imagine a much worse vector of values than what is being logged in April. And, of course, a lot of this is just the month-to-month worsening. The manufacturing and services surveys echo these sorts of sharp shifts in sentiment. I wanted to include the sector indexes in this report to highlight their weakness along with the component readings in the household survey in contrast to a household headline that seems far more muted than the details in the report are indicating. All is not well in France among households, in the services sector or among manufacturers and other businesses.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief